- Responsible for new idea generation; portfolio construction; risk management; due diligence

- 25+ years overseeing concentrated small-cap portfolios, on behalf of the most sophisticated allocators in the United States

- Previously: Founder, Endowment Capital Group; Portfolio Manager, Downtown Associates; Analyst, W.H. Newbold’s Son & Company

- University of Pennsylvania, Wharton School, B.S. 1986

- Married to Isabella, 3 sons, 3 daughters, 2 dogs

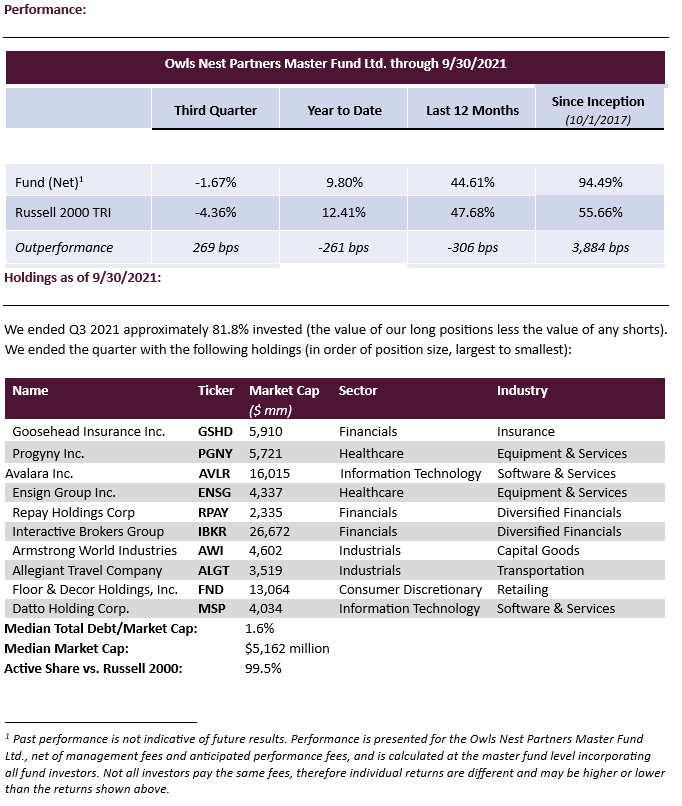

by Owls Nest Partners on Sep 30, 2021

Quarterly Attribution:

Despite its being a down quarter for stocks, the winners and losers tally was close with four gainers and six decliners. The positive contributors, in order of largest impact to smallest, were Goosehead Insurance (GSHD), Floor & Decor (FND), Avalara (AVLR), and Allegiant Travel (ALGT). The negative contributors, in order of largest impact to smallest, were Ensign Group (ENSG), Armstrong World Industries (AWI), Datto (MSP), Progyny (PGNY), Interactive Brokers (IBKR), and Repay (RPAY). In general terms, quarterly stock performance had little to do with the fundamental performance of the companies - which was solid to exceptional across the board - but was instead driven by a rebound of those stocks that had been recent laggards.

Portfolio Adjustments:

In the quarter we did not add any new positions or sell any existing ones. Datto, highlighted below, was added in Q2 although we saved the detailed discussion for this letter due to the length of the prior one. Given that it was a fairly quiet period for our companies and their stocks, we did not make many significant changes to the portfolio. We pared back on a few positions into pockets of significant strength and added to positions whose stock price experienced weakness and where we believe the outlook is much stronger than what the market is discounting. The most significant increases were in Datto and Repay while the trimming included Goosehead Insurance and Progyny.

Datto Holding Corp. (MSP):

If you ever have to choose between the best product or the best distribution, take distribution. Product leadership may come and go. Superior distribution always wins.

In 1980, when IBM was hurriedly designing its PC and making substantial use of third parties for the first time, it faced a problem when negotiations to license an operating system (OS) from the logical partner stalled. Rather than risk pushing back the all-important launch deadline, it reached out to a small company whose versions of certain programming languages, including BASIC, it was already licensing. That company, Microsoft, had never developed an operating system but went ahead and agreed to provide an OS. They, in turn, approached a local software company and licensed and ultimately bought for the not-so-princely sum of $50,000 a marginal product with the great name Q-DOS (for Quick and Dirty Operating System) that was used primarily to test hardware. Microsoft brilliantly asked that their deal with IBM not be exclusive, thereby giving Microsoft the right to sell their operating system to other companies under the new name MS-DOS. Perhaps blinded by arrogance or lack of appreciation of the revolution in computing that they were helping to create, IBM agreed. The rest is history. After negotiating license deals with IBM’s competitors, Microsoft had frictionless distribution to 90% of America’s computers and became the de facto operating system for countless millions of computers. A marginal product, after a few months of tinkering, became the foundation of a fantastically profitable monopoly touching much of the world’s economy through this masterstroke of distribution strategy. IBM, on the other hand, got caught in a commodity hardware battle which they lost to others, including Dell, who won because of an innovative and lower cost direct-to-consumer method of distribution.

The power of the right distribution strategy is a consistent theme in our portfolio. Avalara wins because of their more than 1,000 integrations and partnerships with ERP and other “invoice” creators (such as marketplaces like Shopify or website builders like Wix) who effectively provide distribution for Avalara as IBM did for Microsoft. Armstrong World Industries was once sued (ultimately unsuccessfully) on the grounds that their exclusive contracts with the largest distributors in each region of the country blocks existing and new competition and was a violation of anti-trust laws. Allegiant’s unique position as a dominant airline in its core, smaller markets enables it to distribute exclusively through its own website and app which enhances their cost advantage by avoiding third party online travel agency (e.g. Expedia) fees and gives it superior ability to capture the economics of their customers spend on hotels and rental cars through bundling with airfare, effectively getting costless revenue for being an efficient distribution channel for those hotel and rental car partners. And we have companies who recognized distribution channels that were horribly antiquated, fragmented, and unable to properly serve the end customers, and who set about completely redefining the method of distribution from the ground up. This is the case for Floor & Decor and Goosehead Insurance which is why they have so much growth still ahead of them.

The distribution channel that is relevant to Datto is the 125,000 Managed Service Providers (MSPs) that oversee on an outsourced basis the IT infrastructure, applications, security, and technical support for small and medium sized businesses (SMBs) globally. Although some consolidation is inevitable and healthy, the MSP market is enormously fragmented for logical and durable reasons as most SMBs want and need someone local, someone who they matter to so they will get attention in a crisis, and someone with knowledge of their particular industry and software applications. MSP fragmentation is critical because in this environment the power does not accrete to the middleman in the way that it does with say Amazon or even Goosehead Insurance, but instead to the supplier who successfully empowers the channel.

The MSP industry developed in the early 2000’s about 20 years after the big bang moment for SMB IT: the August 12, 1981 introduction of the IBM PC which at $1,565 cost about 98% less than the next cheapest IBM business computing platform. In the early days, the needs were straightforward, and any employee that was young and with some interest in computers could add “computer guy” to his other responsibilities. Soon things started to get much more complex, and the savvy generalist doing this in addition to a real job was overmatched. Enter “Johnny Ponytail”, the likeable but strange outsourced IT guy who took care of all things computer related on a one-off time and material basis. However, over time, the breadth of capabilities needed, the mission critical nature of IT, and the challenge small businesses have in attracting and keeping good IT talent have made it impractical for small business to attempt to manage IT in-house or on an as-needed basis. This need has ushered in the era of the managed service provider (MSP).

The MSP market is huge, controlling approximately 9% of the SMB IT spend of $1.1T currently, and it is growing rapidly. Most industry watchers predict that by 2023 MSPs will control 11% of the SMB IT spend which itself is growing by ~5% annually (implying ~16% MSP growth). In general, the dividing line between the MSP market and the “enterprise” market is companies with greater than 1,000 employees, but even that is breaking down in the favor of MSPs as increasingly large companies are hiring a MSP to supplement their internal resources in this era of scarce, available, IT talent.

Datto’s current offerings address approximately $28B of the MSPs total offering, with Datto’s products centered around the critical areas of backup and disaster recovery, and data security. Datto enjoys a reputation for very technically strong and easy to use products built with the most current cloud technology stack. But that’s just the product. Datto wins because of how they go to market and because of the trust and confidence they have earned amongst the thousands of MSP partners they sell through. In many ways, Datto sees its mission as not to sell product but rather to develop the tools needed to help their MSP partners grow and prosper. Hence, when they came public, they chose the ticker “MSP”.

A product being sold through and administered by MSPs has very different technical requirements than a product developed specifically for the enterprise market. In addition to the importance of simplicity and ease of use, the MSP product needs to be configurable so that one MSP technician can have a view across many different SMB end clients. Datto serves only one master – the MSP market – and has no enterprise products to sell directly to end users, thereby negating the need for a direct salesforce which would compete with their MSP partners. Their product is therefore designed specifically for MSP-only use cases. This approach also gives their MSP partners complete flexibility in how they want to price or bundle the suite of Datto products to deliver a customized solution to the end SMB customer. Furthermore, without an enterprise product or direct salesforce, the end customer can only access the Datto suite of products through the MSP channel. And to protect their MSP partners, Datto offers no transparency to the cost of a single Datto product, which ultimately positions Datto as a profit line-item to their MSP partners, rather than a cost item.

Datto also has market leading products that they sell to MSPs to help them run their daily operations. Datto offers a next generation RMM (Remote Monitoring and Maintenance) tool built on the cloud which is essential for managing a computer or a network from a remote location (think when your IT staff remotes into your computer to patch an issue or download security software). AutoTask, their PSA (Professional Services Automation) tool, is the equivalent of an ERP system for any MSP and is used to track work tasks and processes, client information, inventory, billable hours, technician productivity, time-off requests, and more. The ability to buy so much from one vendor is increasingly resonating in the market, not only because MSPs need to simplify their business and gain the advantage of stronger vendor relationships with “one throat to choke” which reduces vendor complexity and field tech training requirements, but also because for the first time, a vendor is able to deliver tangible benefits from tight product integration.

Datto has three vectors of growth: 1) growth within their existing MSP client base, 2) the addition of new MSP clients, and 3) the development of new products to distribute through the MSP channel. Our conversations with Datto clients and even competitors make us confident in all three vectors. The vast majority of Datto’s MSP clients only use one or two Datto products and use those products across only a portion of their SMB client base. The growing maturity of the MSP market, and the desire to simplify by standardizing on easy to administer products, and Datto’s ability to bundle and integrate products including the newly released and much anticipated backup for Microsoft Azure, will drive growth within this existing base. Today, Datto’s average MSP customer spends approximately $33,600 on Datto products annually, however there are over 1,250 top-end MSP partners who are spending over $100,000 annually with Datto. Datto typically prices “per end user employee per month” or “per end point per month” so they also inherently grow as the SMBs add employees or add endpoints. With only 17,800 of the global 125,000 MSPs, Datto has plenty of runway to keep adding MSPs consistent with their historic rate of 500 net new adds per quarter. This growth vector is particularly important because each MSP on average serves dozens of customers and hundreds of end points, so there is significant sales and support leverage from adding a new MSP partner.

New product is the most exciting vector. The company recently released SaaS protection to back up and restore SaaS applications like Microsoft Office 365 which has received significant traction, and just released Continuity for Microsoft Azure, which offers complete protection for data stored in Microsoft’s cloud as well as cost savings through reduction in the amount of data stored by Microsoft. Many SMBs have already moved to the cloud, and that trend will continue. But moving to the cloud does not obviate the need to backup and protect the data and ensure quick and easy disaster recovery. There is no shortage of opportunity for new products to roll out to this channel. If they were updating “The Graduate” for today, the one-word Mr. McGuire would share with Ben, would no doubt not be “plastics”, but “cybersecurity” instead. And Ben would be smart to heed the advice, given how many MSP's SMB customers are on the journey of moving from spending $1 per user per month solely on basic anti-virus to $10 or even $100 over time per user per month on a suite of cyber security products, given growing awareness and fear around ransomware attacks, other existential threats and the compounding impact of expanding end points per user.

Despite its leading industry position, significant profitability (20% EBIT in 2021 and the ability to top 30% over time) and great growth prospects, Datto is something of an odd duck by Wall Street conventions. It came public as a play on an industry that nobody followed or cared about due to it having no other related public companies, and it had no direct comparables. It is a small cap to begin with and, as we discussed last quarter, is 70% owned by Vista Equity, its private equity sponsor, so it trades little volume. For now, at least, it is the last thing any largescale investment shop wants to work on – something that requires a lot of time and work to understand both the industry and the company and that you can’t build a meaningful position in anyway. The perfect example of a name where Owls Nest can have an edge.

Many software companies, especially enterprise software companies or those tied to ecommerce, benefitted from COVID as the world scrambled to work remotely. This was not the case for Datto as SMBs fearfully tightened spending and MSP partners were focused on helping SMBs shift to work from home and secure many more and geographically scattered IT assets rather than adding new SMBs and cross-selling Datto products to existing SMBs. Some of Datto’s MSPs folded, and the company shrank or eliminated some relationships as they tightened credit standards. Datto’s resilient business model and multiple vectors of growth allowed it to grow annual recurring revenue 14% in 2020 and somewhat faster in 2021, but that was a meaningful deceleration at a time when many software companies were enjoying almost panic buying. The company had the new costs of being a public company, and Datto made clear that 2021 would be a year of heavy investment spending as important new products were released.

Driven by the factors in the two above paragraphs, Datto’s stock has dropped from the low 30’s to the low 20’s despite its recent growth on the high end of our expectations, the reacceleration in the additions of new MSP partners, and the very strong reviews of the recently released products which serve to reinforce the value of an MSP consolidating their vendor relationships and replacing older former best of breed backup and security products with Datto’s. This stock decline is even more surprising to us because the recent high profile debilitating cases of ransomware including Colonial Pipeline will only accelerate the inevitable adoption of security products like Datto’s in the heretofore slow-moving SMB market. The catalyst may not be a sudden change of heart among SMBs about their willingness to take data security risks, but the fact that they may soon find it impossible to get essential insurance or to do business with key partners unwilling to work with companies that have inadequate data protection. We feel that by being patient, we have an Owls Nest entry point on a quirky Owls Nest name. And as we like it, while every investment has its risks, our success with this investment does not have the extra hurdle of our having to nail a macro call on the economic cycle, congressional actions, interest rates or commodity prices. Those factors will be overwhelmed by the growth of data, the importance of data, and the ever-increasing need to make sure that that data is secure. And with such a strong position in its key distribution channel, Datto is in a great position to fully exploit the huge and still underpenetrated opportunity that lies in making all SMB data secure.

What Does It Mean to Put the Client First?:

What does it mean to “Put the Client First?” Evidentially to us, it appears that rather than really address that question, most investment firms rely on a menagerie of perks and an army of polished client service reps, christened “Portfolio Managers”, to relay platitudes and generally comfortable, conventional thinking in as personal a way as possible while still maintaining juicy margins and profitability for the firm irrespective of performance. Harsh, but the evidence is what the evidence is, and we call ‘em like we see ‘em (at least in letters like this that only a handful see). Instead, we believe truly putting the client first requires enough tough decisions, risk bearing, and short-term sacrifice that one only does it if they are truly passionate about their work and their sense of purpose.

What do we mean by tough decisions, risk bearing and short-term sacrifice? Let’s first look at the issue of scale in the world of active, fundamental equity management. Beyond each strategy’s reasonable capacity, the tradeoff is clear – growth benefits the manager at the expense of his/her ability to perform for the client. I have always been blown away by stories of managers who did well by early clients and then grew, often with abundant help and support from those clients to the point where the client had no choice but to terminate the manager as performance suffered and culture changed. How could anyone say, “thanks for helping me out when I needed it, but I don’t need you anymore, the money is flowing, and I think my odds are pretty good with or without you, so I’m intentionally making decisions that can only harm you”?

Shouldn’t putting the client first require a fee structure that is fair to all parties and tethered to performance and commitment to the client’s long-term success? Who does using carried interest in an LP structure benefit? Only the GP/manager. It generally hurts the client since its annual calculation means that the client’s full dollar does not compound and because clawing back performance fees is very difficult even after subsequent underperformance. Why have incentives based annually at all if the strategy claims to be long-term in nature? Why should the client bear all the risk of subsequent underperformance? This is why our incentive is only earned after five years and only earned if we outperform over the full period, not just some short subset. And we understand further that doing what we believe is the right thing is additionally unpalatable to other managers because it results, God forbid, in their paying a lot more taxes.

We believe that honoring any claim to be able to outperform for their clients requires a manager to take certain risks and alter its business model in ways that inherently reduce the certainty of its profitability. In our case, concentration exposes us to periods of short-term underperformance which hurts us by making us unable to work for the many potential clients who are short-term in nature and care about tracking error. Just as having limited capacity makes it impossible for us to work for very large potential clients. But without concentration, it is impossible to have an experienced portfolio manager with intimate knowledge of every investment you own, and without capacity constraint it is impossible to invest in smaller growth companies and maintain advantageous liquidity. And relying on in-depth primary research instead of computer algorithms inherently limits profitability due to the manual (but fascinating) process involved. But that is in our opinion the only way to truly have conviction, a complete understanding of the company, and the ability to see a couple moves ahead on the investment chess board.

For the most part, we do what we do because we love doing it. Investing, as we do it, is endlessly interesting and rewarding in many ways. But we also we do it because we hope in a modest way to change our industry.

According to Jack Bogle2 the period of huge scale in the investment industry began in earnest after a 1950’s California court case allowed investment managers there to sell their businesses at a premium to book value for the first time. It is impractical to think that an industry this large could be a cottage industry of small practitioners or that that would even be desirable. The industry’s advancements are, on the whole, positive. But it seems to us that the first duty being that of putting the client’s interest first has gotten lost in the shuffle. We hope we do our part to restore that focus and demonstrate that putting the client first leads not only to superior investment results but ultimately is the best way to build a truly outstanding and durable investment firm. And in the interim, there is comfort in this irony: The fact that others have demonstrated no interest in copying our structure only reinforces the depth and durability of our advantages in the markets.

Owls Nest Partners Firm Update – New Hires:

We believe that in evaluating talent, commitment to our culture is just as important as competence. We can always train and develop people, but we cannot succeed with anyone who will not thrive in our culture, or truly believe in what we consider to be our noble purpose. As such, we always want to hire talent ahead of the need so we can have the luxury of taking our time to make sure we have competence and cultural fit. Accordingly, although our business is still fairly simple and Michelle Krayer has our operations running smoothly, we are very happy to have been able to add two professionals to the operations team since our last firm update.

In May, Angelo Rodriguez joined the team having built significant experience in trade operations at both J.P. Morgan and BlackRock. He is adding heft to our daily trade operations procedures, including communication with our outsourced trading teams, transaction cost analyses, commission reporting, and daily allocations across our growing account base. And to ensure continued high levels of service for that growing client base, we welcomed Matt Munro to the team in June as our new Director of Client Services. Matt joins us from MetLife Investment (formerly Logan Circle Partners), where he built a career servicing many of the firm’s hundreds of clients. Increasing our confidence in his ability and his commitment to our culture is the fact that Matt is a known quantity to us, having been hired 8 years ago and subsequently trained at Logan Circle, by David.

March 31, 2022 Closing:

I have found over the years that institutional allocators are generally a polite and pleasant group who keep their misgivings about managers to themselves. There is one exception, however. I have found that almost every allocator cynically shares lots of stories about managers who promised to be capacity constrained and then reneged on that pledge as soon as it became inconvenient. So, we will take this time to remind you what we said in our Year-End 2020 letter: We have a wonderful, fun, and rewarding business, and we intend to keep it that way. Discipline around capacity and growth is the goose that repeatedly lays the golden egg. With our appreciation of this fact, we will close to new capital once our assets under management reach $250M.

We ended the quarter within striking distance of $250M AUM, and we expect a few commitments to fund in the next few months. And we are indeed going to do as we said we would and close, effective March 31, 2022, for a period of six months. During that time, we will not take on new clients, however we will allow existing clients to make incremental contributions. To be clear, this is not imposed due to any concern on our ability to invest more than $250M. Instead, we view this as a reasonable point in our growth to pause and make sure that

2 Mr. Bogle referenced this in a speech I heard him give at the University of Delaware approximately seven years ago. Unfortunately, I cannot put my finger on the exact lawsuit, but I am confident we can trust Jack Bogle on a discussion of scale and history in the investment business.

everyone internal and external to the business, especially clients, is happy with all aspects of their relationship with Owls Nest Partners and that all operational policies, procedures, vendors etc. are prepared for the next leg of growth. Just as we take a long-term view toward investing, we want to take a long-term view toward how we run our own business.

Investment Program:

For the benefit of any first-time readers, the hallmark of the Owls Nest Partners approach is the purchase of industry leading growth companies when a temporary headwind has recoiled the fundamental growth drivers and compressed its multiple. This typically happens as hot money “renters” exit and drive the price down. There is no such thing as a free lunch: we can only receive our requisite value if we accept that our companies will appear “catalyst-less” and uninteresting for some time. We believe we are wildly overcompensated for this modest level of patience, especially since it is in these moments that a company can invest in its own business with the highest returns. There is wonderful optionality associated with a well-run, shareholder friendly, cashladen company that is able to aggressively put money to work during a temporary headwind.

It is our belief (and experience) that our future outperformance will not be driven by any economic or market forecasting prowess but instead by ten unique investments, each playing out over time. We perceive these investments to have modest downside due to high quality and low expectations, and very significant upside as growth and margin expansion return in spades. We seek reasonable ballast and diversification within the portfolio as a result of our natural conservatism (strengthened by our co-investment alongside clients) and our predisposition to avoid crowded trades and instead invest in temporarily out of favor areas.

Final Thoughts:

We hope you and your family remain safe and well.

More than ever, we thank you for your support and for choosing to have your money working alongside ours.

Gratefully,

Philip & the Owls Nest Partners team

Disclaimer

In General: This disclaimer applies to this document and the verbal or written comments of any person presenting it. This document has been prepared by Owls Nest Partners IA, LLC as Investment Adviser (the “Adviser”) of Owls Nest Partners Concentrated Long Only SMA (the “Strategy”). By receiving this document you acknowledge that you are an investor in the Strategy, or a prospective investor who is known to the Adviser, and that you meet all regulatory definitions of “Accredited Investor” and “Qualified Client,” in order to be considered a prospective client of the Adviser. The information included herein reflects current views of the Adviser only, is subject to change, and is not intended to be promissory or relied upon. There can be no certainty that events will turn out as the Adviser may have opined herein.

No offer to purchase or sell securities: This document does not constitute an offer to sell (or solicitation of an offer to buy) any security and may not be relied upon in connection with the purchase or sale of any security.

No reliance, no update and use of information: You may not rely on this document as the basis upon which to make an investment decision. To the extent that you rely on this document in connection with any investment decision, you do so at your own risk. This document is being provided in summary fashion and does not purport to be complete. The information in this document is provided you as of the dates indicated and the Adviser does not intend to update information after its distribution, even in the event the information becomes materially inaccurate.

Knowledge and experience: You acknowledge that you are knowledgeable and experienced with respect to the financial, tax and business aspects of this presentation and that you will conduct your own independent financial, business, regulatory, accounting, legal and tax investigations with respect to the accuracy, completeness and suitability of this information, should you choose to use or rely on this document, at your own risk, for any purpose.

No tax, legal or accounting advice: This document is not intended to provide and should not be relied upon for (and you shall not construe it as) accounting, legal, regulatory, financial or tax advice, or investment recommendations. Any statements of U.S. federal tax consequences contained in this document were not intended and cannot be used to avoid penalties under the U.S. Internal Revenue Code or to promote, market or recommend any tax-related matters addressed herein.

Confidential information and distribution: By accepting receipt or reading any portion of this document, you agree that you will treat all information contained herein confidentially. Any reproduction or distribution of this document or any related marketing materials, as a whole or in part, or the disclosure of the contents hereof, without the prior written consent of the Adviser, is prohibited.

Suitability: Any investment program involves a high degree of risk and is suitable only for sophisticated investors who meet certain other suitability standards.

Investment strategies, market conditions and risk disclosures: Notwithstanding the general objectives and goals described in this document, readers should understand that the Adviser is not limited with respect to the types of investment strategies it may employ or the markets or instruments in which it may invest. Over time, markets change and the Adviser will seek to capitalize on attractive opportunities wherever they might be. Depending on conditions and trends in securities markets and the economy generally, the Adviser may pursue other objectives or employ other techniques it considers appropriate and in the best interest of the Fund. No representation or warranty is made as to the efficacy of any particular strategy or actual returns that may be achieved.

Investors must be prepared to bear the risk of a total loss of their investment.

Projections: This document may contain certain “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of the Strategy’s investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

Disclosures

- Past performance is not indicative of future results. Performance presented from inception through September 2020 is for a representative account of the Owls Nest Partners Concentrated Long Only strategy (the “Strategy”). As of October 2020, performance is for a composite of separately managed accounts managed in accordance with the Strategy (the “Composite”). Performance is presented gross and net of all fees, as of the date listed at the top of this document. The fees applied are the prevailing fees of the Strategy at the time such performance was generated. From inception to the date of this document, the fee structure applied is a 1% annual management fee, and 15% performance fee that is charged only on the outperformance of the Strategy to the Benchmark (as defined below), and only after five years. Performance fees are accrued monthly. All performance is calculated by the Adviser and represents preliminary, unaudited figures that are subject to change. Further information regarding the Strategy or the Composite can be provided upon request. The Adviser does not claim compliance with the GIPS reporting standards and the performance presented herein has not been audited or verified by any third-party.

- The Russell 2000 Total Return Index (the “Benchmark”) is a broad market index that is presented for comparative purposes as the performance benchmark to the Fund. The Benchmark is an unmanaged index consisting of the smallest 2000 stocks in the Russell 3000 Index. The stocks are issued in the United States, and the Benchmark includes the reinvestment of all dividends and income. Because the Benchmark is unmanaged, it assumes no transaction costs, management and performance fees, or other expenses. Unlike the Fund, it contains only domestic companies and is rebalanced monthly. Therefore, while the Benchmark contains publicly traded companies, it does not purport to represent an exact performance comparison to the Strategy. It is not possible to invest directly in an index, such as the Benchmark

- The Standard & Poor’s 500 Index is a domestic equity market index that is presented for comparative purposes only (the “S&P 500”). The S&P 500 is an unmanaged index consisting of largest 500 companies by market capitalization having common stock listed on the NYSE or NASDAQ. The S&P 500 index components and their weightings are determined by S&P Dow Jones Indices. Because the S&P 500 is unmanaged, it assumes no transaction costs, management and performance fees, or other expenses. It is not possible to invest directly in an index, such as the S&P 500. In instances where insufficient data is available for the Benchmark, the S&P 500 has been used as a proxy for the broader domestic equity market.