- Responsible for new idea generation; portfolio construction; risk management; due diligence

- 25+ years overseeing concentrated small-cap portfolios, on behalf of the most sophisticated allocators in the United States

- Previously: Founder, Endowment Capital Group; Portfolio Manager, Downtown Associates; Analyst, W.H. Newbold’s Son & Company

- University of Pennsylvania, Wharton School, B.S. 1986

- Married to Isabella, 3 sons, 3 daughters, 2 dogs

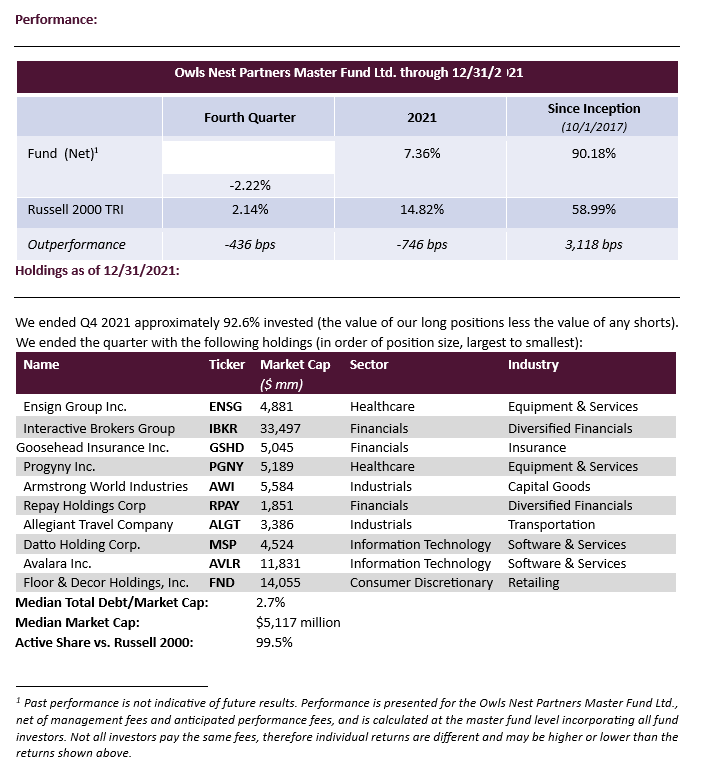

by Owls Nest Partners on Dec 31, 2021

Quarterly Attribution:

Gainers and decliners were evenly matched at five apiece. Fundamental performance of our portfolio companies was solid to exceptional across the board. The positive contributors, in order of largest impact to smallest, were Interactive Brokers (IBKR), Armstrong World Industries (AWI), Ensign Group (ENSG), Datto (MSP) and Floor & Decor (FND). The negative contributors, in order of largest impact to smallest, were Avalara (AVLR), Repay (RPAY), Goosehead Insurance (GSHD), Progyny (PGNY) and Allegiant Travel (ALGT).

Portfolio Adjustments:

In the quarter we did not add any new positions or sell any existing ones. We pared back on a few positions into pockets of strength and added to positions whose stock price experienced weakness and where we believe the outlook is much stronger than what the market is discounting. The most significant increases were in Repay and Ensign Group, while the trimming included Floor & Decor and Armstrong World Industries.

2021 Attribution:

Nine of the eleven positions we held during the year posted positive returns. Performance was broadly distributed, but, in general terms those considered reopening plays, or which had lagged in 2020 were the best performers. Armstrong World Industries was our leading contributor, followed by Progyny, Interactive Brokers and Ensign Group. Repay and Avalara were our two negative contributors for the year.

Revisiting our 2021 Outlook:

In reviewing our “predictions” for 2021, essentially everything we anticipated came to be, however not to the full extent we would have hoped. Progyny managed to grow revenues 45% and adjusted EBITDA more than 100%, but the inability to do in-person sales meetings and the impact on utilization as clients deferred family building so that they could travel and visit their families first as COVID restrictions abated, and then due to Delta and Omicron variants later in the year, definitely tamped down what was possible.

Allegiant significantly outperformed its peers and was once again one of the most profitable U.S. airlines in 2021. We made money on Allegiant in 2021, but it was something of a “what might have been” scenario as Omicronrelated labor shortages wreaked havoc on Allegiant and the rest of the industry in Q4.

Ensign had another year of incredible performance against a very challenging industry backdrop. I don’t think I’ve ever seen a company so dramatically fundamentally outperform their peers as Ensign did in 2021. Ensign clearly won our 2021 MVM (Most Valuable Management) Award, and that performance helped us make money on our investment too. However, the hoped-for flood of acquisitions of smaller, struggling players did not materialize beyond the normal acquisition cadence as federal relief dollars bought time for the weaker players and put off the inevitable.

Avalara maintained its growth rate close to 30% as hoped. Buoyed by the widening gulf between themselves and competitors and the opportunity to broaden their compliance platform beyond indirect tax, management decided to accelerate some new product investments and partnership investments – a move that we support – which reduced their near-term profitability outlook causing some indigestion later in the year, despite furthering the many-years-long runway of 20%+ revenue growth that lay ahead.

Goosehead also had a bang-up year growing policies in force by 42%. This growth drove good performance in the stock, but the advance was constrained by an obviously unpredictable major uptick in bad weather events in 2021. We love Goosehead’s agency model which requires almost no capital and is insulated from the vagaries of the underlying risk compared to the carriers who write the insurance policy and own that risk. However, in any given year Goosehead earns bonus “contingency” commission dollars based on the profitability of their underlying book of business. These commissions should grow in line with premium over time or perhaps a little faster as Goosehead becomes a larger partner for more and more carriers. 2021 turned out to be the occasional year in which everything from people texting while driving, to forest fires, to three-letter-named hurricanes (Ida and Uri) caused much greater than expected losses across the industry and hence greatly reduced contingency commissions.

2022 Outlook:

While we view short-term predictions generally as a fool’s errand, we can unequivocally express our confidence in the near-term outlook of our portfolio companies as we look to 2022. The easiest wins should come from those companies who had to navigate adversity in 2021. Ensign enters the year as our largest holding. The end of the industry’s pandemic related federal support (which Ensign generally returned), and the unprecedented scale of wage inflation in the nursing industry, are together causing panic in the skilled nursing industry. At the same time, well run and financially stable skilled nursing facilities (SNFs) are benefitting from their demonstration of essential utility during the pandemic. The continuum of care needs SNFs to handle those patients who do not have to be treated in a scarce and expensive hospital setting but who are too sick to be effectively treated at home. Ensign has earned the trust of discharging hospitals and managed care providers in all of its regions and can leverage those relationships in expanded ways in 2022. In addition to organic share growth, 2022 should be a banner year for the proven inorganic growth strategy of buying struggling small operators and upgrading management, systems and patient outcomes to dramatically improve results in future years.

Human resource directors have repeatedly told us that in the last 18 months the inclusion of fertility benefits in any large company employee health insurance plan has gone from a nice-to-have for a few very successful companies to a must have for any employer who wants to compete for young talent and who wants to be seen as committed to equity and inclusion in the workplace. We look forward to the results of Progyny’s selling season as the company benefits from reduced pandemic distraction, greater-than-ever awareness and importance to their potential clients, and the largest new client pipeline in company history.

Powered by rapid growth in new agents, continued progress in agent productivity, and an easy comparison on contingency commissions, we believe Goosehead will continue to grow at a very fast clip (>30%) even if the housing cycle proves to be something of a headwind at some point. Additionally, the recently developed client facing technology which enables consumers to get an extremely accurate quote within a minute based on just a handful of easy inputs should improve agent productivity by easing the referral process. Sorry to be the bearer of bad news, but after the industry suffered significant losses in 2021, including industry-leader Progressive having its highest combined loss ratio in 20 years, your homeowners and auto insurance rates will be going up a lot. The good news is that a Goosehead agent can help you minimize the impact (we can put you in touch with a good one!), and your investment in Goosehead will directly benefit from the increased rates (more on that below).

Interactive Brokers will finally get the benefit of higher short-term interest rates as the Federal Reserve raises rates. The leverage across tens of billions of cash earning very little if anything will be very positive with the first 25 basis points increase in rates, for example, adding $165 million annually in revenue with essentially no incremental costs.

Datto will benefit on the heels of much greater awareness of the issue of cybersecurity in the small and midsized business area. A flurry of new security offerings and continued growth in their base of managed service provider (MSP) partners should power strong performance in 2022. The compounding need for IT security and the complexity of those solutions will play out for decades to come.

We expect Floor & Decor will also greatly outgrow its industry as lingering supply chain issues squeeze the unfortunate local suppliers that cannot get inventory at reasonable prices if at all. The average home in America remains ~40 years old, and rising home equity levels will help fund the necessary improvements. 2022 should also be the year where Floor & Decor begins flexing its muscles around the very large and untapped commercial opportunity, further adding to their growth runway. We look forward to their Investor Day, March 16. Who knows? Maybe we’ll even see their newest shareholder, Warren Buffett.

We anticipate rebounds in the two stocks that were our decliners in 2021. Repay executed very well in 2021, but its stock was dragged down in a case of guilt by association. Tons of money flowing into “fintech” companies has understandably worried investors about the future of pricing in electronic payments. At last, the fees associated with basic, commoditized payments may head lower, and as a result, 2021 was a brutal year in the normally cushy world of payment company stocks. However, Repay’s offerings are integrated with valuable software that is very unlikely to be ripped out and replaced, and they operate in markets that are extremely underpenetrated when it comes to electronic payments to begin with. So, they are very far from the mature, commoditized payment world which may be at risk. Their “take rate” has remained remarkably steady and actually increased in 2021 due to a very logical and strategic acquisition. We expect accelerated organic growth, and that growth coupled with continued high levels of profitability will distinguish the company from the lower multiple mature players and should drive very good 2022 performance for us.

Lastly, Avalara will benefit from tax jurisdictions increasing enforcement, from their expanded product line driving cross-sell opportunities and from their successful early penetration of the marquee enterprise market. We think Avalara, like Repay, is currently being dragged down in a case of guilt by association related to the unsustainable growth of e-commerce during the pandemic and the resulting inevitable slowdown. Avalara provides tax calculation and remittance automation solutions for e-commerce companies and is integrated into many e-commerce platforms like Shopify. So, while pure e-commerce companies are still a distinct minority of Avalara’s clients and revenues, they have clearly benefitted from the rapid growth of e-commerce and should continue to do so as e-commerce and omnichannel commerce continues to grow. However, even within that ecommerce client base, their revenues are less sensitive to e-commerce activity levels or transaction values. Although, Avalara’s fees get adjusted modestly in the case of a significant increase or decrease in the number of transactions, the reality is that what they charge is much closer to a fixed cost. The stock market is reasonably anticipating a reopening of the economy and a deceleration in ecommerce growth, and the first few weeks of 2022 have been punishing for anything related to ecommerce including Avalara and other leaders like Shopify. We think that during 2022, Avalara will prove the resilience of its model and its ability to continue its 20%+ growth separating itself from the pack and heading higher.

Topics du Jour:

With turmoil and volatility in the markets, and with our not having a new name from Q4 to write about (by the way, we have a doozy we’ve added in Q1 that we will write about next letter), we will deviate from our normal approach and try to share some thoughts about commonly discussed issues and their impact on our portfolio companies.

Inflation / Interest Rates

My take on inflation has always been informed by a pearl of wisdom I received from a company CEO that I think of as one of my 30 second MBAs. At a time when diesel fuel was approximately $2 a gallon but rising quickly, a trucking company CEO said to me, “Philip, look here, if you run the lowest cost, most efficient, most conservatively financed trucking company, you wake up everyday praying for $5 diesel fuel. Sure, it will cause you some shortterm heartburn and pressure margins, but it will crush the weaker players and force them out and allow you to gain share faster than you can ever imagine in a normal operating environment. And in the end, you’ll make tons more money.”

Having grown up in an era when it was crucial to understand the differences between LIFO and FIFO accounting on the quality of earnings, I have enormous respect for the impact of prices going up. Predicting levels of inflation however, is a challenge (the Fed got it wrong this year, and everyone else got it wrong coming out of the Global Financial Crisis money printing). Rather than move around the portfolio based on our anticipation of inflation and hence interest rates, our approach has always been focused on finding companies that will directly or indirectly benefit from inflation-related turmoil. This leads us to low-cost leaders that can pass on price increases better than weaker players, and those with the best balance sheets that can avoid the trauma of rising debt service. For example, we have already discussed how if your Goosehead arranged insurance policy premium goes up by 6% this year, Goosehead will make 6% more in commission without doing an iota of extra work. Interactive Brokers’ tens of billions of dollars sitting uninvested in client accounts or on its own balance sheet will now start earning hundreds of millions of dollars with just the first interest rate increase. With dominant market share and a wealth of new product innovation, Armstrong World Industries has been able to put through multiple price increases to defend and ultimately grow margins in ways competitors cannot. Avoiding financial leverage allows our companies to ultimately feast on the carcasses of overleveraged companies whose CEOs made the mistake of taking modern finance theory in college. Ensign will be in aggressive carcass-feeding mode while weaker players give up. And Floor & Decor will gobble up share against smaller players lacking the toolset to deal with sudden cost increases. As if to prove the point, Floor & Decor reported comparable stores increased 14% in the fourth quarter, while its closest direct competitor LL Flooring, parent of Lumber Liquidators, reported that their comparable store sales fell 7% in the same period: an amazing differential. Current inflation is clearly exacerbated by some temporary factors including government stimulus, COVID impacts, and supply chain issues, but inflation is a gnarly problem that is not going away any time soon and is not easily solved in the short run. It is a tragic confiscation of the buying power of those who labor at the bottom tiers of society and of those on fixed incomes without savings. Ultimately, however, as Warren Buffett has pointed out, the solution to high prices is high prices. High prices will attract new capacity and will lead, in time, to lower rates of inflation. We should do really well in that environment too.

Inflation / Labor Shortage

Wage pressures extending across the economy are extraordinary for a peacetime economy. This strain reinforces one of the great advantages of owning growing companies – the ability to offer advancement opportunities that mature or marginal companies cannot and hence the ability to attract and retain better, more motivated and more loyal workers. Part of the reason Floor & Decor was able to put up such outstanding fourth quarter sales compared to LL Flooring is that its productivity allows them to pay higher wages to attract more capable entry level employees, and the prospect of still more than tripling the store count and expanding into the huge commercial market keeps those employees showing up and motivated to move up. Ensign’s growth model allows it to have industry leading employee retention and the lowest use of temp nurses, who typically constitute two or three percent of their nursing pool in an industry where it is commonly 20%-30%. This is an enormous advantage in an environment like today which has seen the going rate for temp nurse surge from $40$45 a year ago to $80 - $90 today.

Lastly, innovative and differentiated business models are more productive and don’t require lots of people. Our median company produces $400k of revenue and $80k EBITDA per employee which compares very favorably to a small-cap median of $350k and $36k. Our average skews even higher led by the incredibly productive Interactive Brokers which will produce more than $1M of EBITDA per employee in 2022, more than double the rate for Microsoft (no slouch) and 60 times the rate for Walmart.

Inflation / Supply Chain Issues

We believe supply chain issues across the economy will gradually get better but it will take frustratingly long to get there. Further, absent a significant change in corporate and governmental behavior and priorities, our supply chain will remain substantially less robust and resilient compared to where it should be and compared to other nations that have invested more heavily in relevant infrastructure. As to the fundamental cause of the problems, the best commentary we have read is from an interview with Ryan Peterson, founder and CEO of Flexport, a supply chain software company. We share this with you because we believe he is correct but also because the same issue is the root cause, in our opinion, of many problems we see and why we prefer investing in long term, owner-oriented businesses, rather than those with professional care-taker managements. He says “In my opinion, what’s caused all the supply chain bottlenecks is modern finance’s obsession with Return on Equity (ROE). To show great ROE, almost every CEO stripped their company of all but the bare minimum of assets. ‘Justin-time’ everything with no excess capacity, no strategic reserves, no cash on the balance sheet and minimal investment in R&D. We stripped the shock absorbers out of the economy in pursuit of better short-term metrics… And let’s not forget the human aspect of the workforce that makes this all happen. A lot of companies in the industry haven’t invested in taking care of their people, especially during market downturns, so now they can’t staff up quickly to meet surging demand. When the floods inevitably hit, the survivors will be those who invest in excess capacity, in strategic reserves of key capital assets, in employee trust that let them attract and retain talent.”

Stock Market Volatility

If you ever hear us go on at length about the advantages of our model and our investing in liquid and occasionally volatile public markets, you know that it is heartfelt and logical. The market is there for us to access if we want to, otherwise we can ignore it. So, this occasionally vexing and time-consuming element of the public markets is an advantage for us in that we have a standing offer at all times to buy or sell. All other things being equal, easy liquidity is better than illiquidity even if only half the time or less it values the company fairly and rationally. But the advantages of public market access are particularly pronounced for those running highly concentrated portfolios and who have done the primary research needed to understand the true long-term value and to develop true conviction – neither of which are possible when the PM has not done the work personally or is responsible for a portfolio of dozens or even scores of names. As David Swensen wrote in Pioneering Portfolio Management, “Concentrated portfolios provide focused exposure to a manager's best ideas, avoiding the lack of conviction inherent in a diversified portfolio.” And later in Unconventional Success he also wrote, “Courage of conviction stands investment managers in good stead, as willingness to initiate and hold out-of-favor positions plays a critical role in taking advantage of true investment wisdom. All too often, the difficulty of maintaining a contrarian stand turns what should been profits into losses.” So, we say “Bring on the volatility!” Without it we cannot take full advantage of those whose diversification dramatically dilutes any ability to know the company more than superficially and those who took on short-term oriented clients forcing them to make decisions based on marketing-related externalities rather than long-term value. And if the price of prime tenderloin goes down temporarily, the smart carnivore stock ups and fills the freezer.

Stock Market Volatility / Sector Rotation

As 2021’s meme stock mania showed, the stock market’s fashion du jour does not even need to be tied to the real economy or real value. But since the dawn of markets, sectors of the market have come in and fallen out of fashion like hem lines on skirts. Like the general market volatility discussed above, we like to take advantage of sector rotation often by adding positions when their industry is out of favor and lightening or exiting a position when the industry is all the rage. There is more behind this logic than just getting a good price. A company’s industry going out of favor means that Wall Street’s dollars are going elsewhere allowing leaders to more easily go unchallenged, while popularity brings the risk of new capital changing industry dynamics.

There are certain industries and sectors we intentionally stay away from because they are typically driven by unknowable macro factors and are difficult areas to build a special, growing, capital-light business. Energy and commodities are examples as are big balance sheet financials, like banks. We understand the temptations to speculate with commodities and capital-intensive businesses, and even crypto for that matter. Oil trading below zero in 2020 seemed very oversold, for example. And consistent with the discussions above, a lack of new investment for capacity would likely bring higher prices. But, to us, jumping in and out of sectors is a trader’s game, not investing. And very few can get both entries and exits right consistently. Energy, for example, has seen more than a decade and a half of secular decline until this recent rally. There will be times when we are left out and lagging because we do not own banks or commodities including energy, but history has proven again and again to our satisfaction, that riding the coattails of a couple handfuls of great companies is a much easier game to win and win big.

Stock Market Volatility / Growth vs. Value

We have always bristled at the question “Are you growth investors or value people?” After all, how can you value anything without factoring in its level of growth? To answer “growth” implies you don’t care about valuation, which is a bad idea and an easy way to lose money. To us, answering “value” implies you only own second rate, stagnant companies that over time can never keep up with growing and investing companies.

But if you put a (proverbial please) gun to our head and forced us to answer one or the other, we would say “growth”, and then add, “but with an absolute return mindset, the hatred of losing money and the insistence on a ‘value’ entry point where the key drivers of long-term stock performance – revenue growth rate, operating margin and trading multiple – are coiled setting up a ‘triple win’.” This approach is consistent with the fact that we do not view things in style-box terms but only through the lens of how we can maximize our long-term returns.

Two beliefs most prominently inform our view on growth stocks vs value stocks. First, we have heard repeatedly from people in the real economy, as opposed to those trading pieces of paper or opining from an ivory tower, that this is increasingly a winner-take-almost-all economy. This makes intuitive sense when you think about it.

As capital replaces labor, cost structures get more fixed allowing the lower cost guy to justify more marginal pricing and more incremental investment to either further lower prices or improve the customer experience in other ways. The world has changed dramatically in the last 25 years with advancements in technology, global competition and transparent global supply chains. Those companies that are statistically cheapest are generally marginal players in their industry or in unattractive industries to start with. Regression to the mean is a powerful force and supports the idea of fishing amongst value stocks when they are statistically well below trend. But this assumes the mean is constant and not in secular decline. Marginal players who have not made the necessary technology and people investments to make life better and easier for their customers are becoming modern buggy whip purveyors.

The second and largest reason we would unapologetically answer “growth” is strategically straightforward. We have huge advantages in the marketplace by being capacity constrained, concentrated, primary research driven, and only available to true “investors” who have an appropriate investment time horizon. It makes no sense being a “cigar-butt” value investor when you have those advantages. As we see it, smaller, less liquid, less followed, less understood, high quality compounders are the ultimate way to leverage our structure and focus and are happily also the best way to have great long-term returns. If your opponent has cornerbacks and safeties that are 5’9” and your receivers are 6’5”, then you throw the ball. And you win.

Stock Market Volatility / Current Destruction of the Stocks of Companies Losing Money

This is the best news we have had in a while. If asked, “what’s the greatest risk to the durability of the moat surrounding any of our portfolio companies?”, the honest answer is the seemingly endless eagerness of earlystage investors to indefinitely fund even flimsy business models that are untethered from the real world need of at least a prospect of eventual profitability and self-sustainability. The current concerns about inflation and interest rates are shortening investors’ time horizons and splashing cold water on the infinite timeline to profitability concept and causing a massacre of the stocks of small-cap unprofitable companies. This action brings to mind something of a corollary to the trucking CEO’s inflation prayer. In this case, if you are profitable and well financed and never need to access the capital markets, you pray every day that Wall Street shuts down, closing the spigot.

Take Goosehead Insurance, for example. Founder Mark Jones personally absorbed all the early losses, and now the company is very profitable, cash-generative and even able to pay special dividends despite growing well north of 30%. The would-be quasi-competitors that have sprung up and gone public in the “insuretech” space include Lemonade (LMND), Metromile (MILE), Root (ROOT) and Kin Insurance. In the last year or so, LMND fell from nearly $200 to below $20, MILE fell from $20 to below $1 and gave up and sold itself at essentially no premium, ROOT fell from close to $30 to under $2, and Kin Insurance’s attempt at going public got scrapped. Of course, the declines cannot happen in complete isolation or without impacting the stocks of peers, so GSHD has had its share of volatility and is down maybe 25% during that time. But it’s relative stock performance, like its fundamental performance, has been stellar.

In the case of Interactive Brokers, money-losing-would-be-competitor Robinhood’s stock hit $90 last year valuing it more highly than IBKR, but it collapsed to single digits earlier this month. By the way, in terms of pre-tax earnings IBKR put up roughly $1.8 billion in 2021 while HOOD lost roughly $3.7 billion. This health restoring dose of rationality benefits all of our companies, and those who held to those fantastic dreams promised by the money-losers only to see harsh reality crush their dreams and separate them from their money may be left pondering the warning held in the last lines of Shakespeare’s Sonnet 94:

The summer’s flower is to the summer sweet,

Though to itself it only live and die, But if that flower with base infection meet, The basest weed outbraves his dignity.

For sweetest things turn sourest by their deeds;

Lillies that fester smell far worse than weeds.

And the Above Logically Leads to…

As is often the case, the market, in all its algorithmic wisdom, may be indiscriminately throwing out the baby with the bath water. It may not come as a surprise that with the carnage taking place among the stocks of the not-yet-profitable, we searched that pool aggressively and found a gem of a great growth business that is changing a huge industry, but which is not yet profitable, although it will be by the end of 2023 and has much more cash than needed to be self-funding to that point and well beyond given modest cash needs. Since coming public last year (traditionally, not via SPAC), the company has exceeded the high end of what could have been expected while those they are disrupting have struggled, consistent with our thesis. And yet, the stock is more than 50% below where it traded on its opening day. As usual, we are zigging, while others are zagging. We are excited to talk about the company, but we are still building the position so that discussion is for the next letter.

Investment Program:

For the benefit of any first-time readers, the hallmark of the Owls Nest Partners approach is the purchase of industry leading growth companies when a temporary headwind has recoiled the fundamental growth drivers and compressed its multiple. This typically happens as hot money “renters” exit and drive the price down. There is no such thing as a free lunch: we can only receive our requisite value if we accept that our companies will appear “catalyst-less” and uninteresting for some time. We believe we are wildly overcompensated for this modest level of patience, especially since it is in these moments that a company can invest in its own business with the highest returns. There is wonderful optionality associated with a well-run, shareholder friendly, cashladen company that is able to aggressively put money to work during a temporary headwind.

It is our belief (and experience) that our future outperformance will not be driven by any economic or market forecasting prowess but instead by ten unique investments, each playing out over time. We perceive these investments to have modest downside due to high quality and low expectations, and very significant upside as growth and margin expansion return in spades. We seek reasonable ballast and diversification within the portfolio as a result of our natural conservatism (strengthened by our co-investment alongside clients) and our predisposition to avoid crowded trades and instead invest in temporarily out of favor areas.

Final Thoughts:

We hope you and your family remain safe and well.

More than ever, we thank you for your support and for choosing to have your money working alongside ours.

Gratefully,

Philip & the Owls Nest Partners team

Disclaimer

In General: This disclaimer applies to this document and the verbal or written comments of any person presenting it. This document has been prepared by Owls Nest Partners IA, LLC as Investment Adviser (the “Adviser”) of Owls Nest Partners Concentrated Long Only SMA (the “Strategy”). By receiving this document you acknowledge that you are an investor in the Strategy, or a prospective investor who is known to the Adviser, and that you meet all regulatory definitions of “Accredited Investor” and “Qualified Client,” in order to be considered a prospective client of the Adviser. The information included herein reflects current views of the Adviser only, is subject to change, and is not intended to be promissory or relied upon. There can be no certainty that events will turn out as the Adviser may have opined herein.

No offer to purchase or sell securities: This document does not constitute an offer to sell (or solicitation of an offer to buy) any security and may not be relied upon in connection with the purchase or sale of any security.

No reliance, no update and use of information: You may not rely on this document as the basis upon which to make an investment decision. To the extent that you rely on this document in connection with any investment decision, you do so at your own risk. This document is being provided in summary fashion and does not purport to be complete. The information in this document is provided you as of the dates indicated and the Adviser does not intend to update information after its distribution, even in the event the information becomes materially inaccurate.

Knowledge and experience: You acknowledge that you are knowledgeable and experienced with respect to the financial, tax and business aspects of this presentation and that you will conduct your own independent financial, business, regulatory, accounting, legal and tax investigations with respect to the accuracy, completeness and suitability of this information, should you choose to use or rely on this document, at your own risk, for any purpose.

No tax, legal or accounting advice: This document is not intended to provide and should not be relied upon for (and you shall not construe it as) accounting, legal, regulatory, financial or tax advice, or investment recommendations. Any statements of U.S. federal tax consequences contained in this document were not intended and cannot be used to avoid penalties under the U.S. Internal Revenue Code or to promote, market or recommend any tax-related matters addressed herein.

Confidential information and distribution: By accepting receipt or reading any portion of this document, you agree that you will treat all information contained herein confidentially. Any reproduction or distribution of this document or any related marketing materials, as a whole or in part, or the disclosure of the contents hereof, without the prior written consent of the Adviser, is prohibited.

Suitability: Any investment program involves a high degree of risk and is suitable only for sophisticated investors who meet certain other suitability standards.

Investment strategies, market conditions and risk disclosures: Notwithstanding the general objectives and goals described in this document, readers should understand that the Adviser is not limited with respect to the types of investment strategies it may employ or the markets or instruments in which it may invest. Over time, markets change and the Adviser will seek to capitalize on attractive opportunities wherever they might be. Depending on conditions and trends in securities markets and the economy generally, the Adviser may pursue other objectives or employ other techniques it considers appropriate and in the best interest of the Fund. No representation or warranty is made as to the efficacy of any particular strategy or actual returns that may be achieved.

Investors must be prepared to bear the risk of a total loss of their investment.

Projections: This document may contain certain “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of the Strategy’s investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

Disclosures

- Past performance is not indicative of future results. Performance presented from inception through September 2020 is for a representative account of the Owls Nest Partners Concentrated Long Only strategy (the “Strategy”). As of October 2020, performance is for a composite of separately managed accounts managed in accordance with the Strategy (the “Composite”). Performance is presented gross and net of all fees, as of the date listed at the top of this document. The fees applied are the prevailing fees of the Strategy at the time such performance was generated. From inception to the date of this document, the fee structure applied is a 1% annual management fee, and 15% performance fee that is charged only on the outperformance of the Strategy to the Benchmark (as defined below), and only after five years. Performance fees are accrued monthly. All performance is calculated by the Adviser and represents preliminary, unaudited figures that are subject to change. Further information regarding the Strategy or the Composite can be provided upon request. The Adviser does not claim compliance with the GIPS reporting standards and the performance presented herein has not been audited or verified by any third-party.

- The Russell 2000 Total Return Index (the “Benchmark”) is a broad market index that is presented for comparative purposes as the performance benchmark to the Fund. The Benchmark is an unmanaged index consisting of the smallest 2000 stocks in the Russell 3000 Index. The stocks are issued in the United States, and the Benchmark includes the reinvestment of all dividends and income. Because the Benchmark is unmanaged, it assumes no transaction costs, management and performance fees, or other expenses. Unlike the Fund, it contains only domestic companies and is rebalanced monthly. Therefore, while the Benchmark contains publicly traded companies, it does not purport to represent an exact performance comparison to the Strategy. It is not possible to invest directly in an index, such as the Benchmark

- The Standard & Poor’s 500 Index is a domestic equity market index that is presented for comparative purposes only (the “S&P 500”). The S&P 500 is an unmanaged index consisting of largest 500 companies by market capitalization having common stock listed on the NYSE or NASDAQ. The S&P 500 index components and their weightings are determined by S&P Dow Jones Indices. Because the S&P 500 is unmanaged, it assumes no transaction costs, management and performance fees, or other expenses. It is not possible to invest directly in an index, such as the S&P 500. In instances where insufficient data is available for the Benchmark, the S&P 500 has been used as a proxy for the broader domestic equity market.