- Responsible for new idea generation; portfolio construction; risk management; due diligence

- 25+ years overseeing concentrated small-cap portfolios, on behalf of the most sophisticated allocators in the United States

- Previously: Founder, Endowment Capital Group; Portfolio Manager, Downtown Associates; Analyst, W.H. Newbold’s Son & Company

- University of Pennsylvania, Wharton School, B.S. 1986

- Married to Isabella, 3 sons, 3 daughters, 2 dogs

by Owls Nest Partners on Mar 31, 2020

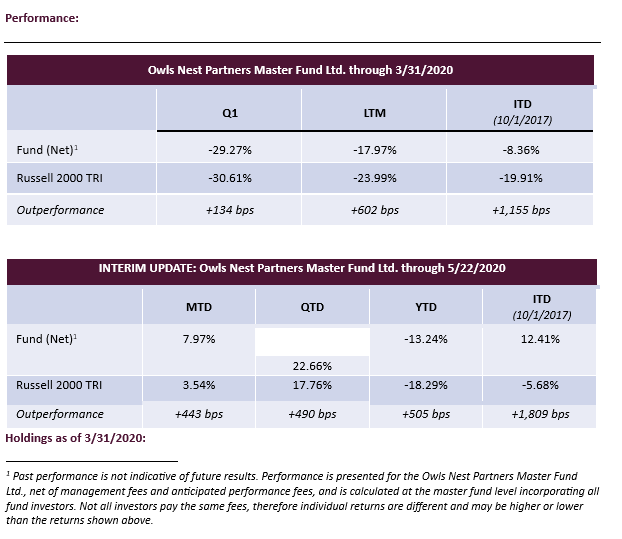

Quarterly Attribution:

It is almost impossible for us to discuss attribution in Q1 without breaking it down into airlines and everything else. Taken together, our investments in Allegiant Travel and Spirit Airlines were responsible for nearly half of our decline. Managing to outperform despite owning airlines makes it clear how well the rest of the portfolio held up, relatively at least.

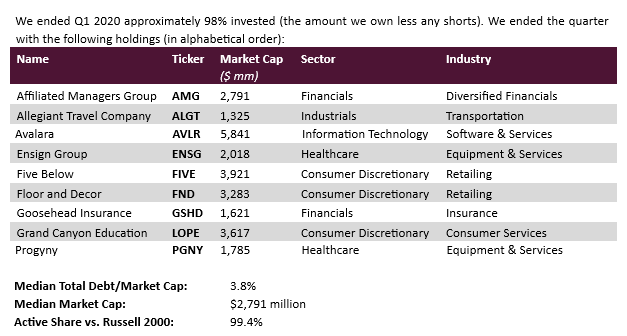

We had two stocks that were gainers in the quarter. Goosehead Insurance and Avalara, Inc. were slightly positive contributors. Our decliners, in order of smallest impact to largest, were FLIR Systems (FLIR), Progyny (PGNY), Five Below (FIVE), Grand Canyon Education (LOPE), Ensign Group (ENSG), Affiliated Managers Group (AMG), Floor & Decor (FND), Allegiant Travel (ALGT) and Spirit Airlines (SAVE). In general, short term market pressures and perceived near-term COVID impact overwhelmed any company-specific news. For example, Ensign Group had a stunningly good quarter and significantly raised their guidance, but the stock still closed down roughly 30% in the quarter. Needless to say, we added materially to that position.

Portfolio Adjustments:

We added two names in the quarter, and we sold two. The most important addition was Progyny (PGNY), a manager of fertility benefits for self-insured employers. Progyny attacks a major problem in healthcare benefit design to deliver incredible outcomes for employee members while actually saving the employer money and helping them recruit leading talent. With clear industry leadership, a huge head-start and only mid-single digit penetration of their immediate opportunity, Progyny is positioned to be in the portfolio for a very long time. With its business activity caught up in the postponement of all elective surgeries during quarantine, we were afforded a unique entry point into this high growth company. We will write extensively on PGNY in our next letter.

We also added Five Below (FIVE), a highly differentiated deep value discount retailer. FIVE sports tremendous unit economics and still has plenty of runway to grow. We will also discuss FIVE more in the July letter.

Selling Spirit Airlines was painful. It was a casualty of COVID. In early February they reported a very solid quarter consistent with our thesis and giving us, briefly, a very nicely profitable position. Then the world changed. Spirit’s enviable low-cost position stems from its heavy utilization of its equipment. With travel down so hugely and with no relief in sight and no certainty as to the depth and width of the abyss, we chose to sell and put the money to work in other names about which we could foresee greater gains with greater certainty. Selling Spirit begs the question “why hold on to Allegiant?”. We can answer that in great detail, but Allegiant’s low utilization, low-cost model and small and midsized market focus is the perfect model to not only survive this crisis but to play aggressive offense on the other side as they take advantage of industry capacity shrinking and many cheap used aircraft coming to market from distressed sellers.

We also sold FLIR Systems early in the quarter. A key part of our thesis was that the company would prune its product portfolio and sell off the parts that are non-core or where they are subscale, leaving behind a faster growing clear leader in infrared with a bright future. Management has been slow to execute this strategy, and ultimately it did not offer the upside that our other names with more organic growth offered.

Investment Program:

For the benefit of any first-time readers, the hallmark of the Owls Nest Partners approach is the purchase of industry leading growth companies when a temporary headwind has recoiled the fundamental growth drivers and compressed its multiple. This typically happens as hot money “renters” exit and drive the price down. There is no such thing as a free lunch: we can only receive our requisite value if we accept that our companies will appear “catalyst-less” and uninteresting for some time. We believe we are wildly overcompensated for this modest level of patience, especially since it is in these moments that a company can invest in its own business with the highest returns. There is wonderful optionality associated with a well-run, shareholder friendly, cashladen company that is able to aggressively put money to work during a temporary headwind.

It is our belief (and experience) that our future outperformance will not be driven by any economic or market forecasting prowess but instead by ten unique investments, each playing out over time. We perceive these investments to have modest downside due to high quality and low expectations, and very significant upside as growth and margin expansion return in spades. We seek reasonable ballast and diversification within the portfolio as a result of our natural conservatism (strengthened by our co-investment alongside clients) and our predisposition to avoid crowded trades and instead invest in temporarily out of favor areas.

Closing Thoughts:

We hope you understand why this letter is far more brief than normal. The feedback from the interim letters and notes during the quarter was very positive, and it certainly seems that an additional flowery letter was perhaps redundant and less important than using the time and energy to take advantage of the volatility to make real money. We promise you an unusually verbose letter next quarter. Is that a chorus of groans I hear?

The response from our clients during this crisis has been incredibly gratifying. We are happy to say we received no redemptions of any kind, and we had a number of clients add to their positions. As we write this, we are quickly approaching the peak in firmwide assets under management we had attained in early March.

Another highlight of the quarter was the addition of a new research analyst, Tyson Wilson to work with Sam Gudeon whom many of you have met. As you know, we hire for culture as much as we do for skills. No entitlement here. We can assure you that in hiring someone who worked so hard during rehab after a traumatic injury that he managed to get signed to an NHL contract, we have hired someone who is willing to work super hard to make sure every one of your dollars is working super hard for you.

A final highlight of the quarter was the hiring of Constellation Advisors to make sure our back and middle office are industrial strength as we grow. This hiring was especially well-timed in that it helped ensure no slippage in operational execution as we moved to work-from-home. In our line of work, work from home does not present any insurmountable challenges. During this period, our collaboration tools worked well, and we had little or no interruption in our research or operational processes. I guess, however, that it says something about our culture and team that I very much look forward to being back in the office with everyone every day, which apparently will happen by June 5.

We hope everyone is safe and well.

Without the right clients you are doomed to mediocrity. More than ever, we thank you for your support and for choosing to have your money working alongside ours.

Gratefully,

Philip & the Owls Nest Partners team

Disclaimer

In General: This disclaimer applies to this document and the verbal or written comments of any person presenting it. This document has been prepared by Owls Nest Partners IA, LLC as Investment Adviser (the “Adviser”) of Owls Nest Partners Concentrated Long Only SMA (the “Strategy”). By receiving this document you acknowledge that you are an investor in the Strategy, or a prospective investor who is known to the Adviser, and that you meet all regulatory definitions of “Accredited Investor” and “Qualified Client,” in order to be considered a prospective client of the Adviser. The information included herein reflects current views of the Adviser only, is subject to change, and is not intended to be promissory or relied upon. There can be no certainty that events will turn out as the Adviser may have opined herein.

No offer to purchase or sell securities: This document does not constitute an offer to sell (or solicitation of an offer to buy) any security and may not be relied upon in connection with the purchase or sale of any security.

No reliance, no update and use of information: You may not rely on this document as the basis upon which to make an investment decision. To the extent that you rely on this document in connection with any investment decision, you do so at your own risk. This document is being provided in summary fashion and does not purport to be complete. The information in this document is provided you as of the dates indicated and the Adviser does not intend to update information after its distribution, even in the event the information becomes materially inaccurate.

Knowledge and experience: You acknowledge that you are knowledgeable and experienced with respect to the financial, tax and business aspects of this presentation and that you will conduct your own independent financial, business, regulatory, accounting, legal and tax investigations with respect to the accuracy, completeness and suitability of this information, should you choose to use or rely on this document, at your own risk, for any purpose.

No tax, legal or accounting advice: This document is not intended to provide and should not be relied upon for (and you shall not construe it as) accounting, legal, regulatory, financial or tax advice, or investment recommendations. Any statements of U.S. federal tax consequences contained in this document were not intended and cannot be used to avoid penalties under the U.S. Internal Revenue Code or to promote, market or recommend any tax-related matters addressed herein.

Confidential information and distribution: By accepting receipt or reading any portion of this document, you agree that you will treat all information contained herein confidentially. Any reproduction or distribution of this document or any related marketing materials, as a whole or in part, or the disclosure of the contents hereof, without the prior written consent of the Adviser, is prohibited.

Suitability: Any investment program involves a high degree of risk and is suitable only for sophisticated investors who meet certain other suitability standards.

Investment strategies, market conditions and risk disclosures: Notwithstanding the general objectives and goals described in this document, readers should understand that the Adviser is not limited with respect to the types of investment strategies it may employ or the markets or instruments in which it may invest. Over time, markets change and the Adviser will seek to capitalize on attractive opportunities wherever they might be. Depending on conditions and trends in securities markets and the economy generally, the Adviser may pursue other objectives or employ other techniques it considers appropriate and in the best interest of the Fund. No representation or warranty is made as to the efficacy of any particular strategy or actual returns that may be achieved.

Projections: This document may contain certain “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of the Strategy’s investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

Disclosures

- All “portfolio” information presented is for the Owls Nest Partners Concentrated Long Only SMA (the “Strategy”). Such data represents preliminary, unaudited, figures that are subject to change. The Adviser prepares final month-end and quarterly performance figures for the Strategy, which therefore represent its own internal, unaudited estimates of performance. Because the Strategy is only offered via separate account or SMA/UMA platforms, fees will be different for each client of the Strategy, however the fees used for calculating net performance are annual management fees of 1%, and a 15% performance fee accrued on the outperformance to the Benchmark, over 5 years. For further information regarding Strategy performance, please contact the Adviser at info@owlsnestpartners.com, or by calling 484-352-1110.

- The Russell 2000 Total Return Index (the “Benchmark”) is a broad market index that is presented for comparative purposes as the performance benchmark to the Fund. The Benchmark is an unmanaged index consisting of the smallest 2000 stocks in the Russell 3000 Index. The stocks are issued in the United States, and the Benchmark includes the reinvestment of all dividends and income. Because the Benchmark is unmanaged, it assumes no transaction costs, management and performance fees, or other expenses. Unlike the Fund, it contains only domestic companies and is rebalanced monthly. Therefore, while the Benchmark contains publicly traded companies, it does not purport to represent an exact performance comparison to the Strategy. It is not possible to invest directly in an index, such as the Benchmark