- Responsible for new idea generation; portfolio construction; risk management; due diligence

- 25+ years overseeing concentrated small-cap portfolios, on behalf of the most sophisticated allocators in the United States

- Previously: Founder, Endowment Capital Group; Portfolio Manager, Downtown Associates; Analyst, W.H. Newbold’s Son & Company

- University of Pennsylvania, Wharton School, B.S. 1986

- Married to Isabella, 3 sons, 3 daughters, 2 dogs

by Owls Nest Partners on Dec 31, 2022

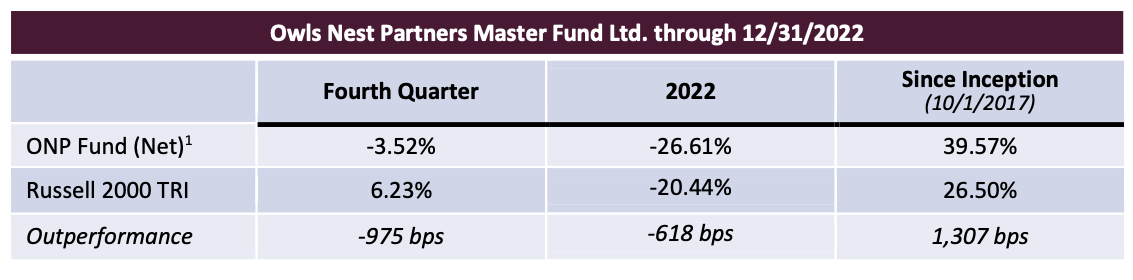

Performance:

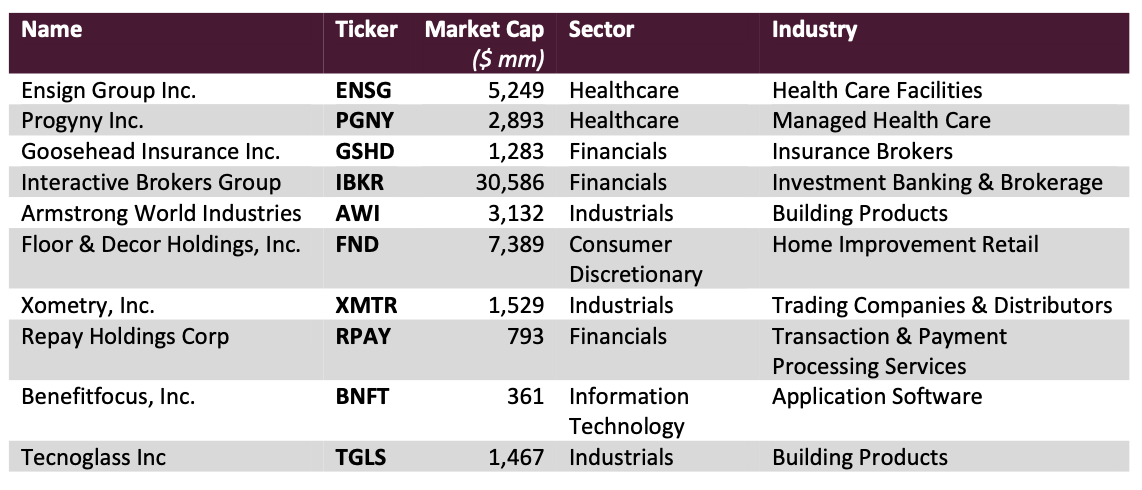

Holdings as of 12/31/2022:

We ended the quarter with the following holdings (in order of position size, largest to smallest):

Median Total Debt/Market Cap: 9.8%

Median Market Cap: $2,198 million

Active Share vs. Russell 2000: 99.5%

1Past performance is not indicative of future results. Performance presented from inception through September 2020 is for a representative account of the Owls Nest Partners Concentrated Long Only SMA strategy (the “Strategy”). As of October 2020, performance is for a composite of accounts managed in accordance with the Strategy (the “Composite”). Please see the Disclosures at the end of this document for further information with regards to performance.

Quarterly Attribution:

Reflecting investor unease about the economy, our biggest gainer among our core positions in the quarter was the ever-steady skilled nursing facility operator, Ensign Services (ENSG). Ensign again reported record profitability despite a tough labor environment, and they announced a large acquisition on very favorable terms that was available to them because the extended challenging operating conditions are bringing many other operators to their knees. Interactive Brokers (IBKR) was also a meaningful positive contributor as it benefits from higher short term interest rates which drive significant earnings for the company on the tens of billions of dollars that they have either as their own excess capital or in client accounts. This cash was unproductive only a year ago but is now generating great income despite IBKR’s commitment to pay the highest rate in the market to their customers. Repay (RPAY), Tecnoglass (TGLS), Avalara (AVLR), and Goosehead Insurance (GSHD) were more modest positive contributors.

Xometry (XMTR), which had been a star performer in the third quarter on the heels of outstanding Q2 results, gave back almost all of the prior quarter’s gains when their Q3 results disappointed. Mercifully, we trimmed the position last quarter into that strength, but nonetheless the stock’s decline had a meaningful impact on our Q4 results. Recall that Xometry operates a marketplace for custom manufacturing. Significant commodity deflation, yes deflation, and pockets of excess capacity among suppliers led to orders being accepted by suppliers at lower prices. Ultimately this setback perversely bodes well for Xometry in that it reinforces the value of the marketplace to suppliers who were able to gain acceptable orders for their capacity which otherwise would have sat idle, as well as for the buyers who profited from even lower prices as their orders were matched effectively with that capacity that they otherwise would not have found. But in the short term, lower prices equate to lower revenues for Xometry. We discuss the current challenges and very positive long-term outlook in more detail below.

Progyny (PGNY) also detracted from the quarter’s results despite actually raising earnings estimates in the quarter. Progyny is the leading provider of managed fertility benefits to large employers. The market is concerned primarily about the impact of layoffs at large technology companies, many of whom are Progyny clients. The issue is real, but we think it is dramatically overestimated given Progyny’s diverse customer base in which more than 80% come from outside tech, and the fact that they have modest single digit penetration of their core target market while having near 100% client retention, outstanding outcomes, and no direct competition able to offer a similar service. Armstrong World Industries (AWI) also declined somewhat, and Floor & Decor (FND) was a very modest negative performer.

Portfolio Adjustments:

The acquisition of Avalara closed in the quarter, so we exited that position. We lightened up on Interactive Brokers since it rallied nicely. We added to almost all other positions, but our largest increases were in our Goosehead Insurance and Repay positions.

2022 Attribution

With a rate hike inspired bear market and coming on the heels of a strong 2020 and 2021, 2022 had few winners for us. Only Datto (MSP) which was acquired earlier in the year, Tecnoglass, and Ensign were up for the year. Our largest negative contributor on the year was Goosehead primarily as a result of tremendously reduced profitability in the personal lines insurance industry. Goosehead was followed by Progyny, Armstrong World Industries, Xometry, Repay, Floor & Decor, Avalara, Allegiant Travel (which was exited early in the year) and Interactive Brokers. Although there are recurring themes, each holding has a unique recent history and outlook, and given all the volatility in the economy and market we think it would be a useful exercise to review each of the core holdings. This letter we’ll start with four of the most important holdings, and we’ll discuss the others in the next letter.

2022 in Review for Our Companies and Expectations for 2023

Stock prices are volatile reflections of fear and greed, and their changes may or may not be closely tethered to the progress or regression of the underlying company. If dwelling on the 2022 stock performance, one might be surprised to learn that our portfolio had median revenue growth of more than 25% in 2022 over 2021, and also enjoyed median profit margin expansion of one percent. Looking at the average rather than the median, the year’s positive revenue and profit margin growth performance is even more robust at north of 32% and nearly 1.5%, respectively. Hardly disastrous. And when coupled with the decline in stock prices, one can easily grasp the exciting improvement in valuation.

Few companies are unaffected when abundant liquidity in the economy and in the markets quickly evaporates as a result of the most dramatic increase in interest rates in four decades. The inhospitable desert left behind is a challenging environment, but it can be very advantageous in the long run for companies well prepared for such an environment due to superior business models and financial strength. These companies can benefit from the optionality created by exceptional opportunities that present themselves in harsh times and from a less crowded market as weakened competitors die on the road. So, it is important to look at a year in review not only in terms of what progress was made in that year, but also in terms of how the prospects of arriving at the ultimate hoped- for destination evolved.

The Four Largest Positions

Ensign Services:

The environment in the skilled nursing industry continues to be very tough as a litany of hardships including increasing regulatory burdens, demanding payors including fast growing Medicare Advantage payers, a tight nursing labor market driving huge wage inflation, higher rents/higher financing costs, and the wind down of COVID support lifelines all compound miseries for subscale players. There are approximately 15,000 skilled nursing facilities in the country, and the median facility does not make money after rent. However, Ensign’s unique combination of hyper-focused and empowered local management at the facility level supported by the best practices, financial strength and scale of one of the industry’s largest players continues to pay rich dividends. For 20 years, Ensign has executed and refined a playbook designed to earn the trust of all the referral sources in their immediate community through great care, great outcomes, and leading systems for sharing data with those referral sources, which has in turn driven a client mix of higher acuity patients as opposed to filling beds with simple, low margin custodial work.

Impressively, Ensign managed to grow revenues and earnings in the mid-teens in 2022 despite being impacted to some extent by labor challenges which can require them to turn away business. In addition to the organic growth it generates in its existing facilities, Ensign grows by acquiring the businesses of small operators who cannot make the necessary investments to get the talent, systems, and scale needed to prosper. Ensign has been an opportunistic but disciplined acquirer for two decades with an unequaled track record. Acquisitions at distressed prices yield fantastic returns once Ensign installs its management and systems and builds that facility’s reputation in its local market. The cash-on-cash returns are so great, in fact, that since its IPO in 2007 Ensign has grown by 635% but has never needed to offer any additional equity and remains by far the strongest and most liquid player in the industry. Ensign’s opportunity set is expanding in unprecedented ways as a result of broader industry pressures, and 2023 and 2024 promise to be great years for Ensign as smaller players cry “uncle” and capitulate and sell out to a consolidator at very attractive prices. And with less than 2% of the industry, Ensign has ample room to grow. Longer term, there is also the interesting demographic development as the “silver tsunami” strikes and the baby boomer generation enters the prime age for needing Ensign’s services. The number of facilities in this country has been shrinking for years. A huge new and inexorable wave of demand without an easy way to accommodate it may lead to very interesting possibilities for Ensign and even turn a sleepy, consistent and profitable plodder into something of a glamour stock.

Progyny:

Progyny grew revenues and EBITDA north of 50% in 2022, and it completed a highly successful selling season that allowed them to guide to 2023 revenue growth of nearly 30% along with continued margin expansion. And this is on top of its track record which has produced cumulative revenue growth of 647% over the last four years (a 65% CAGR). And yet, Progyny saw its stock decline by 38% in 2022. For sure, investors were a tough crowd for growth companies in 2022. But that, in turn, sets the table for significant outperformance coming out of this market cycle.

We often invest in companies that do not have directly comparable “competitors”. We gravitate to such situations because they are more easily misunderstood and, hence, yield a much higher potential return for a given unit of risk. Our companies also tend to have business models which are more difficult to copy, providing a longer runway of growth and excess returns. No one else does precisely what Progyny does. There are companies with cute apps or other superficial solutions to part of the fertility benefit problem, but no one has the robust national network of the best clinics in the country, integration with all the leading claims administrators, the unique plan design to efficiently allocate resources and dollars, an integrated pharmacy offering to assure cost savings and timely delivery of drugs, huge scale to drive efficiencies and savings to pass on to clients, and the much needed hand holding and guidance from patient care advocates. No one else can deliver the outcomes that they produce, which thrill their clients and drive essentially 100% client retention and rapid growth. Progyny is the brand in its space and is the only provider with history, data, and large referenceable clients. Why would you even consider going elsewhere? Before a company hires Progyny, they may offer their employees no fertility benefit at all, or they may offer a limited cash reimbursement as the employee navigates the private pay healthcare system on their own with no support and a very limited budget. Imagine a self- respecting employer saying, “Sorry to hear about your brain cancer diagnosis. Here’s $10,000. Good luck.” Yet that remains effectively the most common manner of handling infertility diagnoses by employers today, even large, sophisticated ones.

The status quo “good luck” strategy of going without a managed fertility benefit is clearly unsustainable and collapsing. And not just for reasons of equity. One by one, the leading companies in many industries have adopted Progyny, which causes all the dominoes to fall over time as other companies in each of those industries discover the challenges of recruiting scarce talent when a competitor enjoys the halo of a strong culture, evidenced by offering robust benefits including the one that is most important to a 30-something. After all, infertility affects one in five couples in America of child-bearing age. Progyny enables companies to do the right thing, attract and retain talent, produce vastly superior clinical outcomes with a program that largely pays for itself with the hard savings that come from reduced expense on the back end that would otherwise have to cover the costs of complicated, premature and multiple births. And with only single-digit penetration of its initial target market, there is no wonder why Progyny’s outlook is so strong.

Xometry:

Xometry gets a little extra ink in this letter because it has gone from hero to goat (not G.O.A.T) in a matter of 120 days. If you want to skip this section and the sordid details, just takeaway that after many hard questions of management, probing many customers and suppliers, and more than a little self-reflection and contemplation, we believe Xometry will once again be a hero for us (and maybe even a G.O.A.T.).

Xometry is our earliest stage and fastest growing company. Alone among all of our companies, it is still in investment mode and not yet profitable, although the hundreds of millions of cash are more than enough to see it through to full self-funding. Although we have built a portfolio dominated by companies with industry-leading profitability and financial strength, we believe there can and should be a company with Xometry’s profile in our portfolio when the quality and uniqueness of the business model and the potential to positively and profitably alter a massive industry drive enormous potential upside. While it is extremely early in its journey relative to their opportunity, Xometry is very far along in proving the unique utility and ultimate scalability of the only true digital marketplace for the enormous custom manufacturing industry. Even with some heartburn at the end of the year, Xometry had a strong year growing total revenue 75% (organic revenue growth was over 40%) and drove solid performance across all key performance indicators. Active buyers grew by 45%, revenue per buyer grew 3.6%, the number of buyers spending over $50,000 increased 47%, and the number of active sellers grew 22%. Xometry’s 2022, however, was a tale of two halves. In the first half of the year, they accelerated beyond our expectations, and the stock soared. In the second half, they seemed snakebit.

In the third quarter, orders were very strong, but pricing reversed and headed down sharply and unexpectedly. Xometry’s pricing algorithm works generally like this: someone submits a computer-aided design (CAD) rendering of an item they need made and requests a production quote in which they specify the quantity to be manufactured, the modality of manufacturing to be used (e.g. injection molding, CNC, sheet metal, 3D printing, etc.), the required level of tolerance, the required time frame, and any geographical requirements or required certifications. Applying machine learning to its huge database of prior orders and the knowledge of its more than 2,400 active suppliers in its network of manufacturers, Xometry estimates what it will cost to manufacture the item, slaps a margin on that, and returns a real-time quote for the production of these never-before-built parts. It’s actually quite miraculous. This process replaces a manual and time-consuming back and forth process. And while other companies can today accomplish narrow pieces of what Xometry does, the breadth of its offering and the fact that they own no equipment and hence are impartial, and the implementation of the latest technology on top of the largest database of prior orders, effectively makes them the New York Stock Exchange for custom manufacturing.

Once the buyer approves the quote and an order is confirmed, Xometry queries its database of suppliers and offers that order to certain suppliers based on the quality of the match – basically how well this supplier has done before manufacturing similar parts and how likely this supplier will be able to make these parts at the lowest possible all-in price. If the first person doesn’t accept the order, they offer it to others and gradually increase what they are willing to pay for the piece, decreasing Xometry’s margin since the price at which they have to deliver it has already been set. This is brilliant, but it is unprecedented at scale, and impossible to refine without a few bumps along the way. Xometry has had great success getting better at the “match” as it has scaled – this is a big moat for any future competitors – and has seen enormous gross margin expansion over the last twelve quarters (from 18% to 27%) as a result. As a young company, Xometry has generally operated in an environment of stable or increasing prices and of stable to strong economic activity, which leads to stable or tight manufacturing capacity utilization. By the middle of Q3, the backdrop had suddenly and dramatically changed. The price of hot-rolled coil steel, for example, which had soared in 2021 fell over 40% from late May to mid-August. Costs to manufacture items went down, and Xometry’s matching algorithm got even better. Almost instantly, Xometry’s pricing algorithm adjusted, and pricing went down a lot. Customers were thrilled, and suppliers were happy to have good orders that kept their equipment humming. The sudden change of events, however, made for unhappy shareholders, including us, since a fixed margin on lower costs equals lower revenue and gross profit. We, in fact, have had “robust” conversations with the management over this algorithm not having old school, common business sense embedded in it. I know nothing about how to program an algorithm, but I know a fair amount about selling gasoline since I grew up in a family that owned convenience stores. As gasoline costs rise, you raise price quickly. As they fall, you take your time and max out a little margin opportunity. Xometry’s algorithm, instead, passed on all the benefits real time to the buyer, at its own expense. And based on our conversations with customers, this was completely unnecessary since customers buy from Xometry for many reasons other than price including breadth of offering, convenience, speed, and reliability. We should add that management wasn’t as obtuse as we make out above, and in fact we continue to hold them in very high regard. But this was new and happened quickly, and for better or worse, they had to gain a certain degree of experience before adjusting the pricing algorithm.

Q4 brought another new set of circumstances to train the algorithm, this time in the form of a sudden air pocket in order rates. In a newly disciplined financing environment, companies across the nation pivoted quickly to focus on profitability and cash generation for the year-end financials, and Xometry saw its quote-to-order conversion rate, which had risen meaningfully in Q3, slow suddenly and unprecedentedly. Rather than being completely passive, the company experimented to see if cutting price would stimulate conversion of quotes to orders. It didn’t. Pricing wasn’t the problem. People were simply pushing out future orders. In the end, overriding the algorithm by lowering price simply cost the company extra margin. All of this is frustrating to us, but the conversations with customers and suppliers have been more positive than ever. Counterintuitively, these issues should actually demonstrate and reinforce the strength of Xometry’s position. Q3’s issues speak to how eager suppliers are to get business from Xometry which in turn increases the value to customers and Xometry’s gross margin opportunity. In fact, the company has accelerated its target date for getting to optimal mature gross margins. Q4’s challenges, in turn, showed that the customers have bought into the full value offering and aren’t as price sensitive as might have been suspected. Taken together, these two quarters show how difficult it is to build and scale such an operation, which is why others have failed to gain any traction. We’ve spent a great deal of time with management since the snafus. We appreciate their candor and humility, but more importantly we are convinced that they are on the right path and building an extremely valuable business.

Which, at last, brings us to 2023. 2023 is also likely to be the tale of two halves. It will take some time for the company to get back to revenue per buyer levels seen in 1H 2022, but this metric is improving and there will be a nearer-term recovery of gross margin. The most important metric, however, is the consistent growth of active buyers. Active buyers are expected to grow north of 30% in 2023, which provides a larger base for Xometry to drive their land and expand strategy. Xometry offers the breadth of processes, materials, and finishes along with the depth of global suppliers to be a one-stop-shop for prototyping, small batch production, and production runs for the largest businesses globally.

A conversation we had recently with a large customer best illustrates the land and expand/revenue-per-buyer growth opportunity for Xometry. The customer we spoke with spends roughly $1.5 billion annually on manufacturing related to new product introductions. 40% of that spend is with internal manufacturing capabilities, and the other 60% is split between over 500 small manufacturing shops. Today, Xometry captures less than 0.4% of that spend. Most of the small shops have long lead times, limited to no digital capabilities, and are incredibly difficult to manage. The Chief Procurement Officer at this customer said he and many of his engineers love Xometry and that he believes that over time Xometry can realistically grow to 20% of the total new product introduction spend as Xometry effectively manages and consolidates this spend and provides the incredible convenience and ease of compliance of one vendor to deal with. If this were to happen as this executive suggests, just this one company would give Xometry business roughly equal to its entire 2022 marketplace revenue. Relative to its current size Xometry’s opportunity is astonishing. The ride has had a few bumps of late, and we are guilty of missing a couple things ourselves including the extent of the tailwind of commodity inflation in 2021 and the offsetting headwind in the second half of 2022 from commodity deflation. But it is rare to own a clear leader with an opportunity in focus as enormous as driving the migration to digital manufacturing, and all of our work makes us more confident in their ultimate success.

Goosehead Insurance:

We own Goosehead because we think they have the best mousetrap in a huge and stable industry and a long runway of growth with barely 0.5% share in its industry nationally. Nothing that happened in 2022 dissuades us from our belief that the next five years will see them make great progress towards their ultimate goal of being the largest agent in personal lines insurance, which would require them to pass State Farm which is more than 25x their size currently. Goosehead delivered a strong year with total written premium growing 42%, policies in force growing 27%, and margins expanding by 3.7%. And this was accomplished according to some measures in the least profitable year for the industry in decades as claims costs soared with inflation, increased driving, and weather events. For example, loss claims for GEICO expressed as a percent as premiums increased in an unprecedented way from 74% in 2020 to a staggering 93% in 2022.

As an agent, as opposed to a carrier who bears risk, Goosehead doesn’t get directly impacted by underwriting losses. Hence, while Allstate actually lost money in 2022, Goosehead had a remarkably positive year by most accounts. But serving as a leading distribution arm of an industry makes it difficult to be impervious to the downturn in that industry. Goosehead was affected in two primary ways. First, appreciate that most carriers operate in highly regulated markets which makes it an arduous and long process to raise price sufficiently to cover the new level of losses. And what carrier wants to grow when rates are inadequate? Accordingly, many carriers withdrew from writing new business, especially in certain important geographies like Florida and California, limiting the ability of Goosehead agents to flex the full advantage of choice which accrues to their robust independent model representing approximately 150 carriers nationally. The bigger impact on the year’s P&L came from dramatically lower contingency commissions which are paid to distributors like Goosehead based on the profitability of the business they bring as well as the growth that agent brings to the carrier. Contingent commissions are inherently volatile in any given year for reasons that are out of Goosehead’s control, but they are an important long-term source of profitability especially since they have no direct costs associated with them and fall straight to the bottom line. Given the backdrop of underwriting losses at the carriers, contingent commissions collapsed in 2022. Compounding the macro challenges was the slow down in real estate transactions. People tend to passively renew their insurance until they buy a new home, at which point they actively shop for a new policy. That passive renewal habit contributes to the great value of what Goosehead is building because it is essentially an ever-increasing annuity. However, more real estate transactions and more shopping for insurance typically favors Goosehead since they have the superior offering. In Texas, for example, they were the insurer in more than 15% of the housing transactions in the most recent quarter, which portends staggering growth for a company with only 0.6% share nationally. But not all of the challenges Goosehead had to overcome in 2022 were macro in nature.

For the second straight letter, the early days of CarMax can be illustrative. CarMax was created in Richmond, VA as a side project for electronics retailer Circuit City (RIP). The model was refined, a degree of infrastructure was in place, and management decided it was time to expand. It was an era of good feelings, cheap money and dodgy initial public offerings (dot com bubble of late 1990’s), and CarMax was able to float an offering of “tracking shares”. The success invariably attracted competition, most prominently Wayne Huizenga’s AutoNation USA. Huizenga’s appetite for and creativity around doing deals was truly incredible, and at times he was thought to have a Midas touch. He would be a formidable competitor, or at least one with access to tons of capital. Feeling the need to lock up big markets before AutoNation, CarMax engaged in a land rush buying up entry into a number of big, expensive markets, notably South Florida and Texas. CarMax had to make certain assumptions as they tweaked their midsize market model to large, urban markets. How much land did they need? How many cars did they need in inventory? How far would people drive to save $500 on a car? The battle for used car supremacy began, and soon it was clear that both were losing as result of rolling out untested business models. CarMax had guessed wrong. They overbuilt and lost money, overburdened with overhead. AutoNation’s situation was worse because they had been financial opportunists without any real and proven model. They capitulated in December 1999, closing all 23 locations and laying off 1,800 people. CarMax, on the other hand, quickly adapted, selling off excess real estate and shrinking inventory and changing the configuration of stores in major metros. CarMax’s stock sank as confidence was lost. Even its IPO underwriter dropped research coverage of them, but the changes were working. The numbers were obscured by the runoff of the costs associated with prior sins, but proforma for that adjustment the stores began making good money. And wonderfully, the competitive environment was infinitely better than it had been. AutoNation was gone, and it had become impossible for a new entrant to raise money for a used car only concept since it was now general knowledge that you could only make money as an auto retailer if you had both used and new cars, and service. The rest is history. CarMax expanded and was a 150 bagger off those lows as it grew unchallenged until the next era of good feelings, cheap money and dodgy IPOs spawned the next challenger and created a new level of investment required to stay ahead.

We tell the story of CarMax above because of its relevance to Goosehead Insurance. At the onset of the pandemic, Goosehead had proven the uniqueness and durability of their model in almost every state of the union. Carriers valued their distribution, their corporate and franchised agents valued their platform which enabled great careers, and their customers valued their savings, service, and professional advice. In 2019, they grew policies in force by 44% and were extremely profitable with better than 20% EBITDA margins. They justifiably harbored grand ambitions, even though they remained but a footnote in the industry rankings. And then the COVID shutdown happened. One of the beauties of this company is that people must insure their homes and cars at all times, even in a pandemic. And then the real estate market picked up as lifestyle changes and low rates drove transactions. And Goosehead was even better positioned as the ossified State Farm and Allstate models that require physical locations in strip malls became even more preposterous to agents. (When was the last time you or anyone you know stepped foot in one of those places? Yet, they remain a requisite financial millstone around the necks of those agents.) Amidst all the turmoil and new-found work force flexibility, torrents of new people from both inside and outside of the insurance industry sought to join Goosehead. An opportunity for a generational landgrab emerged, and Goosehead seized the day rapidly accelerating the pace of hiring both corporate and franchised agents. It was true that they could only interview and train people over Zoom, but it was a risk worth taking given the opportunity to quickly become a true national force. And for a while, it worked. In 2020, policies in force grew by an astounding 48%, and margins expanded. Policies in force grew by another 42% in 2021. Cracks, however, began to develop, although at first any issues were easily covered by surging contingent commissions as industry profitability soared amidst lower driving during COVID.

Fast forward to 2022, and it was clear that agent productivity was sagging in a way that was more than just noise around a weakening real estate market. The company had outstripped its infrastructure in service, training, and field support. It was clear that many of the new agents weren’t up to snuff and/or decided to be an agent on the side while they returned to other jobs. Unlike empty car lots, unproductive agents don’t cause losses per se, but they soak up valuable resources that could be more productively engaged. Margins were cut in half, although most of that was on account of declining contingent commissions and investments in service to keep up with the growth and high wage rates. By the second half of 2022, management had seen enough and chose to act decisively as CarMax had in 1999. They began a purge of less productive agents, which will cause a deceleration in growth in the first half of 2023, but which will provide resources for investing in other proven paths to scaling productive agencies. Like the CarMax scenario above, it will take some time for the numbers to reflect the progress, but the progress is real.

2022 was, in many ways, Goosehead’s annus horribilis as industry profitability disappeared, real estate activity tanked, agent productivity sagged, and service and technology investments surged. Yet Goosehead grew revenues by 38% and grew free cash flow. And as we look forward, many of these headwinds are lessening and even beginning to reverse. Policy price increases are golden nectar to an agent who gets paid more for essentially the same work, which makes this annuity more valuable than ever. In fact, the company enjoyed an unprecedented 100% dollar retention in Q4 2022.

Looking forward, we see industry profitability and carrier’s growth ambitions returning, and with them we see the return of product availability and of pure-profit contingent commissions. We see the company leveraging significant recent investments in service and in technology. The investment in a digital agent is opening up new partnerships with organizations that have access to homeowners who would logically be open to an easy way to get a competitive quote. Embedding the Goosehead quoting engine with a mortgage processor, for example, can be an extremely efficient and entirely incremental lead generation model. But the costs of this work have been born over the last three years. Receiving a massive price increase is a catalyst for shopping your insurance coverages, just like buying a new home is. The digital agent will also be helpful as customers re-shop policies after getting sticker shock. With the complexity of integrating with carrier IT systems and running real-time risk quality assurance, only Goosehead can give you a firm quote that considers 150 different carriers to ensure the best value and embed the knowledge of millions of prior quotes to ensure the correct coverage. 2023 should be the year where we begin to see the long tail of value from these digital investments. The initiatives to drive agent productivity will also take hold this year. And even a stable real estate market would be a pleasant incremental positive.

Goosehead’s business model has now proven its resilience as well as its ability to drive growth and free cash flow due to its capital-light nature. It is impossible for the tens of thousands of captive carriers’ agents who only can offer one product, have no technology, and an inefficient go-to-market based on costly celebrity promotion to compete. As a consumer there’s no way to trust you are getting the best deal with a captive and that is becoming increasingly important in a hard insurance market where it is tough to get coverage and prices are increasing. Goosehead today has $2.2 billion in total written premium out of an industry of $380 billion with 35% held by captives. We know how this story is going to play out. Goosehead may or may not have a shot at being anything like the 150 bagger off its lows like CarMax was, but it certainly has a long and bright future which will get an incremental boost as the headwinds of 2022 and all the investments put in place over the last two years become strong incremental tailwind.

Ramesses II: the Chamath Palihapitiya of 1250 B.C.?

In the ancient and awful 1970’s, poor and abused children had no mobile devices and only three networks plus PBS for television. With so few choices, certain TV traditions sprang up including the annual showings of movies such as It’s a Wonderful Life, The Ten Commandments and The Wizard of Oz, although what holiday is a logical fit for The Wizard of Oz is unclear. I particularly liked The Ten Commandments because it was interminably long, which permitted me to stay up late. With studs Yul Brynner as Pharoah Ramesses II and Charlton Heston as Moses, it was truly a story of biblical proportions. I was always struck by the scene in which Pharoah, despite knowing better allows his ego and various other bad short-term incentives to chase after the Israelites even after he “released” them. In true technicolor glory, Moses, cornered with no way out, raises his hand and parts the Red Sea. Pharoah, despite obvious ill foreboding including an impressive burning bush, orders his men (while he watches) to chase after Moses et al. while these walls of water magically stay up at the behest of the God of the people they are chasing. Of course, as the last of the Israelites gets across, the walls of water crash down on Pharoah’s men killing them all.

This story seems to be playing out again today. Moses is the CEO of the established company with a good balance sheet trying to make rational, balanced and profitable long-term decisions. Pharoah is the Chairman of some VC-backed competitor seeking growth at any price. Moses’s people complain about not having ping pong tables or endless employee-based stock comp and having to justify their budget. Pharoah just loves harassing Moses’s companies with crazy and expensive solutions to problems that may or may not even exist but forcing Moses’s companies to invest to keep up. Moses can only exhort his people to be patient as God will not allow crazy investing without any prospect of return to continue unabated. The vengeful God will bring his wrath. In this version, God is played by Fed Chairman Jerome Powell.

We have just witnessed the wall of water come crashing down on many would be competitors of our companies. Among the companies above, for example, Xometry has seen a number of pseudo knockoffs fold and other “digital manufacturing” companies have seen their stocks and prospects collapse to raise going concern issues. “Digital health tech” companies trying to cobble something akin to Progyny light are seeing funding pulled, and a company trying to get around Progyny’s fortress position by building its own network of IVF clinics failed in its capital raise last year and is resorting to debt which effectively bogs them down in a loss-making low gear. Goosehead’s digital agent will have less competition in the future than it might have had, as a number of “insurtech” companies have folded or been sold for pennies on the dollar. One surviving insurtech is Lemonade, Inc. (LMND) which has seen its stock fall from a peak above $180 to its current $13, which is roughly its book value. They were smart enough to raise a pile of money when they could, but with projections of more than $8 per share in losses over the next two years, things aren’t looking very bright. We mention Lemonade specifically because their journey says a great deal about Goosehead. Lemonade came public with a vision of being a pure digital, direct to consumer insurance carrier. No distribution needed, just spend the money to build a brand, and the customers will come to you. As Mike Tyson wonderfully said, “Everyone has a plan until they get punched in the mouth.” Building the brand turned out to be much more expensive and difficult than expected. Simply paying for distribution would be easier and more effective. And they discovered something, to them at least, unexpected. When people are insuring their biggest asset and are aware of the complexity, risks, and downside around selecting insurance, they actually want to get advice from an agent. Further, the agent can vet the client and make sure it’s the right risk for the carrier, especially when that agent is incentivized by contingent commissions. Faced with an existential risk, Lemonade decided to pivot and embrace independent distribution. And guess who their biggest agent is today? Goosehead. And guess who provides them their most profitable clients? Goosehead, whose quality assurance ensures much better risk than the adverse selection laden stuff that Lemonade gets directly. Our conversations with Lemonade have reinforced the belief that it will be a long, long time before insurance agents are disintermediated because they add real value to clients and to carriers. And to the extent that agents are someday disintermediated, it won’t be geeks in a garage with no insurance knowledge doing the disintermediation. It will be Goosehead itself with its very refined digital agent.

The collapse of these potential competitors greatly expands the runway of growth and the moats around the businesses we own. Of course, in a stock market where investors bet on sectors or factors, the crushing of a group of companies will invariably drag down all companies considered to be in the group for a short time at least, even if one company benefits from the demise of the other. But our companies have the financial strength and resilient business models needed to not only get through a period of difficult financing but to take advantage of it and earn great returns on organic and inorganic investments. The Ten Commandments was such a long movie, I never followed where Moses actually took his people. Presumably a Four Seasons in the desert. But we know where our companies are going, and the walls of water collapsing on our companies’ competitors will only accelerate their arrival.

The Next Letter

This was an unusual letter. We tried to take our time to give a broader update on our key holdings. As a result, it was longer (and later) than a more typical letter. In the next letter we will try to review the rest of the holdings. We will also introduce a new position. Spoiler alert: the new name is not CarMax. We mentioned we had been working on it in the last letter, and we mentioned it again today, but we are not ready to plunge into CarMax. It is solid, and it will get through this period. But the vast majority of their earnings are now coming from finance operations, as opposed to pure vehicle margin, and we expect finance spreads to be under pressure for some time. And even if competitor Carvana goes bankrupt, they will still be around in some form, applying pressure and requiring CarMax to keep investing dimming its prospect for margin recovery. By contrast, the name we look forward to speaking about will be a classic “triple win”, with a de-risked entry point and an outlook that includes a temporary headwind abating over time and yielding to the very significant long-term tailwinds providing the company with top line acceleration, margin improvement, and multiple recovery off depressed lows.

Investment Program

For the benefit of any first-time readers, the hallmark of the Owls Nest Partners approach is the purchase of industry leading growth companies when a temporary headwind has recoiled the fundamental growth drivers and compressed its multiple. This typically happens as hot money “renters” exit and drive the price down. There is no such thing as a free lunch: we can only receive our requisite value if we accept that our companies will appear “catalyst-less” and uninteresting for some time. We believe we are wildly overcompensated for this modest level of patience, especially since it is in these moments that a company can invest in its own business with the highest returns. There is wonderful optionality associated with a well-run, shareholder friendly, cash- laden company that is able to aggressively put money to work during a temporary headwind.

It is our belief (and experience) that our future outperformance will not be driven by any economic or market forecasting prowess but instead by ten unique investments, each playing out over time. We perceive these investments to have modest downside due to high quality and low expectations, and very significant upside as growth and margin expansion return in spades. We seek reasonable ballast and diversification within the portfolio as a result of our natural conservatism (strengthened by our co-investment alongside clients) and our predisposition to avoid crowded trades and instead invest in temporarily out of favor areas.

Final Thoughts:

More than ever, we thank you for your support and for choosing to have your money working alongside ours.

Gratefully,

Philip, and the Owls Nest Partners team

Disclaimer

In General: This disclaimer applies to this document and the verbal or written comments of any person presenting it. This document has been prepared by Owls Nest Partners IA, LLC as Investment Adviser (the “Adviser”) of Owls Nest Partners Concentrated Long Only SMA (the “Strategy”). By receiving this document you acknowledge that you are an investor in the Strategy, or a prospective investor who is known to the Adviser, and that you meet all regulatory definitions of “Accredited Investor” and “Qualified Client,” in order to be considered a prospective client of the Adviser. The information included herein reflects current views of the Adviser only, is subject to change, and is not intended to be promissory or relied upon. There can be no certainty that events will turn out as the Adviser may have opined herein.

No offer to purchase or sell securities: This document does not constitute an offer to sell (or solicitation of an offer to buy) any security and may not be relied upon in connection with the purchase or sale of any security.

No reliance, no update and use of information: You may not rely on this document as the basis upon which to make an investment decision. To the extent that you rely on this document in connection with any investment decision, you do so at your own risk. This document is being provided in summary fashion and does not purport to be complete. The information in this document is provided you as of the dates indicated and the Adviser does not intend to update information after its distribution, even in the event the information becomes materially inaccurate.

Knowledge and experience: You acknowledge that you are knowledgeable and experienced with respect to the financial, tax and business aspects of this presentation and that you will conduct your own independent financial, business, regulatory, accounting, legal and tax investigations with respect to the accuracy, completeness and suitability of this information, should you choose to use or rely on this document, at your own risk, for any purpose.

No tax, legal or accounting advice: This document is not intended to provide and should not be relied upon for (and you shall not construe it as) accounting, legal, regulatory, financial or tax advice, or investment recommendations. Any statements of U.S. federal tax consequences contained in this document were not intended and cannot be used to avoid penalties under the U.S. Internal Revenue Code or to promote, market or recommend any tax-related matters addressed herein.

Confidential information and distribution: By accepting receipt or reading any portion of this document, you agree that you will treat all information contained herein confidentially. Any reproduction or distribution of this document or any related marketing materials, as a whole or in part, or the disclosure of the contents hereof, without the prior written consent of the Adviser, is prohibited.

Suitability: Any investment program involves a high degree of risk and is suitable only for sophisticated investors who meet certain other suitability standards.

Investment strategies, market conditions and risk disclosures: Notwithstanding the general objectives and goals described in this document, readers should understand that the Adviser is not limited with respect to the types of investment strategies it may employ or the markets or instruments in which it may invest. Over time, markets change and the Adviser will seek to capitalize on attractive opportunities wherever they might be. Depending on conditions and trends in securities markets and the economy generally, the Adviser may pursue other objectives or employ other techniques it considers appropriate and in the best interest of the Fund. No representation or warranty is made as to the efficacy of any particular strategy or actual returns that may be achieved.

Projections: This document may contain certain “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of the Strategy’s investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

Disclosures

- Performance presented from inception through September 2020 is for a representative account of the Owls Nest Partners Concentrated Long Only SMA strategy (the “Strategy”). As of October 2020, performance is for a composite of separately managed accounts managed in accordance with the Strategy (the “Composite”). Performance is presented gross and net of all fees, as of the date listed at the top of this document. The fees applied are the prevailing fees of the Strategy at the time such performance was generated. From inception to the date of this document, the fee structure applied is a 1% annual management fee, and 15% performance fee that is charged only on the outperformance of the Strategy to the Benchmark (as defined below), and only after five years. Performance fees are accrued monthly. The vehicle for the Strategy is a separately managed account. All performance is calculated by the Adviser. Further information regarding the Strategy or the Composite can be provided upon request. The Adviser does not claim compliance with the GIPS reporting standards and the performance presented herein has not been audited or verified by any third-party. The Russell 2000 Total Return Index (the “Benchmark”) is a broad market index that is presented for comparative purposes as the performance benchmark to the Fund. The Benchmark is an unmanaged index consisting of the smallest 2000 stocks in the Russell 3000 Index. The stocks are issued in the United States, and the Benchmark includes the reinvestment of all dividends and income. Because the Benchmark is unmanaged, it assumes no transaction costs, management and performance fees, or other expenses. Unlike the Fund, it contains only domestic companies and is rebalanced monthly. Therefore, while the Benchmark contains publicly traded companies, it does not purport to represent an exact performance comparison to the Strategy. It is not possible to invest directly in an index, such as the Benchmark.

- The Russell 2000 Total Return Index is the performance benchmark for the Strategy (the “Benchmark”). The Benchmark is a domestic equity market index of the 2,000 smallest companies by market capitalization in the Russell 3000 Index. Because the Benchmark is unmanaged, it assumes no transaction costs, management fees or other expenses. The calculation of the benchmark return includes the reinvestment of all dividends. It is not possible to invest directly in an index, such as the Benchmark, and therefore it is presented here for information purposes only.