- Responsible for new idea generation; portfolio construction; risk management; due diligence

- 25+ years overseeing concentrated small-cap portfolios, on behalf of the most sophisticated allocators in the United States

- Previously: Founder, Endowment Capital Group; Portfolio Manager, Downtown Associates; Analyst, W.H. Newbold’s Son & Company

- University of Pennsylvania, Wharton School, B.S. 1986

- Married to Isabella, 3 sons, 3 daughters, 2 dogs

by Owls Nest Partners on Mar 31, 2022

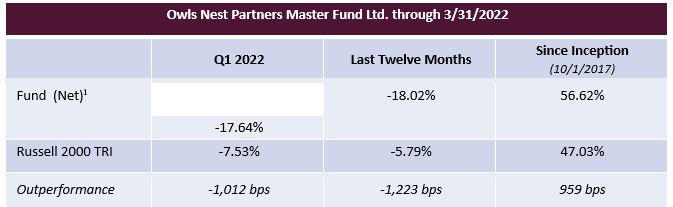

Performance:

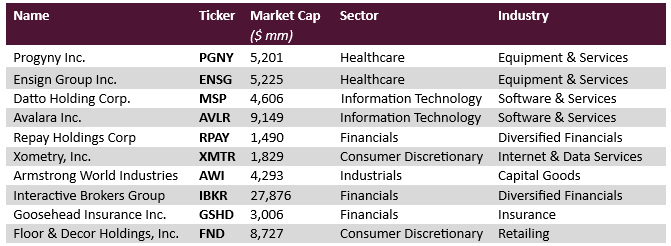

Holdings as of 3/31/2022:

We ended Q1 2022 approximately 100.3% invested (the value of our long positions less the value of any shorts). We ended the quarter with the following holdings (in order of position size, largest to smallest):

Median Total Debt/Market Cap: 3.5%

Median Market Cap: $4,904 million

Active Share vs. Russell 2000: 99.6%

1Past performance is not indicative of future results. Performance presented from inception through September 2020 is for a representative account of the Owls Nest Partners Concentrated Long Only strategy (the “Strategy”). As of October 2020, performance is for a composite of accounts managed in accordance with the Strategy (the “Composite”). Please see the Disclosures at the end of this document for further information with regards to performance.

Quarterly Attribution:

During the quarter, we had three gainers and eight decliners. The gainers were modest and included defensive healthcare related names. The positive contributors, in order of largest impact to smallest, were Ensign Group (ENSG), Progyny (PGNY), and Datto (MSP). The largest declines came in anything perceived to be tied to the housing cycle irrespective of their strong underlying fundamental performance. The negative contributors, in order of largest impact to smallest, were Goosehead Insurance (GSHD), Xometry (XMTR), Floor & Decor (FND), Armstrong World Industries (AWI), Avalara (AVLR), Interactive Brokers (IBKR), Repay (RPAY), and Allegiant Travel (ALGT).

Portfolio Adjustments:

During the quarter, we sold our Allegiant position as discussed below. On the margin we lightened up on the relatively strong performers (Ensign most significantly) to redeploy the proceeds into new position Xometry (discussed below) and into more beaten-up names including Avalara, where we feel the fundamentals are accelerating, especially relative to the expectations implied in the stock price.

Intro to Xometry – A quick reminder on Why We Do What We Do and Why, Together, We Win:

You do not own some nebulous financial asset. What you own is a portion of ten businesses that are solving very real and sizable problems in unique ways and getting better, stronger and more valuable as they do that.

Anyone who has ever spoken with us knows how much we enjoy our research process. Other firms often have a top-down approach in which smart people in tall buildings come up with some thesis and employ analysts to go out and find supporting material and ways to invest or speculate in a manner consistent with that thesis. This approach can make for convincing copy, but, to us, it drives a difficult and dangerous investment process. Our approach is the opposite. We always want to maintain an open mind, and we are unwilling to risk our capital based on our simply being smarter than others as we interpret readily available information. Instead, from the second floor of a building we go out and learn from the people in the real economy who know what is actually going to happen, at least as relates to what products or services they are going to buy or not buy and why, where the talent in their industry is going, what problems remain unsolved, and what the risks are for the various players in the market.

We do the pick and shovel detective work of gathering all the necessary pieces of the mosaic and then arrange and rearrange the pieces until a clear image emerges. It is a lot of work, but “You have to carry a big basket to bring something home.”2 It is great fun learning all day, and it is exciting and rewarding when the pieces come together into a logical design. Our skill is not some innate ability to predict the future but rather lies in knowing what questions to ask, recognizing patterns and synthesizing.

To be clear, while we talk about fun, we do this to win. And we think the “game” we play is a much easier game to win than the “I’m the smartest guy in the room” game. We also put ourselves in a highly advantaged position to win since we are, by design, capacity-constrained, highly concentrated and only available to true long-term oriented investors. So, together, we are among the very few investors who can truly minimize risk and maximize growth of our capital by doing in-depth, long-term oriented, primary research on less well-known and less liquid durable growth companies that have strong positions today and nearly inexhaustible room to grow long into the future.

As a case in point, Xometry was not our primary target when we started sniffing around its industry. We were working on a competitor of sorts whose stock price and expectations had come down very significantly over the last two years. We knew that that company enjoyed a solid reputation in its industry and still possessed only a small part of a large market that theoretically could be in reach. Perhaps there was an opportunity for a reacceleration which could drive the stock much higher.

But customer after customer kept saying of the initial target, “they’re fine, and there’s a role for them, but the world is moving quickly in the direction of this other guy who has a totally different offering that makes our lives so much easier and solves a big problem for us. That’s who we’re moving to, and that’s who we are going to rely on in much larger ways going forward.” Our process allowed us to avoid the dreaded value trap landmine and uncover a growth company gem instead.

2 David Epstein (2019). Range: Why Generalists Triumph In A Specialized World, page 153. A really enjoyable and thoughtprovoking work. growth of our capital by doing in-depth, long-term oriented, primary research on less well-known and less liquid durable growth companies that have strong positions today and nearly inexhaustible room to grow long into the future.

Xometry (XMTR):

Any company’s opportunity and ultimately its value is a function of the size of the problem it is solving and the enduring uniqueness of their solution. With the creation of its on-demand digital marketplace for manufacturing, Xometry solves three enormous and thorny problems in genuinely unique ways that will only grow more compelling as scale and network effects kick in.

Problem 1:

There are more than 625,000 manufacturing shops in the U.S. alone, and 75% of them have 20 or fewer employees and almost no cost-effective way to tap into demand outside of their local market. They also typically lack the proper technology to manage their business, relying instead on spreadsheets and clipboards. They also have little access to convenient financing tools to alleviate significant working capital needs.

Problem 2:

Everyday tens of millions of people globally use AutoCAD and other computer aided design (“CAD”) packages to design new things or components of things, but they have no precise knowledge of what their new thing will cost to manufacture since it has, by definition, never been built before.

Problem 3:

Most consumer services have been digitalized creating vast empires along the way for the likes of Amazon, Google, and Apple. But manufacturing has yet to be digitalized. When you design something, figuring out who has the expertise and capacity at that moment to build it to your specifications and on your timeline is a manual, time-consuming process that fundamentally fails to discover new and better sources of capacity and, hence, best available pricing.

Xometry is uniquely solving these huge problems by:

- Creating and qualifying a curated network of suppliers across all relevant manufacturing

methodologies, - Creating the first real-time pricing tool for newly designed products, and

- Creating the first large scale digital marketplace where customers can instantaneously purchase a desired quantity of a newly designed product at specified tolerance levels, turnaround time, and with all necessary certifications across all major manufacturing modalities.

The Supplier Network

Xometry currently has more than 2,000 active suppliers in its network, mostly based in the United States although the build out of the network is underway in Europe and Asia. The appeal to join the network for a manufacturer is obvious. Once you are vetted and demonstrate quality and reliability through test runs you have access to orders you would never otherwise see. Xometry offers each new order it receives to a subset of their network based on prior performance and qualifications. The marketplace is voluntary to suppliers. If they are busy and do not need work, they can ignore it and someone else will jump at those orders. The first supplier to accept the specifications and pricing gets the order and gets to work. The pricing offered to suppliers is the price Xometry quoted to the purchaser less Xometry’s take-rate which can vary but averages close to 25% and continues to trend higher as Xometry leverages AI/machine learning and expands their supplier network. Sorry for the buzzwords, but it is a real and powerful application of the technology. As the owner of the largest, by far, relevant data set, Xometry is in a privileged position to apply AI/machine learning to get better at its initial pricing to customers and estimating their cost of production.

The beauty of these orders to a supplier lies in the fact that most manufacturing is very much a fixed cost business. The cost is in the equipment, and labor is largely fixed. If you have idle equipment, it makes sense to take any order that offers any substantial revenue beyond the cost of production. The marketplace is voluntary to suppliers. If they are busy and do not need work, they can ignore it and someone else will jump at those orders. Importantly, orders from Xometry have no sales and marketing expense. There are no salespeople to pay. We have spoken to manufacturers who have launched businesses around Xometry. They bought the equipment and never hired a salesperson because they knew they could just pick their orders off the Xometry job board. Other suppliers indicated that this order flow will give them the confidence to buy more equipment and grow their business.

Xometry also helps their suppliers in other ways. They offer fast, competitively priced supplies and raw materials, and utilizing their data and positioning they offer accelerated payment terms for a fee against any orders in process. Through their recently acquired Thomasnet division they offer manufacturers complete digital marketing services, e-commerce solutions, analytics, and the ability to advertise in Thomasnet, the largest industrial directory with 1.3 million registered users searching for suppliers each month.

Xometry recently acquired FactoryFour, a powerful but easy to use manufacturing execution system. FactoryFour software replaces clipboards and spreadsheets and helps manufacturers plan their capacity, enhance process control, and optimize order execution. Xometry has integrated Thomasnet and the Xometry marketplace into FactoryFour and will shortly release the combined offering on a freemium basis to any manufacturer. With these integrations, FactoryFour will make accepting and managing Xometry orders extremely easy for suppliers and further embed Xometry in their workflow.

Providing all these solutions to manufacturers and embedding them in their workflow strategically ensures that Xometry will be able to grow its supplier base as needed to meet the ever-increasing demand generated in its digital manufacturing marketplace. And as the provider of the leading tools for revenue generation, operational control, and digital marketing, Xometry is positioned as both the Shopify and the Google for the enormous and fragmented universe of small and mid-sized manufacturers.

The Pricing Engine

The ability to offer buyers an instant price for never produced items that only exist in CAD files is the lynchpin of the entire Xometry offering. Without instant pricing, Xometry would just be an interesting bulletin board and the buying process would be challenged by significant friction. Pricing a pack of Duracell batteries is simple for Amazon or Walgreens, while pricing something that doesn’t exist is complex and error prone, particularly for items requiring tight tolerances, short timelines, and for demanding applications like aerospace and defense.

By being a pioneer with this vision, Xometry has built the widest and deepest database of custom manufactured items and their cost, across virtually every manufacturing modality. The head start from millions of datapoints, the years of focused R&D, tactical acquisitions to complete the offering, and the losses accumulated building the brand, awareness and all other aspects of the business have cemented their preeminence. It would seem very difficult to make the business case to try to copy Xometry with a manufacturing pricing model, especially in today’s business and stock market climate. You’d be begging for losses, and how would you even do it without an established supplier base who actively engages with you? And how would you refine the model without any real-world orders? And how would you ever catch up to Xometry who will keep getting sharper with better tools for this focus and an ever-growing supplier base?

The Xometry pricing engine is so useful and unique that many engineers told us that the term “Xometry it” has come to mean get pricing in the engineering/design world. Even if you are not ready to buy but want to know the cost and manufacturability, just download the file to Xometry and learn the cost, a process which embeds Xometry as a useful part of the design process. Through Xometry you can quickly learn what would happen to cost if you tweaked the design, the material, the tolerances, or changed the manufacturing modality.

In solving this pricing challenge, Xometry is effectively the New York Stock Exchange of custom manufacturing.

The Digital Marketplace for Custom Manufacturing

Even if you are suspicious of Amazon’s power, root for others to somehow surpass them, and actively dislike Jeff Bezos when he wears cowboy hats into space, you have to admire what Amazon has done to make it super easy for consumers to buy everything they could possibly want. It is the bar by which all other shopping experiences are judged. Nothing approaching that experience existed in custom manufacturing prior to Xometry. Companies with narrow offerings especially in easy to execute modalities such as 3D printing could offer a reasonably good experience, but that is akin to a 1997 Amazon experience when they only sold books. Such limited offerings lack any clear savings since the nature of the item makes price comparison difficult and by being captive to that one company, these offerings can never benefit from having hundreds or thousands of suppliers essentially compete for the assignment thereby driving down the cost to build for the customer.

Long-time readers may already recognize a favorite Owls Nest theme at work here. There are few business models better than being the trusted conduit through which an impossibly fragmented supplier base reaches an infinitely fragmented customer base. 60% of Amazon orders are third-party where Amazon simply connects and provides confidence to the buyers and provides other services for related fees to the supplier. Apple is the toll taking intermediary between content and app creators and the 1 billion iPhone users. Google is…well…Google it. Floor and Decor’s merchants connect nameless, faceless manufacturers all over the world with hard surface flooring customers who don’t care about the manufacturer but love the merchandising, breadth of product, value and in-stock position at Floor &Decor. Goosehead functions in the same way in the personal lines insurance industry, and Avalara connects businesses of all shapes and sizes to the 14,000 US sales tax jurisdictions.

From the perspective of a product engineer who needs custom manufacturing services, think of the challenges of procuring and managing your supplier base. The underlying challenge that can never be solved without Xometry is that design engineers need a range of capabilities that no single manufacturer can provide. Xometry’s current menu covers 70 different materials, 15 different manufacturing processes, all necessary certifications and traceability requirements, and even carbon offset programs. Beyond that, it is impossible to be certain that any particular partner will have capacity when you need it. With Xometry there is always capacity. You will never need to find another supplier; Xometry does that for you. And there is always a sophisticated, trusted, financially strong partner with hundreds of millions of dollars in cash standing behind your order, while any individual small supplier may ultimately prove unstable. And there is always fair to exceptional pricing. It begs the question: why wouldn’t you just use Xometry?

The alternative to using Xometry is calling around to a bunch of people, seeing who has capacity, sending them the file, finding out how long they will need to do it, and negotiating on price. Even if you don’t have to qualify a new supplier, this process alone can take weeks. If you are busy trying to get a new product to market ahead of the competition, do you want to spend weeks on this when instant, easy, fully certified, and better pricing is readily available?

The Xometry marketplace is leading the digitalization of manufacturing. Xometry is, dare we say, the Amazon of custom manufacturing.

The long-term opportunity for Xometry is ridiculously large for a company with barely a $1 billion enterprise value. The biggest immediate opportunity is penetration of existing accounts of which there are already more than 30,000 active buyers on the platform. 95% of the revenue in any given quarter comes from prior existing customers. The advocates and evangelists are building up. Getting a few engineers that have used and loved Xometry inside a place like Lockheed Martin to grow to hundreds or thousands is not rocket science, and Xometry has been building out a direct salesforce to accomplish that now that it has proven its ability to deliver and scale. Overall, marketplace revenue will grow between 50-60% this year, and the number of accounts with over $50,000 of revenue is growing even faster. Total penetration and domination of a market as large as North American, European, and Asian custom manufacturing won’t happen overnight. People change habits slowly. I still read physical newspapers to the utter consternation of my children, for example. Digitalization, however, just makes too much sense, the timing is right, and Xometry’s clear vision and head start will make them difficult to unseat. That said, it may not take as long as it would otherwise because the current supply chain trainwreck has focused a very bright light on the need for flexible and resilient supply chains including domestic options. There is even a national security element to Xometry’ s value proposition since it greatly facilitates the onshoring of critical manufacturing.

Xometry is exciting, but it is just one of your ten that share common characteristics: experienced, visionary and aligned management teams solving huge problems in unique ways and armed with a resilient business model and a great balance sheet to ensure they can exploit their full opportunity. They will do well in great times and accelerate their share gains in bad times. Turbulent times like these with labor challenges, inflation, supply chain issues only play into Xometry’s strength as companies need to re-evaluate all their business practices. When you are disrupting (oops, buzzword again) a huge industry, you want people asking, “is there a better way?”. While the market cooldown is disquieting to all but the most stoic and long-term oriented, the collapse of growth stock valuations and the “not yet making money” economy has allowed us to buy XMTR stock at a fraction of last year’s price and has stuck a fork in any early-stage would-be competitors whose businesses or talent are now ripe for poaching on attractive terms.

I love creative destruction. I love that ours is an investment approach grounded in the real-economy and not in stock market mumbo jumbo, black boxes, or theoretical economic models that provide no comfort when challenged in bad times. I love that each of our companies makes our country a little better and a little more competitive in their own ways. And we get to partner with them and profitably participate. It’s a great job; it’s a great country.

Allegiant Travel (ALGT):

Ours is often a process of understanding the incremental changes on the margin. We are not necessarily trying to anticipate or bet on every short-term machination, but instead we try to appreciate when the long-term opportunity and positioning starts to change. We sold Allegiant Travel during the first quarter because, while its prospects remain strong, on the margin the thesis was starting to be challenged.

Maury Gallagher, Allegiant’s very entrepreneurial CEO and one of my favorites, summed up the root cause perfectly when I asked about him about building his fleet for future growth. He may have intended it as just a throwaway comment at the time, but he confided, “Philip, there’s just too much money out there chasing everything, including planes.”

Our expectation was that with its very liquid balance sheet and as one of the few domestic carriers who was profitable in 2021 and who didn’t have to repay any COVID-related borrowings from the government, Allegiant would be able to lock up the capacity they needed for growth at very good prices, perhaps even once-in-ageneration type fire sale prices. After all, Ryanair’s great success over the last 20 years stemmed in a meaningful part from a great deal to buy aircraft that was available due to the turmoil after 9/11. In early 2021, Allegiant was able to strike some very attractive deals on used but still young Airbus A320s with prices down 40% from pre-COVID levels as European carriers culled their fleets or went bankrupt. But soon prices bounced, and the ability to do anything of scale evaporated. Ultimately, Allegiant made a shrewd deal to buy a substantial number of new planes from Boeing who was having its own troubles and was in a mood to deal. The economics of the purchase are compelling, but it introduces undesirable new complexity and possible inefficiencies into the Allegiant system since they are presently an all-Airbus fleet.

The flow of capital into the industry also allowed for new, opportunistic entrants including Breeze, started by JetBlue founder David Neeleman, and Avelo, started by former Allegiant President Andrew Levy, whom we know well and respect and who may be reading this letter right now too. Breeze and Avelo are still small and have different models and target markets and won’t have any immediate impact on the market. But years from now, it’s possible that they would at least be skimming some of Allegiant’s growth, and it was always best to have a competitive set made up largely of much higher cost operators, especially those with customer-unfriendly hub and spoke models.

Lastly, business travel is returning, but its return to pre-pandemic levels is uncertain and distant. Allegiant is a pure leisure travel model, but the impact on Allegiant is that capacity that would otherwise be used by legacy competitors for business travel may end up being used for leisure travelers who might otherwise have flown Allegiant. The industry faces other challenges now including fuel prices and labor shortages, but those will in some ways help Allegiant gain share and weren’t really a factor in our decision to sell.

Allegiant was a profitable investment for us despite a crippling pandemic, and it still has a bright future and a very capable management team. But we always want the highest quality portfolio made up of the most differentiated companies, and we want every dollar working as hard as possible. The world is a fascinatingly dynamic place. As Warren Buffett once said, “if past history was all there was to the game, the richest people would be librarians.”

Fortunately, that in-depth primary research process which helped us identify Xometry also helps us stay on top of positions as things inevitably evolve. Exploring new ideas is great fun, but protecting our capital and challenging our thesis on portfolio companies is the most important job we do. All the work that has come before is ancient history and a sunk cost. All that matters is what lies ahead. And for the ten companies you own, the future looks very bright indeed.

Applying Lessons Learned in the Field:

For businesses, including our own, that require investment and talent to compete, there is a lot of truth in the mantra “grow or die.” Profitable growth ensures access to the necessary resources and the career paths to retain and nurture the talent. That said, growth done badly is the surest and fastest way to die.

We’ve been blessed with great examples of how and when to grow. Ensign and Floor & Decor, for example, work as hard at developing the future managers on the bench as they do anything else since they know that even a single poorly run operation is not the absence of a positive but a very substantial negative. Goosehead CEO Mark Jones betrays his prior life as a Bain partner when he says he has to measure and develop the company’s “absorptive capacity” to ensure highly productive growth.

In contrast we see examples of the destructive power of growth done badly. Fortunately, our investment program keeps us away from the biggest chunks of kryptonite for growth companies – betting on the unsustainable tailwind (anyone want a deal on a Peloton bike?) and the dumb acquisition done for growth’s or ego’s sake (endless examples). But simply growing beyond your capacity to manage can be just as sinister.

Last year we looked at a promising healthcare service company. It was a leader in a rapidly growing delivery methodology aimed at taking care of society’s most vulnerable citizens, those that are dually eligible for both Medicare and Medicaid and have a long list of complications. It was almost universally agreed that this type of program (called PACE) delivered superior care, much happier patients and even lowered costs for the system. The industry was historically a fragmented group of not-for-profits, but rule changes made it possible for wellcapitalized for-profit entrants. The first player with the capital to expand organically, the ability to leverage best practices and overhead efficiencies, and the ability to consolidate the space would enjoy a great advantage in a vastly underpenetrated and growing market. The stock was statistically cheap and screened like a champ. The publicly available literature and the Wall Street primers were all very positive.

We dug in. And then the fireworks began. We heard consistent stories about how the business expanded aggressively without sufficient controls in place and without the leaders or even line workers to deliver the promised service. People who loved the mission fled the company because they couldn’t stand to be part of something that didn’t treat its clients or the government agencies who paid with respect. Important front-line positions went unfilled to hit short-term profit targets. The company felt the need to grow and even bought a company against the advice of the internal employee assigned to do the due diligence who was concerned about the lack of controls. Once again, the primary research process separated the wheat from some very nasty chaff. Since we stopped work, the company has fired the CEO and the Chief Medical Officer, and several states have suspended the company’s ability to add patients pending investigations. And this was a company that had come public with a $3.5B valuation in a highly regulated industry and backed by an extremely well-known PE shop. If they can screw up growth so monumentally, any company can if they don’t respect the risks.

These examples, as well as our own experiences, powerfully inform our thinking about our own growth. Although we still have more than $200 million of capacity before we close to new clients, we will temporarily close starting July 1 through next January 1. This is a pause to reassess vendors, review all operational procedures and generally make sure we are well prepared for our next leg of growth.

One of the items we will review is the client relations/communications program. I hope you can spare a couple minutes when you get that call or email to let us know how we can best serve your needs and what you would like to see and what you don’t need to receive. We also look forward to the return to seeing everyone in person.

Investment Program:

For the benefit of any first-time readers, the hallmark of the Owls Nest Partners approach is the purchase of industry leading growth companies when a temporary headwind has recoiled the fundamental growth drivers and compressed its multiple. This typically happens as hot money “renters” exit and drive the price down. There is no such thing as a free lunch: we can only receive our requisite value if we accept that our companies will appear “catalyst-less” and uninteresting for some time. We believe we are wildly overcompensated for this modest level of patience, especially since it is in these moments that a company can invest in its own business with the highest returns. There is wonderful optionality associated with a well-run, shareholder friendly, cashladen company that is able to aggressively put money to work during a temporary headwind.

It is our belief (and experience) that our future outperformance will not be driven by any economic or market forecasting prowess but instead by ten unique investments, each playing out over time. We perceive these investments to have modest downside due to high quality and low expectations, and very significant upside as growth and margin expansion return in spades. We seek reasonable ballast and diversification within the portfolio as a result of our natural conservatism (strengthened by our co-investment alongside clients) and our predisposition to avoid crowded trades and instead invest in temporarily out of favor areas.

Final Thoughts:

We hope you and your family remain safe and well.

More than ever, we thank you for your support and for choosing to have your money working alongside ours.

Gratefully,

Philip & the Owls Nest Partners team

P.S. Here is a link to a 3-minute video explaining the Xometry marketplace if you would like to see how they describe it from the customers perspective.

Disclaimer

In General: This disclaimer applies to this document and the verbal or written comments of any person presenting it. This document has been prepared by Owls Nest Partners IA, LLC as Investment Adviser (the “Adviser”) of Owls Nest Partners Concentrated Long Only SMA (the “Strategy”). By receiving this document you acknowledge that you are an investor in the Strategy, or a prospective investor who is known to the Adviser, and that you meet all regulatory definitions of “Accredited Investor” and “Qualified Client,” in order to be considered a prospective client of the Adviser. The information included herein reflects current views of the Adviser only, is subject to change, and is not intended to be promissory or relied upon. There can be no certainty that events will turn out as the Adviser may have opined herein.

No offer to purchase or sell securities: This document does not constitute an offer to sell (or solicitation of an offer to buy) any security and may not be relied upon in connection with the purchase or sale of any security.

No reliance, no update and use of information: You may not rely on this document as the basis upon which to make an investment decision. To the extent that you rely on this document in connection with any investment decision, you do so at your own risk. This document is being provided in summary fashion and does not purport to be complete. The information in this document is provided you as of the dates indicated and the Adviser does not intend to update information after its distribution, even in the event the information becomes materially inaccurate.

Knowledge and experience: You acknowledge that you are knowledgeable and experienced with respect to the financial, tax and business aspects of this presentation and that you will conduct your own independent financial, business, regulatory, accounting, legal and tax investigations with respect to the accuracy, completeness and suitability of this information, should you choose to use or rely on this document, at your own risk, for any purpose.

No tax, legal or accounting advice: This document is not intended to provide and should not be relied upon for (and you shall not construe it as) accounting, legal, regulatory, financial or tax advice, or investment recommendations. Any statements of U.S. federal tax consequences contained in this document were not intended and cannot be used to avoid penalties under the U.S. Internal Revenue Code or to promote, market or recommend any tax-related matters addressed herein.

Confidential information and distribution: By accepting receipt or reading any portion of this document, you agree that you will treat all information contained herein confidentially. Any reproduction or distribution of this document or any related marketing materials, as a whole or in part, or the disclosure of the contents hereof, without the prior written consent of the Adviser, is prohibited.

Suitability: Any investment program involves a high degree of risk and is suitable only for sophisticated investors who meet certain other suitability standards.

Investment strategies, market conditions and risk disclosures: Notwithstanding the general objectives and goals described in this document, readers should understand that the Adviser is not limited with respect to the types of investment strategies it may employ or the markets or instruments in which it may invest. Over time, markets change and the Adviser will seek to capitalize on attractive opportunities wherever they might be. Depending on conditions and trends in securities markets and the economy generally, the Adviser may pursue other objectives or employ other techniques it considers appropriate and in the best interest of the Fund. No representation or warranty is made as to the efficacy of any particular strategy or actual returns that may be achieved.

Projections: This document may contain certain “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of the Strategy’s investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

Disclosures

- Performance presented from inception through September 2020 is for a representative account of the Owls Nest Partners Concentrated Long Only SMA strategy (the “Strategy”). As of October 2020, performance is for a composite of separately managed accounts managed in accordance with the Strategy (the “Composite”). Performance is presented gross and net of all fees, as of the date listed at the top of this document. The fees applied are the prevailing fees of the Strategy at the time such performance was generated. From inception to the date of this document, the fee structure applied is a 1% annual management fee, and 15% performance fee that is charged only on the outperformance of the Strategy to the Benchmark (as defined below), and only after five years. Performance fees are accrued monthly. The vehicle for the Strategy is a separately managed account. All performance is calculated by the Adviser. Further information regarding the Strategy or the Composite can be provided upon request. The Adviser does not claim compliance with the GIPS reporting standards and the performance presented herein has not been audited or verified by any third-party. The Russell 2000 Total Return Index (the “Benchmark”) is a broad market index that is presented for comparative purposes as the performance benchmark to the Fund. The Benchmark is an unmanaged index consisting of the smallest 2000 stocks in the Russell 3000 Index. The stocks are issued in the United States, and the Benchmark includes the reinvestment of all dividends and income. Because the Benchmark is unmanaged, it assumes no transaction costs, management and performance fees, or other expenses. Unlike the Fund, it contains only domestic companies and is rebalanced monthly. Therefore, while the Benchmark contains publicly traded companies, it does not purport to represent an exact performance comparison to the Strategy. It is not possible to invest directly in an index, such as the Benchmark.

- The Russell 2000 Total Return Index is the performance benchmark for the Strategy (the “Benchmark”). The Benchmark is a domestic equity market index of the 2,000 smallest companies by market capitalization in the Russell 3000 Index. Because the Benchmark is unmanaged, it assumes no transaction costs, management fees or other expenses. The calculation of the benchmark return includes the reinvestment of all dividends. It is not possible to invest directly in an index, such as the Benchmark, and therefore it is presented here for information purposes only.