- Responsible for new idea generation; portfolio construction; risk management; due diligence

- 25+ years overseeing concentrated small-cap portfolios, on behalf of the most sophisticated allocators in the United States

- Previously: Founder, Endowment Capital Group; Portfolio Manager, Downtown Associates; Analyst, W.H. Newbold’s Son & Company

- University of Pennsylvania, Wharton School, B.S. 1986

- Married to Isabella, 3 sons, 3 daughters, 2 dogs

by Owls Nest Partners on Mar 31, 2019

As you can tell whenever you hear us discuss individual names, we don’t own the market but instead own a handful of what we believe to be very special businesses that have secular growth drivers because of their ability to innovate and thrill their customers. To prevent this letter from being longer than it already is, we have only highlighted in detail our largest recent addition to the portfolio and the position we exited since the logic behind a sale is also important. Please reach out to us to learn more about our other investments.

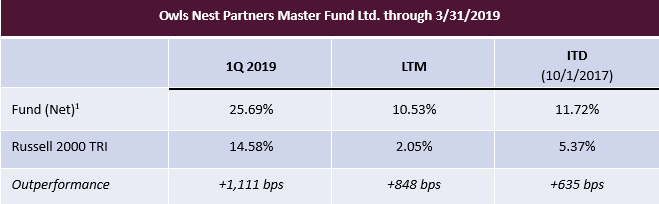

Performance:

Performance is laid out in the table below. We believe our quality business models, underleveraged balance sheets and avoidance of crowded trades, have served us well relative to the market in the first quarter of 2019, and the last twelve months.

Investment Program:

The hallmark of the Owls Nest Partners approach is the purchase of industry leading growth companies when a temporary headwind has recoiled the fundamental growth drivers and compressed its multiple. This typically happens as hot money “renters” exit and drive the price down. There is no such thing as a free lunch: we can only access high quality business models with liquid and strong balance sheets, proven management and a long runway of growth and margin expansion, if we accept that our companies will appear “catalyst-less” and therefore may be dead money for some time. Of course, the offset to this cost is that these moments are (ironically perhaps) when a company can invest in its own business with the highest returns, and there is wonderful optionality associated with a well-run, shareholder friendly, cash-laden company that is able to aggressively put money to work during a temporary headwind.

It is our belief (and experience) that our future outperformance will not be driven by any economic or market forecasting prowess but instead by ten unique investments, each playing out over time. We perceive these investments to have modest downside due to high quality and low expectations, and very significant upside as growth and margin expansion return in spades. We seek reasonable ballast and diversification within the portfolio as a result of our natural conservatism (strengthened by our co-investment alongside clients), an unwillingness to think we can predict markets or economies, and a predisposition to avoid crowded trades and instead invest in temporarily out of favor areas.

Holdings as of 3/31/2019:

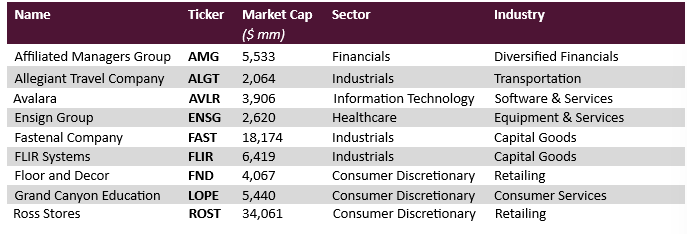

We ended Q1 2019 approximately 95% invested in nine companies. The current holdings are as follow (in alphabetical order):

Median Total Debt/Market Cap: 3.6%

Median Market Cap: $5,440 million

Active Share vs. Russell 2000: 99.5%

Quarterly Attribution:

During the quarter, we had 10 companies contributing to our performance, and each of the ten was a positive contributor. Our largest gainers were Avalara (AVLR), Floor & Decor Holdings (FND – which along with AVLR and ENSG was discussed in our 2018 review letter http://bit.ly/2018_Company_Overviews) and Allegiant Travel (ALGT). These three were responsible for about 60% of the quarter’s performance. Although each of these companies released somewhat stronger than anticipated Q4 results and 2019 guidance, nothing remarkable drove their stock performance, and each continues, in our opinion, to have a very long runway of growth. Also positively contributing, in order of largest impact to smallest, were Ensign Group (ENSG), Grand Canyon Education (LOPE), Fastenal (FAST), Ross Stores (ROST), Affiliated Managers Group (AMG), FLIR Systems (FLIR), and Healthcare Services Group (HCSG), which was sold during the quarter and discussed below.

Portfolio Adjustments:

During the quarter we sold our position in HCSG (discussed below). We have a considerable pipeline of new ideas, but the stars must be properly aligned in terms of fundamentals, sentiment, valuation, and our level of conviction for a new position to be truly additive to the portfolio. Given the attractive opportunities in our existing portfolio, we chose instead to reallocate those dollars to increase certain existing investments. During the quarter we added most significantly to LOPE (discussed below), but also to ENSG, AMG, ALGT and FLIR.

We sold HCSG because we weren’t satisfied with the company’s progress with reestablishing its growth trajectory. Why isn’t the company growing as we had hoped? This may just be a matter of timing if they are just having a tough time replenishing their talent pool in a challenging hiring environment. But we have concluded that although they will continue to be the dominant player in their area, their value proposition simply isn’t as compelling as we had thought. As a provider of outsourced housekeeping and dietary services to skilled nursing facilities, HCSG can provide consistency, cost savings and headache reduction to many customers as they outsource this “non-core” operation. But HCSG historically also provides another value in that it serves as a bank – turning what would otherwise be weekly payroll into 30- or 45-day terms with HCSG. In response to industry struggles, HCSG has had to tighten credit terms and demand more frequent payment from its customers. This activity makes total sense, but it reduces the value of HCSG’s role as a provider of liquidity, and we think this change has materially slowed HCSG’s ability to grow.

One of the beauties of our highly concentrated model is that we are always challenging each of our theses, and we believe we should sell whenever a key element of the thesis cannot hold up to the scrutiny. At the end of the day, we made a few dollars with HCSG, and it contributed meaningfully positive relative attribution, especially in Q4 2018 when it was up in a significantly down market. But we can’t fall in love with ideas, and the work completed on a company is a sunk cost and cannot justify holding the position after the thesis becomes murky. Lastly, we are grateful that our work on HCSG led us to ENSG, which has already contributed very positively and which we expect to own for a very long time.

Grand Canyon Education (LOPE):

The historically entrenched and slow-moving world of post-secondary education is changing dramatically in reaction to the student debt crisis, a changing economy which needs different skills, technology available to educators, and changes in students’ tastes and influencers. Grand Canyon Education is at the forefront of this enormous and important wave.

With visionary leadership, the benefit of greater agility and a lower cost structure due to the lack of legacy entitlements and encumbrances typically found at traditional universities, and the willingness to invest over $1.2 billion in a greatly expanded and modernized physical campus, Grand Canyon has developed into the leading Christian university in the Southwest United States with over 20,000 students on campus and nearly 80,000 students (mostly graduate or degree completer bachelor students) online. The school is focused on academic programs and degrees that today’s college students seek, and has thrived, in no small part, because of its ability to add new programs as soon as demand appears. Growth has also allowed it to freeze tuition for more than ten years such that the average annual ground tuition, net of scholarships is ~$8,600. Grand Canyon has an average class size of 25 on campus and only 15 online and is accredited by the same body that oversees Notre Dame, the University of Chicago and the University of Michigan among others. And all objective measures of outcomes – retention, graduation rate, job placement rate, debt levels at graduation – help explain why the school has become so popular with millennials who aren’t wowed by US News rankings but who care more about what they hear from friends with regard to their experiences and outcomes. Phoenix’s weather doesn’t hurt either. But in many ways, this success has just established the foundation for the next and more impactful stage of growth.

In 2017, Purdue University changed the educational landscape and opened a new world for Grand Canyon. Needing Kaplan University’s expertise in online program management, Purdue acquired the for-profit Kaplan from Graham Holdings and received regulatory approval to use Kaplan as a tool to accelerate their rollout of online education. With that precedent established and through a series of transactions last summer, Grand Canyon Education was able to switch from being the operator of a single university to being an online program manager (OPM) able to serve multiple universities, greatly expanding its long-term potential. Every university realizes the need to move courses online for many reasons including cost, convenience, brand extension, and leverage. But moving online is extremely challenging and expensive, and doing it well and cost effectively requires experience and scale that few companies have. No OPM has more scale or as broad of a service offering as Grand Canyon. We look forward to announcements of Grand Canyon’s growth nationally as it serves other universities in other regions of the country.

This quarter provided an exceptional opportunity and yet another reason to buy LOPE. On December 18, 2018, Grand Canyon announced that it was acquiring Orbis Education for $362.5M, its first acquisition since the original acquisition of the failing private Grand Canyon University in 2004. Orbis is the nation’s leading OPM dedicated to healthcare education, and its financial model is like any OPM in that any new client relationship loses money until it scales at which point it can become very profitable. Because of its 40%+ growth, Orbis’s mature and highly profitable clients are offset by quickly ramping but still unprofitable clients, so that in the aggregate the business is breakeven and therefore dilutive to LOPE earnings once financing costs are factored in. Amidst an already anxious stock market in Q4, a surprising and mildly dilutive acquisition of an unknown (to Wall Street) company was not well received, and LOPE’s stock fell from its November high of $130 to a base in the low $90s where it languished for two months.

To be perfectly honest, we were surprised by this acquisition too. It is true that we have developed enormous respect for this management team over the decade we’ve known them, and any management team that turns the company’s last acquisition which was for a few million dollars into a business worth a few billion dollars likely deserves the benefit of the doubt on an acquisition. Nonetheless, our first reaction was “huh?” So, we got to work. What we have learned is that Orbis is a very special business, solving a huge societal need in a very innovative and ultimately profitable way, and Grand Canyon was the perfect acquirer for the business (so perfect that Orbis’s management rejected higher bids).

Over the next couple decades, Orbis/Grand Canyon is going to help solve the crisis of the shortage of healthcare professionals, especially nurses. We all know of the nursing shortage, and we know that the demographics will make this intensely more acute as the population ages, baby boomers enter the key healthcare usage stage and as the biggest chunk of the current nursing pool reaches retirement age. But do we all know why there is such a nursing shortage? After all, nursing pays pretty well. The average RN will make $75,000 this year and the average nurse practitioner will make over $100,000. Demand is not the problem. More than enough people want to become nurses. Supply (educational capacity) is the problem. In fact, every year over 50,000 qualified applicants for nursing schools get rejected due to lack of available school openings. Why is there such a shortage of openings?

Training a nurse is a very hands-on and expensive proposition. Universities make enormous money off Econ 101 classes in which a single professor and some minimum wage TAs teach 800 students in a single room. With nursing, however, the nursing faculty is too small because nursing professors actually make meaningfully less than they would as nurse practitioners. The alternative for Econ 101 TAs is often working at Starbucks for tips, and they can have 50 students. A clinical nursing professor has to forego a $100K+ job and can teach six to ten in a class. Hence the crux of the problem. With the exception of expensive private schools, schools lose money on every nursing student they produce. State schools often have stipulations that make it difficult or impossible to have much higher tuition for nursing than for other fields. As a result, the number of slots is not growing despite the demand. Closely related to the shortage of faculty is the general lack of clinical rotation availability as healthcare providers are reluctant or unable to accommodate demand or have unlicensed trainees throughout their facility during standard times.

Over the last 15 years, Orbis has developed, refined and successfully implemented at scale a unique solution that works for all three key constituencies – students, universities trying to grow their nursing programs, and healthcare providers who face a shortage of available nurses but who are unable to offer up lots of premium rotation slots. The Orbis solution is an accelerated BSN done in partnership with a university that has a wellestablished and mature traditional nursing program. By eliminating scheduled breaks in the calendar and by utilizing online learning and simulation where appropriate and additive to quality, the Orbis program condenses the two-year program to 16 months. This allows the student to start working sooner, making $50k ($75K X 2/3 of a year) in their second year, reducing their debt burden. Furthermore, this program tends to attract the most motivated students which also leads to the best outcomes. In the end the value proposition for the student is clear: they can access a great education and get started in the career they desire far more quickly than would otherwise be possible.

Orbis’s university partners include Northeastern in Boston, Loyola of Chicago, Xavier in Cincinnati, Marquette in Milwaukee. In every case, the university controls the program and establishes the standards and curriculum. However, Orbis provides a wide breadth of critical services for the university, including: all the course development including online courses where the university has little experience; developing separate facilities nearby for clinical practice/simulation; utilizing its well-developed network of clinical providers to lock up necessary clinical rotations; all marketing and enrollment; hiring and training all faculty; and all student support. As a result, university partners are able to grow from one class per year of 30+ students to three classes per year of 70+ students with comparable or better graduation rates and first-time nursing exam pass rates and job placement. This is a very regulated environment, and Orbis’s experience and spotless record gives academic partners great peace of mind. The economics work very well for university partners too. They are spared program startup costs, and they receive 30% of revenue typically with very little direct cost associated with that revenue.

The other key value proposition is for healthcare providers. In fact, the number one factor in considering markets it will enter is the extent of the nursing shortage and the ability to sign up healthcare providers for clinical rotations. Healthcare institutions gain highly efficient, low cost preferential access to a motivated and qualified pool of talent. Further, healthcare institutions have a say in the curriculum and can steep prospective hires in their culture before even hiring them. Orbis’s use of online classes gives important flexibility to the timing of rotations, which greatly increases the pool of possible instructors and eases the burden for healthcare partners.

Within days of the deal being announced, we had the chance to speak with the CEO and Founder of Orbis. We quickly realized the value of the business and the difficulty anyone would have in overcoming the head start and advances Orbis has accumulated over the last 15 years. We subsequently met a large chunk of the management team and came away impressed with the sense of mission, culture and management depth. Even ex-employees had glowing things to say.

Also, within a week of the closing of this acquisition, we were visiting with portfolio company Ensign Group which operates 200 skilled nursing facilities. A meaningful part of our conversation had to do with the challenges their entire industry faces associated with the nursing shortage. When we discussed the Orbis model and how it’s being acquired by Grand Canyon would accelerate the roll out of these programs into markets where Ensign operates and where Ensign could be a healthcare partner, the CEO got it immediately and described the program as “The Holy Grail” of nursing hiring for healthcare operators. We quickly put them in touch, and this interaction gives us valuable information but also shows how we are always trying to build trust and relationships with the management teams of our portfolio companies.

So, this is what we live for. A short-term oriented stock market thwacking the valuation of a company because reported earnings are going down slightly the next two or three quarters, despite the fact that this investment is, in our opinion, wildly accretive to the long-term value creation engine. We like the countercyclicality of the education space, and LOPE fits well into our portfolio. And it fits very well into our model – innovative, underleveraged, cash generative, extremely well run and grabbing share from challenged competitors who will always have difficulty catching up. We were thrilled to be able to add significantly to our position at depressed prices late in Q4 and early in Q1, and we are eager to see the growth at the main campus in Phoenix, at current Orbis partner campuses, and at new yet-to-be-announced educational institutions who choose to partner with, in our view, the only company who can provide a complete offering and who has a demonstrated track record of success at a large scale – Grand Canyon Education.

Closing Thoughts:

One of the highlights of the quarter was a trip to Seattle to meet with the management of Avalara at their HQ. The meeting had an interesting moment when the CFO asked me to repeat an element of our investment approach. As he requested, I repeated “we want to own companies whose competition is jacked up. Competition whose structure/culture/ownership or whatever makes it impossible for them to adapt/invest/attract talent or whatever is needed to compete effectively with the company we own.” The CFO jotted down “jacked up competition” and said something like “I like that a lot, and I’m going to start using that terminology because that exactly describes the situation with our competition.”

Avalara’s competition is indeed illustrative of what we look for. Their competition is doing fine and making money, but every day they are falling behind in much the same way Bed Bath & Beyond falls farther behind Amazon. We won’t get bogged down in it, but their competition includes the holy triad of slow-moving, sharelosing ownership. One competitor is family owned with 26 family members highly focused on getting their dividend checks quarterly. A second competitor is a cash cow buried inside a big conglomerate getting all the attention and love that less than 1% of corporate revenues should expect to get. The third competitor was bought a few years ago by a private equity firm that promptly loaded it with debt. In AVLR’s dynamic market, these competitors have fallen very far behind, cannot invest as needed to stop the gap from widening, and cannot retain the talent they would need to mount a credible challenge.

Similarly, how are small mid-tier universities with tenured faculty in areas no one cares about anymore and with no online presence, going to compete with Grand Canyon when Grand Canyon costs one third the price and is making all the investments to grow quality programs which it can offer both online and on ground? How are any of the thousands of independent flooring and tile guys going to compete over time with Floor & Decor’s incredible sourcing, merchandising, pricing, in-stock inventory and ability to service professionals? And so, it goes throughout our portfolio.

We love what we do because we spend our time talking to suppliers, customers, competitors, etc., so we can put the mosaic together and figure out the long-game. It’s fun and can drive great financial returns, but it can really only be done most effectively within a concentrated portfolio and with limits to capacity. Which is exactly why we think this analysis applies to our own business. We think we have the better mousetrap that other players cannot compete with because they have scaled and are trying to be all things to all people, which at some point leads to an index-hugging mindset and mediocrity. With their size, our larger peers will generate a lot more management fees than we do and will laugh all the way to the bank. But, we believe we will perform much better for our clients, which is the metric we care most about. And in the long run, maybe some very interesting things will happen for everyone.

Thank you for your support.

Gratefully,

Philip & the Owls Nest Partners team

Disclaimer

In General: This disclaimer applies to this document and the verbal or written comments of any person presenting it. This document has been prepared by Owls Nest Partners IA, LLC as Investment Adviser (the “Adviser”) of Owls Nest Partners Concentrated Long Only SMA (the “Strategy”). By receiving this document you acknowledge that you are an investor in the Strategy, or a prospective investor who is known to the Adviser, and that you meet all regulatory definitions of “Accredited Investor” and “Qualified Client,” in order to be considered a prospective client of the Adviser. The information included herein reflects current views of the Adviser only, is subject to change, and is not intended to be promissory or relied upon. There can be no certainty that events will turn out as the Adviser may have opined herein.

No reliance, no update and use of information: You may not rely on this document as the basis upon which to make an investment decision. To the extent that you rely on this document in connection with any investment decision, you do so at your own risk. This document is being provided in summary fashion and does not purport to be complete. The information in this document is provided you as of the dates indicated and the Adviser does not intend to update information after its distribution, even in the event the information becomes materially inaccurate.

Confidential information and distribution: By accepting receipt or reading any portion of this document, you agree that you will treat all information contained herein confidentially. Any reproduction or distribution of this document or any related marketing materials, as a whole or in part, or the disclosure of the contents hereof, without the prior written consent of the Adviser, is prohibited.

Suitability: Any investment program involves a high degree of risk and is suitable only for sophisticated investors who meet certain other suitability standards.

Investment strategies, market conditions and risk disclosures: Notwithstanding the general objectives and goals described in this document, readers should understand that the Adviser is not limited with respect to the types of investment strategies it may employ or the markets or instruments in which it may invest. Over time, markets change and the Adviser will seek to capitalize on attractive opportunities wherever they might be. Depending on conditions and trends in securities markets and the economy generally, the Adviser may pursue other objectives or employ other techniques it considers appropriate and in the best interest of the Fund. No representation or warranty is made as to the efficacy of any particular strategy or actual returns that may be achieved.

Projections: This document may contain certain “forwardlooking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of the Strategy’s investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

Disclosures

1. All “portfolio” information presented is for the Owls Nest Partners Concentrated Long Only SMA (the “Strategy”). Such data represents preliminary, unaudited, figures that are subject to change. The Adviser prepares final monthend and quarterly performance figures for the Strategy, which therefore represent its own internal, unaudited estimates of performance. Because the Strategy is only offered via separate account or SMA/UMA platforms, fees will be different for each client of the Strategy. Therefore, all performance returns are presented gross of all fees and expenses. For further information regarding Strategy performance, please contact the Adviser at info@owlsnestpartners.com, or by calling 484-352-1110.2. The Russell 2000 Total Return Index (the “Benchmark”) is a broad market index that is presented for comparative purposes as the performance benchmark to the Fund. The Benchmark is an unmanaged index consisting of the smallest 2000 stocks in the Russell 3000 Index. The stocks are issued in the United States, and the Benchmark includes the reinvestment of all dividends and income. Because the Benchmark is unmanaged, it assumes no transaction costs, management and performance fees, or other expenses. Unlike the Fund, it contains only domestic companies and is rebalanced monthly. Therefore, while the Benchmark contains publicly traded companies, it does not purport to represent an exact performance comparison to the Strategy. It is not possible to invest directly in an index, such as the Benchmark.