- Responsible for new idea generation; portfolio construction; risk management; due diligence

- 25+ years overseeing concentrated small-cap portfolios, on behalf of the most sophisticated allocators in the United States

- Previously: Founder, Endowment Capital Group; Portfolio Manager, Downtown Associates; Analyst, W.H. Newbold’s Son & Company

- University of Pennsylvania, Wharton School, B.S. 1986

- Married to Isabella, 3 sons, 3 daughters, 2 dogs

by Owls Nest Partners on Dec 31, 2019

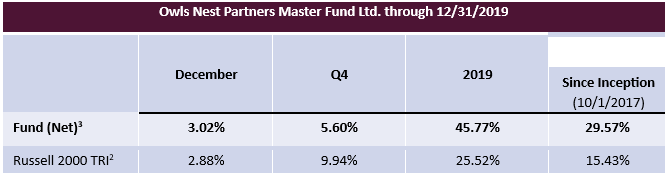

Performance:

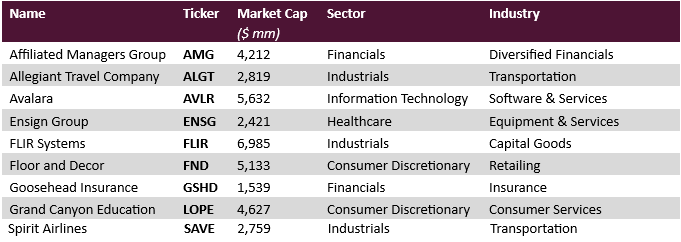

Holdings as of 12/31/2019:

We ended 2019 effectively 97% invested in nine companies. The current holdings are as follow (in alphabetical order):

Median Total Debt/Market Cap: 10.7% Median

Median Market Cap: $4,212 million

1Past performance is not indicative of future results. All returns are presented gross of fees and are preliminary, unaudited, figures that are subject to change. Actual client returns may be different from returns presented herein.

Q4 Attribution:

During the quarter, five of the nine companies we owned were positive contributors, while four detracted from performance. In order of largest impact to smallest, our gainers were Ensign Group (ENSG), Allegiant Travel (ALGT), Avalara (AVLR), Affiliated Managers Group (AMG) and Spirit Airlines (SAVE). The decliners, also in order of largest impact to least, were Goosehead Insurance (GSHD), Grand Canyon Education (LOPE), Floor & Decor (FND) and FLIR Systems (FLIR). While it was a volatile quarter for some of the stocks, it was a boring, businessas-usual quarter fundamentally for the portfolio companies as a whole.

Q4 Portfolio Adjustments:

We’d love to tell you about all of our brilliant moves, but we didn’t make any significant changes to the portfolio in the quarter. Given how much we like what we own, that may, in time, turn out to be brilliant. We’ll see. Also, there wasn’t a lot of volatility in the quarter to provide unique entries or exits. We worked on many possible new ideas, but improvement upon the current portfolio is a high bar to clear.

In lieu of comments on a new position, we’re offering commentary below on “Staying Rich”.

2019 Attribution:

Avalara, Floor & Decor, Allegiant Travel, and Ensign Group (in that order) led the way for us this year, with each contributing more than 600 bps to our performance. Also contributing were Goosehead Insurance (bought in Q2), Ross Stores (sold in Q3), FLIR Systems, Fastenal (sold in Q3), Spirit Airlines (bought in Q3) and Healthcare Services Group (sold in Q1). Grand Canyon Education was our biggest loser for the year, costing us about 100 bps, and Affiliated Managers Group was a modest negative performer.

Commentary on Tax Efficiency:

Performance numbers are important, but what matters most is what you have left after paying taxes. We pay taxes, and while we don’t let tax factors drive investment decisions, we manage for after-tax returns. Every partner’s tax results will vary slightly depending on when he or she entered the Fund, however, everyone should benefit from tax efficiency. This year, for every dollar of appreciation, ~$0.89 came in the form of unrealized and, hence untaxed, gains. Short-term gains (the most expensive variety) were actually negative ~$0.04 which you can use to offset expensive gains elsewhere, and long-term gains were only ~$0.15. Of course, every year will be different, but know that we are focused on this important element of your real returns.

Commentary on "Staying Rich":

When I joined the Loomis family office as a young equity analyst, the mandate was clearly and effectively communicated. It went like this: “We are already rich. Your job is specifically not to take chances where there is a real risk of permanent capital loss in some attempt to get rich. The focus here is absolute returns. Short-term underperformance is fine and is, in fact, a logical and even necessary byproduct. Permanent loss of capital is unacceptable. But we’d also like to get richer, maybe even a lot richer, which, by the way, is a lot easier to do if you still have close to 100 cents on the dollar to invest after a market downdraft. So while doing nothing is acceptable, and vastly superior to chasing hot or low quality stuff, what you should do is scour the world of public equities, take advantage of our longer-term investment horizon and find misunderstood situations where we can have an edge and a wildly positive and asymmetric return profile. And, by the way, we pay taxes.”

That was 1992, and I cautiously felt my way around with fine but generally unremarkable results, trying to learn as much as I could. Some things followed logically. The best opportunities would be in small-cap land, so I would focus there. Small-cap focus also helped me overcome what I saw as my great weakness. Owning secular growers with lots of share to gain before reaching bloated maturity would neutralize my inability to forecast macro or market movements. I’ve subsequently learned that that weakness is scarcely mine uniquely, although my recognition thereof and willingness to adapt accordingly might be. I saw no sense diversifying AWAY from the great opportunities I had found and knew well, so I would concentrate in ten or so ideas. I would invest in longterm growers to make best use of all that fundamental research and minimize taxes. I would stick with leading companies with resilient business models and avoid leveraged balance sheets, since debt is great until it isn’t, at which point it can make rich people poor.

Three years later an episode crystalized the discipline and process that defines our opportunity set 25 years later. I was working on IMRS, a software company that sold budgeting and financial consolidation software to large enterprises where the CFO was the ultimate decision maker. It was the easiest due diligence ever, since, as a young analyst, I spent all day talking to CFOs. People loved the current version of the product, but the soonto-be-released Windows version was a complete game changer. Market share would explode at the expense of the complacent private and smaller competitors who had yet to develop a Windows-based version, in part because of IMRS’s brilliant move to get early and exclusive access to the Windows code for this application. Greater functionality and flexibility would also mean higher price points and the ability to cross sell other modules.

But my mandate required me to keep my powder dry. Expectations were reasonably lofty, and it was fairly priced. As such, it didn’t possess the wildly positively asymmetric return profile. And then a funny thing happened. All the CFOs, who had unhesitatingly stated they would buy the product, suddenly started backpedaling. As a rule, they loved the product more than ever, but they had all learned that they didn’t have the IT infrastructure in place to handle the system requirements. It would take a few quarters before corporate IT could sign off. So, they’d stick it out with manual, error-prone, spreadsheet-based processes for 180 more days. Not ideal, but no big deal.

Then IMRS reported a weak June quarter, and the stock got beaten up. This got interesting. But they assured everyone that this was temporary and the pipeline was exploding. The stock recovered somewhat. A September quarter negative preannouncement was more than the market could bear. The stock collapsed and was now down 80% from its highs earlier in the year, and I knew the pipeline was indeed exploding and the turmoil in the marketplace which led to the shortfall and the crushing of the stock was actually the best thing possible for the business because it signaled the switch to Windows, where they would be dominant, was happening.

The patience that the mandate required and the liberating ability to do nothing until the stars were aligned were how we could make sure we not only stayed rich but got a lot richer. And we did exactly that, as a result of our ownership of IMRS before it ended up inside Oracle.

The patience that the mandate required and the liberating ability to do nothing until the stars were aligned were how we could make sure we not only stayed rich but got a lot richer. And we did exactly that, as a result of our ownership of IMRS before it ended up inside Oracle.

I was stupefied that all this happened. After all, anyone who bothered to talk to any customers knew what was happening. And the CEO, who owned a slug of stock, was a guy you’d want to bet on all day long, the balance sheet was bulletproof and cash-laden, and the company was solidly profitable despite the headwind. So what if the numbers went down for a few quarters? That’s when I learned that if you are armed with an organically developed fundamental competitive mosaic about a smaller public company and can take a longer-term view, buying from “renters” who are short-term oriented (because they took money from short-term people), broadly diversified (because they fear tracking error), and who are making decisions generally on readily available numbers as opposed to hard-to-get qualitative views from customers, competitors, suppliers, etc. was a very profitable formula. And who knew that 25 years later those scaled, diversified, short-term oriented, quantfocused managers would grow and proliferate to such an extent further expanding our competitive advantage.

That event explains the benefit of patience, a longer-term view and investing with an absolute return mindset as applied to individual investments, but what about as a PM building out a portfolio?

A couple years later, I was cutting my teeth as a new PM. I didn’t appreciate it at the time, but I was about to go through the best possible PM training. The dot.com/NASDAQ bubble/burst of 1999-2001 presented incredible pressures on a PM. In 1999 and early 2000, the markets were climbing parabolically, and the need to keep up just led to more distortions. New valuation metrics were being created daily, and naivete trumped skepticism and diligence. And then all the smartest guys in the room, including revered Fed Chair Alan Greenspan, bought into the new paradigm. If ever there was a time when it was difficult to stay true to being an absolute return investor with the restrictions and disciplines mentioned above, this was it. The Global Financial Crisis a decade later, and even the October 19, 1987 Crash (THAT was a crazy week!), presented interesting and different challenges, but this period was definitely more formative and perhaps more relevant to today’s markets.

I was lucky that I was armed with a powerful two-pronged antidote to the speculation contagion poisoning so many others. First, I had the mandate to think like an absolute return investor and not worry about relative performance or variations in weightings relative to an index. In fact, the irony was that the neglected sectors, which provided the cash for the purchase of dot.coms, presented great value for those willing to invest in something with no excitement or near-term catalyst. Remember that the “market” is not some monolithic thing. It is, at least to someone who focuses on the quality of businesses and the associated specific investment opportunities rather than market machinations, the artificial statistical compilation of thousands of individual markets, some of which may be very depressed while others are frothy and dangerous. Second, the addition of some endowments as clients only strengthened my conviction and ability to think longer term.

When the dust settled at the end of 2001, it was clear that the largest contributor to our very substantial outperformance and great absolute returns was simply our ability to remain objective and opportunistic, which was only possible because of our unique client roster of true long-term investors.

So, that is the key to staying rich and getting still richer – the ability to be patient, to invest with an absolute return mindset and to take a longer-term view. And not watching Cramer on CNBC.

Outlook for 2020:

We have no insight into how to play any of the commonly talked about themes in such letters as these, except generally to take the other side of the conventional and accepted opinion and to be prepared for the year to be defined by something that no one saw coming. So how do you prepare in a world of such uncertainty? Buy leading companies with the balance sheet strength, the experienced and aligned management, and the margins to play offense when others must play defense. That formula wins in good times or bad. Especially bad. Nonetheless, we are willing to step out on the ledge and make some predictions for 2020.

We believe that in 2020 leisure travelers will want to save on air travel and prefer non-stop flights. We believe people will insure their homes and will respond favorably to the savings and service only possible from an independent agent with state-of-the-art systems, national scale and who represents over 90 hungry insurers. We believe that the American housing stock will once again be the oldest it has ever been (median over 40 years old) and that millennials forming households will not want to live in a 1970s ranch without a few easy, inexpensive, high-impact upgrades like flooring and will want to save money when doing so. We believe that those with their lives at risk like the military and firefighters will want to use tools whose capabilities are enhanced by infrared sensors and vision, and that everyone concludes that before they go near anything resembling autonomous driving the systems powering those algorithms had better include night vision powered by infrared. We believe that a vast swath of America’s 20 million college students will increasingly want to attend university at a school with good outcomes, programs that lead to jobs, a low price point meaning little or no debt, especially if it’s in a town with 300+ days of sunshine a year. We believe that America’s more than 12,000 tax jurisdictions will still expect companies to collect and remit sales tax and that companies under that crushing burden and facing enormous penalties for non-compliance in something so non-core will seek to hire the clear leader to help them automate that process now that the Supreme Court has essentially ruled that states can collect sales tax on whomever they please. We believe skilled nursing facilities will take care of people being discharged from hospitals and that hospitals, faced with lower reimbursement if readmissions spike, will increase demands on their partner nursing facilities, driving growth for those operators with the best outcomes and systems for sharing data while forcing the subscale, weak players to exit the market.

Investment Program:

For the benefit of any first-time readers, the hallmark of the Owls Nest Partners approach is the purchase of industry leading growth companies when a temporary headwind has recoiled the fundamental growth drivers and compressed its multiple. This typically happens as hot money “renters” exit and drive the price down. There is no such thing as a free lunch: we can only receive our requisite value if we accept that our companies will appear “catalyst-less” and uninteresting for some time. We believe we are wildly overcompensated for this modest level of patience, especially since it is in these moments that a company can invest in its own business with the highest returns. There is wonderful optionality associated with a well-run, shareholder friendly, cashladen company that is able to aggressively put money to work during a temporary headwind.

It is our belief (and experience) that our future outperformance will not be driven by any economic or market forecasting prowess but instead by ten unique investments, each playing out over time. We perceive these investments to have modest downside due to high quality and low expectations, and very significant upside as growth and margin expansion return in spades. We seek reasonable ballast and diversification within the portfolio as a result of our natural conservatism (strengthened by our co-investment alongside clients) and our predisposition to avoid crowded trades and instead invest in temporarily out of favor areas.

Closing Thoughts:

As we wrote above, without the right clients you are doomed to mediocrity.

Thank you for the support and the decision to have your money working alongside ours.

Gratefully,

Philip & the Owls Nest Partners team

Disclaimer

In General: This disclaimer applies to this document and the verbal or written comments of any person presenting it. This document has been prepared by Owls Nest Partners IA, LLC as Investment Adviser (the “Adviser”) of Owls Nest Partners Concentrated Long Only SMA (the “Strategy”). By receiving this document you acknowledge that you are an investor in the Strategy, or a prospective investor who is known to the Adviser, and that you meet all regulatory definitions of “Accredited Investor” and “Qualified Client,” in order to be considered a prospective client of the Adviser. The information included herein reflects current views of the Adviser only, is subject to change, and is not intended to be promissory or relied upon. There can be no certainty that events will turn out as the Adviser may have opined herein.

No offer to purchase or sell securities: This document does not constitute an offer to sell (or solicitation of an offer to buy) any security and may not be relied upon in connection with the purchase or sale of any security.

No reliance, no update and use of information: You may not rely on this document as the basis upon which to make an investment decision. To the extent that you rely on this document in connection with any investment decision, you do so at your own risk. This document is being provided in summary fashion and does not purport to be complete. The information in this document is provided you as of the dates indicated and the Adviser does not intend to update information after its distribution, even in the event the information becomes materially inaccurate.

Knowledge and experience: You acknowledge that you are knowledgeable and experienced with respect to the financial, tax and business aspects of this presentation and that you will conduct your own independent financial, business, regulatory, accounting, legal and tax investigations with respect to the accuracy, completeness and suitability of this information, should you choose to use or rely on this document, at your own risk, for any purpose.

No tax, legal or accounting advice: This document is not intended to provide and should not be relied upon for (and you shall not construe it as) accounting, legal, regulatory, financial or tax advice, or investment recommendations. Any statements of U.S. federal tax consequences contained in this document were not intended and cannot be used to avoid penalties under the U.S. Internal Revenue Code or to promote, market or recommend any tax-related matters addressed herein.

Confidential information and distribution: By accepting receipt or reading any portion of this document, you agree that you will treat all information contained herein confidentially. Any reproduction or distribution of this document or any related marketing materials, as a whole or in part, or the disclosure of the contents hereof, without the prior written consent of the Adviser, is prohibited.

Suitability: Any investment program involves a high degree of risk and is suitable only for sophisticated investors who meet certain other suitability standards.

Investment strategies, market conditions and risk disclosures: Notwithstanding the general objectives and goals described in this document, readers should understand that the Adviser is not limited with respect to the types of investment strategies it may employ or the markets or instruments in which it may invest. Over time, markets change and the Adviser will seek to capitalize on attractive opportunities wherever they might be. Depending on conditions and trends in securities markets and the economy generally, the Adviser may pursue other objectives or employ other techniques it considers appropriate and in the best interest of the Fund. No representation or warranty is made as to the efficacy of any particular strategy or actual returns that may be achieved.

Projections: This document may contain certain “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of the Strategy’s investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

Disclosures

- All “portfolio” information presented is for the Owls Nest Partners Concentrated Long Only SMA (the “Strategy”). Such data represents preliminary, unaudited, figures that are subject to change. The Adviser prepares final month-end and quarterly performance figures for the Strategy, which therefore represent its own internal, unaudited estimates of performance. Because the Strategy is only offered via separate account or SMA/UMA platforms, fees will be different for each client of the Strategy. Therefore, all performance returns are presented gross of all fees and expenses. For further information regarding Strategy performance, please contact the Adviser at info@owlsnestpartners.com, or by calling 484-352-1110.

- The Russell 2000 Total Return Index (the “Benchmark”) is a broad market index that is presented for comparative purposes as the performance benchmark to the Fund. The Benchmark is an unmanaged index consisting of the smallest 2000 stocks in the Russell 3000 Index. The stocks are issued in the United States, and the Benchmark includes the reinvestment of all dividends and income. Because the Benchmark is unmanaged, it assumes no transaction costs, management and performance fees, or other expenses. Unlike the Fund, it contains only domestic companies and is rebalanced monthly. Therefore, while the Benchmark contains publicly traded companies, it does not purport to represent an exact performance comparison to the Strategy. It is not possible to invest directly in an index, such as the Benchmark

- The Standard & Poor’s 500 Index is a domestic equity market index that is presented for comparative purposes only (the “S&P 500”). The S&P 500 is an unmanaged index consisting of largest 500 companies by market capitalization having common stock listed on the NYSE or NASDAQ. The S&P 500 index components and their weightings are determined by S&P Dow Jones Indices. Because the S&P 500 is unmanaged, it assumes no transaction costs, management and performance fees, or other expenses. It is not possible to invest directly in an index, such as the S&P 500. In instances where insufficient data is available for the Benchmark, the S&P 500 has been used as a proxy for the broader domestic equity market.