- Responsible for new idea generation; portfolio construction; risk management; due diligence

- 25+ years overseeing concentrated small-cap portfolios, on behalf of the most sophisticated allocators in the United States

- Previously: Founder, Endowment Capital Group; Portfolio Manager, Downtown Associates; Analyst, W.H. Newbold’s Son & Company

- University of Pennsylvania, Wharton School, B.S. 1986

- Married to Isabella, 3 sons, 3 daughters, 2 dogs

by Owls Nest Partners on Mar 31, 2021

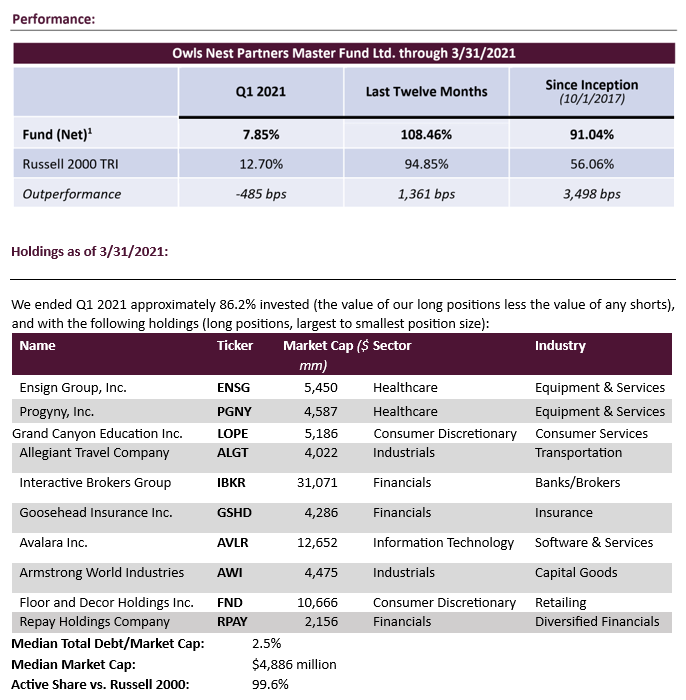

Q1 Attribution:

Most of our holdings were positive contributors in the quarter. The leading gainers, in order of largest impact to smallest, were Ensign Group (ENSG), Allegiant Travel (ALGT), Grand Canyon Education (LOPE), Interactive Brokers (IBKR), and Armstrong World Industries (AWI). The negative contributors, in order of largest impact to smallest, were Avalara (AVLR) and Goosehead Insurance (GSHD) which surrendered some of the large gains from last year and new position Repay Holdings (RPAY).

Q1 Portfolio Adjustments:

This most significant change in the portfolio was the addition of Repay Holdings which expanded the portfolio from nine companies to our usual 10. Consistent with our goal of having every dollar “work as hard as possible” for all of us, we also added to our Avalara position, which has been a recent relative underperformer (in terms of stock price, as opposed to in relation to how the business was performing compared to our expectations) while trimming the strongest stock performers slightly. The positions we pared included Ensign Group, Allegiant Travel, Floor & Decor (FND) and Progyny (PGNY).

On Distortions and Whipsaws:

A friend recently sold his pick-up truck. This normally uninteresting event was, in fact, very interesting and quite revealing of the state of our world. This friend is a general contractor in Florida, and his truck had been, using a phrase borrowed from the horse world, “ridden hard and put away wet.” Use and abuse aside, he sold his truck for $61k, nearly 15% more than he paid for it two years and 26,000 rough miles ago.

Markets are often distorted by some sort of short-lived, unusual force before settling back into something that resembles equilibrium. Although a great deal of energy, especially on Wall Street, is expended trying to exploit these anomalies, to us it is a dangerous game of musical chairs. Since, at some point, but no one knows when, the market will anticipate and price in the return to normalcy, and with that the second derivative of the graph will turn in the opposite direction. For long-term investors this is noise, but noise that can also provide good entry and exit prices.

2021 is shaping up to be the greatest year in our lifetime for distortions and noise. The issues are almost limitless, but most have to do with government policy and standard human behavior including short-term thinking on the part of many CEOs. Among the factors at work right now are unprecedented stimulus in the form of direct cash payments to citizens, aggressive short-term interest rate policy, huge pent-up demand in many areas of the economy, and supply chain shortages due to factories and shipping capacity all over the world being shuttered and employees being released during the pandemic. Now every business is struggling to find trained employees, shortages are everywhere, and commodity prices have soared with lumber prices, for example, nearly tripling the highest price ever recorded. And let us agree to not even discuss so called “meme” stocks or cryptocurrencies.

Against that backdrop what is one to do? Obviously, the first thing to do is to sell any cars you no longer need. Beyond that, we would say one should relax and keep a long-term view in mind.

Warren Buffett is out of favor these days, but he did pretty well for his investors in the inflationary and turbulent 1970s. One comment of his (paraphrased here) that sank in when I first read it and is especially relevant now and informs our strategy is this: “There are two types of investment opportunities where the company has pricing power. Great businesses with sustainable moats or businesses able to earn excess returns briefly due to a temporary shortage.” We are in the business of great businesses, not the temporary shortage business. Betting on pricing power due to shortage is a tough business made even tougher in a globally interconnected economy. It is also tough because in the real economy another Buffettism holds true – “the solution to high prices is high prices,” – meaning high prices attract capital and new and more efficient supply which ultimately drives prices down and often overshoot to the downside as supply comes onboard as demand is waning. Additionally, the market’s discounting mechanism is tricky. No market commentator is always right (which is why we limit our comments to these letters to partners…) but I always appreciated Joe Granville’s witticism, “if it’s obvious, it’s obviously wrong,” meaning that it would already be embedded in the stock’s or market’s price and expectations.

Playing the short-term shortage game can be doubly disastrous. First, it unnecessarily interrupts the magnificent compounding of great companies that are growing their share, profits, and long-term potential even if their stock is not the flavour du jour for some period. Second, it sets up the investor speculator for whipsaws which are particularly insidious because those losses are not nearly quotational but instead very real and permanent losses of capital.

We are very happy with our compounders, and if we are patient, disciplined and a little fortunate we should get some interesting opportunities on the back end of this distortion when frustrated speculators give up.

Repay Holdings (RPAY):

Before we jump into Repay specifically, a few words on “backwaters” which represent one of my favorite and most fertile investment paradigms. Backwaters are characterized by little energy or current compared to the main artery which is peripherally adjoined. Whether you are talking about them literally or metaphorically backwaters are not exciting. But backwaters can be beautiful. This spring I dragged three of my children to Madison, Wisconsin, which like most Americans they had not thought of since they memorized their state capitals in second grade. By the time they left, they were in awe of the town’s relaxed charm and beauty and even its stealth vitality. My high school senior daughter had applied to the University of Wisconsin only at my insistence and would have likely ended up going there, except for great news from Wash U in St. Louis. I knew Madison was beautiful and the only capital city on an isthmus, but I was stunned to learn that a bar across from the beautiful domed capital called The Old Fashioned had served over 1 million cocktails of the same name since its opening. Who says Madison is a boring backwater?

Similarly, certain niche markets can be described as backwaters, but also can be described as beautiful. We have a client, for example, whose business dominates the emergency exit sign industry. That may not sound exciting, but it has allowed him to become a generous pillar in his community, a great and active golfer, and wealthy enough to be a meaningful client of Owls Nest Partners. By any standard, that is a beautiful situation.

And the beautiful thing about backwaters is that they typically do not attract lots of new capital and competition. New competitors are unlikely to find an edge in a well-served slow moving industry, and hence their business plans are unlikely to show anything close to the returns needed to attract capital and talent. Dominating a small, slow moving, and ostensibly economically unattractive market is a little like controlling Oceania in Risk. It is generally easier to defend and keeps you alive, but the attention in the business community is focused on the person who controls a more sprawling empire like Asia, including the all-important Kamchatka.

In business, as in nature, backwaters are often caused by obstacles that block and interrupt the natural flow. And the funny thing about obstacles – whether boulders or a dam in a river, an established competitor in a marketplace or large armies based in Siam preventing you from expanding beyond your Oceania base in Risk – is that sometimes they move or are even destroyed. Sometimes gradually and sometimes suddenly. And when that happens, the backwater becomes part of the primary stream and in some cases even the dominant and most energetic means of progress.

Selling books is a real business, but certainly a backwater in the huge world of retail. But then something changed, and Amazon began its march to global hegemony. Looking at our own portfolio, for example: although Avalara had from its start this preposterously ambitious vision of being part of every commercial transaction anywhere in the world, it began life as a sales tax calculation engine for small businesses. Like shipping books to end consumers via UPS, this was, at that moment in time, a demonstrably small and unprofitable line of work. In Avalara’s case, this required an enormous effort to more or less manually build a tax content engine itemizing the tax rate on millions of items in thousands of taxing jurisdictions and update them continuously. It also required building integrations into hundreds of ERP and POS systems and even paying those integration partners a share of the revenue for any referred joint customer. And all of this was on top of trying to build slick software that can calculate all of this in milliseconds. The market was just too small to justify this investment. How many small businesses even did business in multiple tax jurisdictions? And frankly how many even cared about being truly compliant?

There were established players in the large enterprise market who had built the large content database and integrations with the handful of major systems and maintained their software for the big iron their big customers used. These guys followed the standard playbook. They diworsified into other areas or sold themselves to a many-headed conglomerate. They levered up and enjoyed dividends. They did not invest in this small unattractive backwater market. And then the boulder moved. E-commerce took-off. Even small and mid-sized businesses started doing business in multiple states and in hundreds or even thousands of tax jurisdictions. Suddenly, businesses wanted and needed their software to be in the cloud and real-time. And then the dam burst when the Supreme Court changed the definition of economic nexus and gave every tax jurisdiction the right to collect indirect taxes on essentially every company in the world selling into their jurisdiction. The backwater became a mighty and rapid river which will, in short order, subsume the former river navigated by the competitors caught flatfooted by the change. Moreover, Avalara’s ambitions, plans, and strategies have only expanded as they vow to never repeat their competitors mistakes borne out of complacency and a lack of vision.

The above simply serves as an introduction to our new investment in Repay Holdings Corp., a fast-growing electronic payments company. Taken as a whole, the electronic payments industry is vibrant, sizable, and extremely profitable. But even such a dynamic and attractive area has its backwaters. One such backwater has historically been the area of recurring payments on personal loans including car loans. Most people reading this probably have little recent experience with personal loans and are unaware that the payment networks Visa and Mastercard generally prohibit accepting credit cards for payment against personal loans. The standard practice has always been payment by check through the mail or cash or check in-person. As a result, few people even bothered to build an electronic payments program for personal loans. The use of debit cards was allowed, but debit usage was small compared to credit and the associated fees needed to drive payment processing profitability were a lot smaller. And building a robust payments platform to include all forms of payments and integrate that with the various lender back-office platforms was a lot of work. But believing that the adoption of debit would someday grow significantly, and that the status quo eventually would have to change, building such a payment platform for lenders is exactly what Repay decided to do.

The first earthquake that caused their obstacle inertia to move was the Global Financial Crisis. First due to tightened credit standards and then as a result of a generational behavioral shift among young people away from credit cards and the expensive revolving debt associated with them and toward debit cards and less expensive term debt. Repay’s consumer loan platform was suddenly in demand as consumers increasingly asked to pay with debit. As that activity scaled it became efficient and cost effective for lenders to accept debit. Businesses and lenders also began to realize the hidden costs of cash as it carries high administrative fees, higher security risk, lack of surety of funds, and a slower cash conversion cycle. Moving to an integrated electronic payments solution like Repay streamlines the manual clerical steps of processing physical payments while avoiding errors and providing quicker access to cash, which is particularly valuable to lenders who can now lend again and increase their velocity of funds. To expand their value proposition to businesses and consumers, Repay expanded its payment platform to accept payments (more or less) any way customers wish to pay including by web portal, mobile app, phone, and text.

Personal loan electronic payment penetration remains very low (below 20% compared to 67% for all U.S. consumer payments) and provides a long runway of growth on its own. However, the same dynamic and situation exists in other even larger areas within payments. Not only did Repay’s management recognize that they were in a great position to prosecute the broader opportunities within payments because of their technology, omnichannel payments platform, and wide ranging business system integrations, but so did the leadership of a special purpose acquisition company (SPAC) that was created by Pete Kight, who revolutionized the electronification of consumer banking in the 1990s as founder and CEO of CheckFree Corporation, and whose board included some of the most highly regarded executives in the payment industry. In 2019, the SPAC’s leadership concluded that Repay was the best opportunity in the payment space and merged with Repay giving the new Repay Holdings the financial and human capital and public company visibility to expand within its personal loan niche and expand that platform and vision into other areas where adoption of electronic payments was decades behind the adoption levels of standard consumer purchases. These underserved markets were attractive because of lower penetration of course, but also because solving the difficult challenges which led to the low penetration to start with would also create a stickier, less commoditized, and more profitable payments business compared to standalone merchant acquiring (the term used to describe the process of enabling merchants with very basic data needs to accept electronic payments).

Business to business (B2B) payments and consumer healthcare payments were targeted new areas because of their enormous size and because of their being very underpenetrated due to the complexity required and the reluctance on the part of businesses to pay standard interchange and processing fees when processing checks was “free”. Unlike standard merchant acquiring, B2B payments require a significant amount of additional data including associated invoice number, ship-from and destination zip code, itemized product code, freight amount, among many other datapoints. B2B payments also require building out a network of electronic connections to the millions of businesses in America in order to help them get paid faster and more efficiently. But the methodology needed to accomplish this daunting task was well understood by Repay’s board and management because Pete Kight had built out a first-generation version two decades earlier at CheckFree. Since entering the B2B payments space in 2019 through a small acquisition, B2B has already grown to 20% of the business and is growing greater than 25% organically. Repay is exercising particular strength around helping businesses automate accounts payable which allows their clients to improve cash flow management by enabling them to hold onto cash until the last second, get rebates and rewards similar to a consumer credit card, improve visibility into bills going out reducing fraud, and eliminates manual entry into an ERP system.

As for the other key additional growth vector, we all know how byzantine the world of healthcare payments is given the non-transparent nature of insurance coverage and charges. Integrating with the multitude of required parties is essential and is a formidable technical challenge to say nothing of building a payments platform that is easy for consumers to use and is unified across all the channels consumers may use for payments. The movement toward high deductible healthcare plans is driving great acceleration in consumer healthcare payments, to the extent that healthcare providers are buckling under the strain and seek to automate and accept electronic payments. Repay’s recent acquisition of BillingTree has given them a leading platform and solution, and the combined company should see enormous long-term organic growth as electronic payments become pervasive in healthcare.

COVID created various crosscurrents for Repay, some short-term in nature and some long-term. Long-term it is clearly a “boulder mover” accelerating the adoption of digital payments in its areas of focus. After all, it is hard to process checks if no one is allowed in the office and when the mail service is spotty at best. For example, Mercedes Benz like other auto dealers looked for more ways to digitally engage with their customers and quickly leaned on Repay to develop an omnichannel platform for accepting payments across their loan portfolio. The ability to build partnerships like this and the technology to make this process easy for consumers and robust and seamless for auto lenders in part through key integrations to the leading dealer management ERP systems, have helped drive greater than 20% organic growth in their auto loan repayment business, which has become the largest vertical in their business currently. We described above how the auto industry is going through interesting times right now, and we are delighted to participate in those higher price points and pent-up demand, not through owning a capital intensive, cyclical, auto manufacturer struggling with supply chain issues and persistent labor and cost issues, but instead through a capital-light company that will earn 40% margins facilitating the loan payments needed to buy those expensive new and used cars.

But COVID also had a short-term dampening on their personal loans business as many lenders tightened standards and shrank loan originations as COVID uncertainty waxed. At the same time, direct stimulus payments to consumers meant that fewer people needed loans, and in fact many used stimulus checks to pay off loans entirely. Repay had to announce a deceleration in its core business not long after coming public, and the investing community’s concern around this issue remains a depressant for the stock price as additional stimulus payments are made, even though lenders have clearly opened for business and consumers are clearly shopping again. This temporary headwind is quickly passing, but it has given us a great opportunity to accumulate a position in a company with high teens to 20%+ organic growth for as long as the eye can see, 40%+ EBITDA margins, 98% volume retention (well above the 75% average retention for traditional merchant acquiring), and a leading position in markets in the second or third inning of their development. And given the moat that they built while others disregarded these backwater markets including the 175+ key software integrations, cloudbuilt vertical-specific technology, and growing network effects from having 60,000+ suppliers on their B2B platform, we can only see their position strengthening over time.

Investment Program:

For the benefit of any first-time readers, the hallmark of the Owls Nest Partners approach is the purchase of industry leading growth companies when a temporary headwind has recoiled the fundamental growth drivers and compressed its multiple. This typically happens as hot money “renters” exit and drive the price down. There is no such thing as a free lunch: we can only receive our requisite value if we accept that our companies will appear “catalyst-less” and uninteresting for some time. We believe we are wildly overcompensated for this modest level of patience, especially since it is in these moments that a company can invest in its own business with the highest returns. There is wonderful optionality associated with a well-run, shareholder friendly, cashladen company that is able to aggressively put money to work during a temporary headwind.

It is our belief (and experience) that our future outperformance will not be driven by any economic or market forecasting prowess but instead by ten unique investments, each playing out over time. We perceive these investments to have modest downside due to high quality and low expectations, and very significant upside as growth and margin expansion return in spades. We seek reasonable ballast and diversification within the portfolio as a result of our natural conservatism (strengthened by our co-investment alongside clients) and our predisposition to avoid crowded trades and instead invest in temporarily out of favor areas.

Closing Thoughts:

We hope you and your family remain safe and well.

More than ever, we thank you for your support and for choosing to have your money working alongside ours.

Gratefully,

Philip, David & the Owls Nest Partners team

PS – If you’ve never been to Wisconsin, it’s worth going for the cheese curds alone. Grab a statin first, however.

Disclaimer

In General: This disclaimer applies to this document and the verbal or written comments of any person presenting it. This document has been prepared by Owls Nest Partners IA, LLC as Investment Adviser (the “Adviser”) of Owls Nest Partners Concentrated Long Only SMA (the “Strategy”). By receiving this document you acknowledge that you are an investor in the Strategy, or a prospective investor who is known to the Adviser, and that you meet all regulatory definitions of “Accredited Investor” and “Qualified Client,” in order to be considered a prospective client of the Adviser. The information included herein reflects current views of the Adviser only, is subject to change, and is not intended to be promissory or relied upon. There can be no certainty that events will turn out as the Adviser may have opined herein.

No offer to purchase or sell securities: This document does not constitute an offer to sell (or solicitation of an offer to buy) any security and may not be relied upon in connection with the purchase or sale of any security.

No reliance, no update and use of information: You may not rely on this document as the basis upon which to make an investment decision. To the extent that you rely on this document in connection with any investment decision, you do so at your own risk. This document is being provided in summary fashion and does not purport to be complete. The information in this document is provided you as of the dates indicated and the Adviser does not intend to update information after its distribution, even in the event the information becomes materially inaccurate.

Knowledge and experience: You acknowledge that you are knowledgeable and experienced with respect to the financial, tax and business aspects of this presentation and that you will conduct your own independent financial, business, regulatory, accounting, legal and tax investigations with respect to the accuracy, completeness and suitability of this information, should you choose to use or rely on this document, at your own risk, for any purpose.

No tax, legal or accounting advice: This document is not intended to provide and should not be relied upon for (and you shall not construe it as) accounting, legal, regulatory, financial or tax advice, or investment recommendations. Any statements of U.S. federal tax consequences contained in this document were not intended and cannot be used to avoid penalties under the U.S. Internal Revenue Code or to promote, market or recommend any tax-related matters addressed herein.

Confidential information and distribution: By accepting receipt or reading any portion of this document, you agree that you will treat all information contained herein confidentially. Any reproduction or distribution of this document or any related marketing materials, as a whole or in part, or the disclosure of the contents hereof, without the prior written consent of the Adviser, is prohibited.

Suitability: Any investment program involves a high degree of risk and is suitable only for sophisticated investors who meet certain other suitability standards.

Investment strategies, market conditions and risk disclosures: Notwithstanding the general objectives and goals described in this document, readers should understand that the Adviser is not limited with respect to the types of investment strategies it may employ or the markets or instruments in which it may invest. Over time, markets change and the Adviser will seek to capitalize on attractive opportunities wherever they might be. Depending on conditions and trends in securities markets and the economy generally, the Adviser may pursue other objectives or employ other techniques it considers appropriate and in the best interest of the Fund. No representation or warranty is made as to the efficacy of any particular strategy or actual returns that may be achieved.

Projections: This document may contain certain “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of the Strategy’s investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

Disclosures

- Performance presented from inception through September 2020 is for a representative account of the Owls Nest Partners Concentrated Long Only SMA strategy (the “Strategy”). As of October 2020, performance is for a composite of separately managed accounts managed in accordance with the Strategy (the “Composite”). Performance is presented gross and net of all fees, as of the date listed at the top of this document. The fees applied are the prevailing fees of the Strategy at the time such performance was generated. From inception to the date of this document, the fee structure applied is a 1% annual management fee, and 15% performance fee that is charged only on the outperformance of the Strategy to the Benchmark (as defined below), and only after five years. Performance fees are accrued monthly. The vehicle for the Strategy is a separately managed account. All performance is calculated by the Adviser. Further information regarding the Strategy or the Composite can be provided upon request. The Adviser does not claim compliance with the GIPS reporting standards and the performance presented herein has not been audited or verified by any third-party. The Russell 2000 Total Return Index (the “Benchmark”) is a broad market index that is presented for comparative purposes as the performance benchmark to the Fund. The Benchmark is an unmanaged index consisting of the smallest 2000 stocks in the Russell 3000 Index. The stocks are issued in the United States, and the Benchmark includes the reinvestment of all dividends and income. Because the Benchmark is unmanaged, it assumes no transaction costs, management and performance fees, or other expenses. Unlike the Fund, it contains only domestic companies and is rebalanced monthly. Therefore, while the Benchmark contains publicly traded companies, it does not purport to represent an exact performance comparison to the Strategy. It is not possible to invest directly in an index, such as the Benchmark.

- The Russell 2000 Total Return Index is the performance benchmark for the Strategy (the “Benchmark”). The Benchmark is a domestic equity market index of the 2,000 smallest companies by market capitalization in the Russell 3000 Index. Because the Benchmark is unmanaged, it assumes no transaction costs, management fees or other expenses. The calculation of the benchmark return includes the reinvestment of all dividends. It is not possible to invest directly in an index, such as the Benchmark, and therefore it is presented here for information purposes only.