- Responsible for new idea generation; portfolio construction; risk management; due diligence

- 25+ years overseeing concentrated small-cap portfolios, on behalf of the most sophisticated allocators in the United States

- Previously: Founder, Endowment Capital Group; Portfolio Manager, Downtown Associates; Analyst, W.H. Newbold’s Son & Company

- University of Pennsylvania, Wharton School, B.S. 1986

- Married to Isabella, 3 sons, 3 daughters, 2 dogs

by Owls Nest Partners on Dec 5, 2025

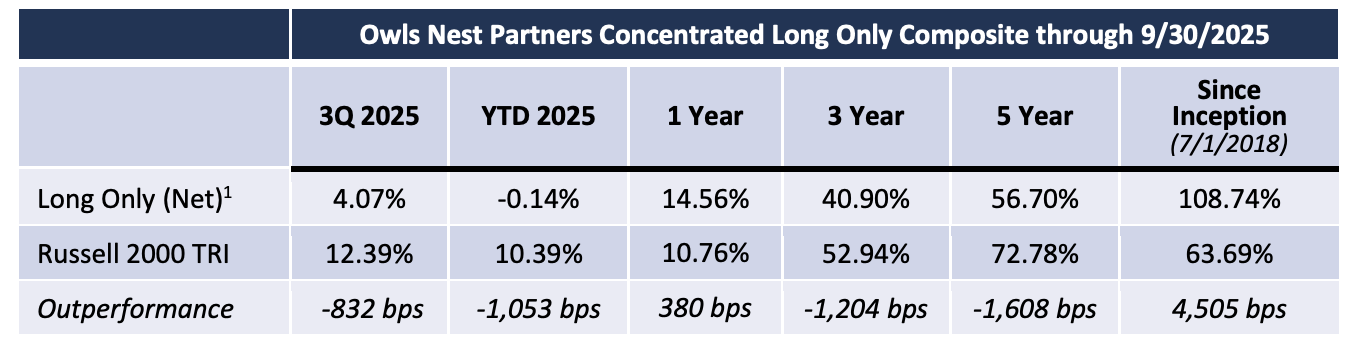

Performance:

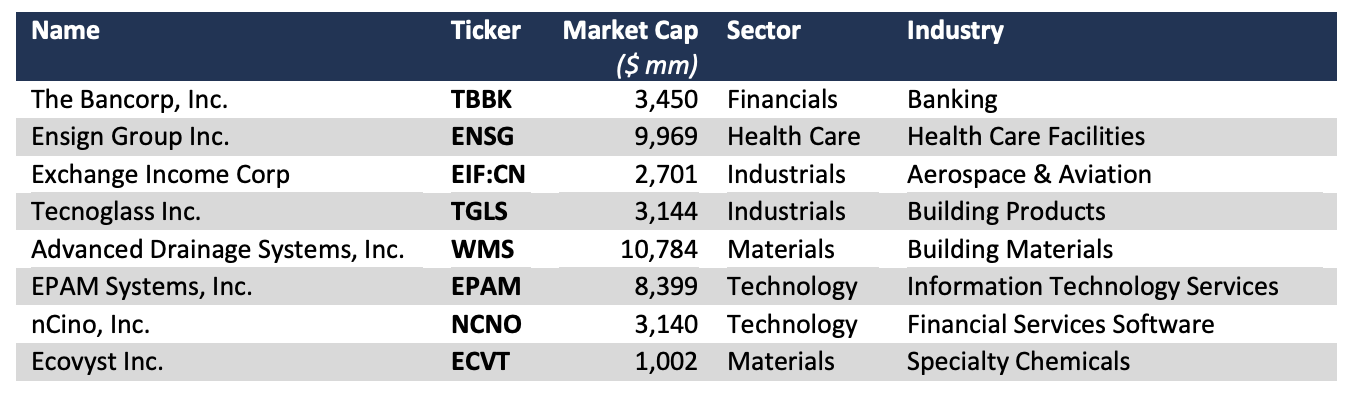

Holdings as of 9/30/2025

We ended September 30, 2025, with the following holdings (in order of position size, largest to smallest):

Median Net Debt/Market Cap: 2.37%

Median Market Cap: $3,297 million

Median Market Cap at Entry: $2,309 million

Active Share vs. Russell 2000: 99.45%

1Past performance is not indicative of future results. Performance presented from inception through September 2020 is for a representative account of the Owls Nest Partners Concentrated Long Only SMA strategy (the “Strategy”). As of October 2020, performance is for a composite of accounts managed in accordance with the Strategy (the “Composite”). Please see the Disclosures at the end of this document for further information with regards to performance.

Market Commentary & Outlook

Most market commentaries today come down to a debate between smart people who argue that the AI revolution will drive unprecedented and even still under-appreciated productivity and profitability gains, and other equally smart people who argue that this AI-driven market is irrational, overpriced, extremely narrow and driven by themes and memes as opposed to fundamentals. While we have views, and we certainly pay close attention to the risks and opportunities associated with AI, we think that all the focus on AI has created enormous and comparatively low risk opportunities for those able to think in absolute, not just relative, terms and who are structured accordingly. Periods like this aren’t new to us and we think there is a great way to capitalize, leveraging a tried-and-true playbook that is right in our wheelhouse.

Mark Twain is attributed with the quote that “history never repeats itself, but it often rhymes”. During the “dotcom bubble” – named after the fact – in 1999 and early 2000, I had the privilege of managing money for a family office and some leading endowments. I was incredibly lucky because I felt zero pressure to manage to any benchmark. My mandate was clear: buy good businesses cheap and leverage our ability to think and act longterm - precisely the opposite of worrying about an index. That experience shaped the mindset we still hold today: stay focused on long-term fundamentals rather than chase whatever parts of the market are most in vogue.

In the time leading up to the bubble’s bursting, I did manage to keep up and even outperform the relevant indices, not because of any acumen or foresight, but probably because I was inexperienced and didn’t have as much of my own money in the fund as I do today. But the story of a bubble and its bursting, to me, is not a story of how anyone managed their exposure to the portion of the market caught up in the bubble. That, to me, is a little bit like discussing when in 2016 the Chicago Bears had won 10 consecutive coin tosses, and should you bet on them winning the 11th. (By the way, the answer to that was yes, because they went on to win 14 straight, but still didn’t make the playoffs). Trying to time extremes is notoriously difficult; even the best investors rarely get it right.

Instead, what I take from a bubble is this: when everyone else is looking in one direction, what kinds of special, rare opportunities are you able to pick up by looking in the other, neglected direction. Just as in prior cycles, not anchoring ourselves to an index helps us stay focused on what ultimately matters: finding durable businesses that are being overlooked in a market driven by a very narrow set of themes.

The obvious but forgotten thing is: if you want to play in a fashionable area of the market, you must sell something perceived as unfashionable to have the proceeds to participate in the popular trade. When enough people do that, you have extremely attractive and de-risked opportunities in overlooked areas of the market and an infinitely more appealing opportunity set rather than risking staying too long at the crowded end of the market. Here is a case in point. The dot com bubble held that brick and mortar retailers were dead. Their stocks were ignored, and broadly shorted. If a brick and mortar retailer had remotely stumbled even while growing quickly, you were especially punished. Your stock price misery was further compounded if you were a somewhat complicated story because you were only recently public with no direct comparable companies or if part of your earnings were from your finance arm. Long-term readers will recognize where I’m going with this, as I have spoken before about CarMax in 2000, when the company was so ignored that even its banker, Morgan Stanley, dropped research coverage. But the situation is certainly a relevant lesson for today: if you did work on the company, you realized that their use of internet technology – primarily putting inventory on the website for customers to search at home and by simplifying the buying process – was not only a wildly positive differentiator for the customer experience but also greatly enhanced sales productivity. The internet wasn’t killing them. It was supercharging them and making them a clear leader in a huge, recession- resistant industry. And once investors gave up on the dot com names and returned their focus to growth and quality in other areas, CarMax soared. It was up ~100-fold over the next two decades. That sort of return is only possible if you can zig when Page 3 of 9 2. Gross performance numbers cited are from Endowment Capital L.P. All clients paid fees and hence no clients ultimately received the precise gross numbers cited. Please see the Endowment Capital Group Disclosures at the end of this document for further information. others are zagging, dig deep, and if you can invest with duration. Similar stories came out of the housing / commodity bubble of 2007 that led to the Global Financial Crisis. Again, it was essential to think independently and in absolute terms to avoid the pressure to participate in areas that were all the rage. Even the most sophisticated players with access to the brilliant derivative financial innovations got burned. In fact, many of them were especially burned. When the dust settled, the Russell 2000 was down over 15% for the combined 2008 and 2009, and the S&P 500 index was down more than 20%. But my fund, focused on the names that had been ignored in the runup, was up 95% gross during the same period2 . Although it can be uncomfortable at first in real time, it pays to zig when others zag.

So, we come to today – is this an AI bubble? That’s unclear. What is clear is that it’s not the kind of game we want to play.

Whether AI leaders are over- or undervalued today isn’t something we claim to know. What we do know is that free enterprise, capitalism, and free markets are wonderful and destructive things, and when a small group of companies attracts the bulk of the market’s excitement, it inevitably invites competition and raises the bar for future expectations – while leaving attractive, fundamentally sound opportunities outside the spotlight. There will be winners, like Amazon from the dot com bubble, and there will be many losers, including some that disappear. But even the winners when bought at the height of their popularity, will test your fortitude. Very few of the most ardent Amazon bulls made it through the 95% - yes 95% - drawdown in AMZN stock, during the bust. Hence, we always believe that the best opportunities and certainly the ones with the lowest risk of permanent capital loss, come by looking where others are not, especially when the tunnel vision is profound, and even systemic.

Our outlook is extremely positive. We own very high quality, compounding companies that trade at unsustainably suppressed prices based on the investment community’s extreme pessimism for things not caught up in the AI mania (like our new position, Exchange Income Corporation, briefly discussed later in this letter). And ironically, much like how CarMax was a beneficiary of the internet, many of our companies will prove to be great beneficiaries of the ongoing AI-driven transformation. No one knows when the pendulum in stock attention will reverse, but the pressure on active management to capitulate in order to keep up is getting as extreme as it did in the months leading up to the massive pendulum shift that led to the dot com burst. In the interim, our companies are growing nicely and acquiring companies at depressed valuations or buying back stock at depressed levels while we continue to work enthusiastically on new ideas.

Q3 Portfolio News and Attribution

Q3 portfolio news consists mainly of companies reporting their Q2 earnings and giving commentary and guidance on their outlook. For us, the news was almost unilaterally good. We entered the quarter with nine holdings. Eight of them beat our/consensus expectations and one was in line. And in a turbulent macro era when you don’t want to be a hero and raise guidance, four raised guidance for the rest of the year and/or for next year, four maintained their guidance, and one doesn’t give guidance. On top of that, two companies announced significantly expanded buybacks.

There was some meaningful news beyond earnings as well. Advanced Drainage Systems (WMS) announced the acquisition of National Diversified Sales (NDS), a leading manufacturer of products for water management that will be integrated into a stronger and broader offering for WMS and with almost zero product overlap. This is a significant ($1 billion) strategic acquisition that is immediately accretive to earnings per share. This was the acquisition we hoped for when we first initiated a position and discussed WMS. We talked to lots of people Page 4 of 9 around NDS including people who had worked for both companies. This is a clear strategic fit that makes WMS more than ever the go-to-one stop shop, and we have extra comfort because of this management’s stellar track record with smart acquisitions and great integrations.

The Bancorp (TBBK), our “arms dealer to fintechs”, announced a very significant client win. They were selected to support the Block (Cash App) card being rolled out in 2026. This was the biggest prize to be won in the industry in 2025. The Bancorp also announced an incremental buyback amounting to another ~10% of the company to be executed in Q3 and in Q4. All in all, between 2023 and 2026, TBBK will have bought back ~30% of the company, with an average price well below 10x 2027 earnings.

More than ever, we thank you for your support and for choosing to have your money working alongside ours.

We had three meaningful gainers in the quarter (The Bancorp, Ensign Group, Advanced Drainage Systems) and three detractors of consequence (Tecnoglass, Goosehead Insurance, EPAM Systems). TBBK powered higher on the back of the client win and the buyback. Ensign Group (ENSG) chugged along based on higher earnings and good acquisition volume, and WMS rose on earnings and the announced NDS acquisition.

Tecnoglass (TGLS), Goosehead (GSHD), and EPAM Systems (EPAM) were generally guilty of being in “bad neighborhoods” in terms of investor sentiment, even if they have idiosyncratic growth drivers that transcend the rest of the industry. TGLS is in the building materials industry, which is suffering through an extended down period in single family residential (SFR) construction related to affordability challenges for the middle and lowend consumer. New SFR, however, is only a very small portion of TGLS’s business. Over half of the business is commercial / high rise multifamily, which has a long lead time. That business, focused on luxury high-rises, is performing very well, sold out with a still growing backlog extending into 2027. The half that is tied to SFR is predominantly linked to the stable repair and remodel portion of the SFR space. While that business is certainly impacted by lower existing home sales, TGLS is still gobbling up market share, growing through the headwinds based on new products and an expanded dealer base in new geographies. Buying the leader, with the best margins, cost structure and balance sheet while they are investing in new products and additional sales resources during a downturn is a proven money-making strategy. TGLS will continue to grow now and will be poised to take off when the industry backdrop improves or even when investor sentiment anticipates an improvement. And management, which owns 40% of the company, is clearly confident of the near and long term as evidenced by their announcement of an aggressive share repurchase. The fact that the affordability issue has gotten so much attention – enough to power the election of a socialist for mayor of New York City – is typically indicative of approaching the point of maximum pain in the space.

The insurance industry in which GSHD competes has been a broad beneficiary of rising insurance rates since the COVID induced inflation emerged. Insurance inflation has peaked, and prices may be headed south. Fear of this change has understandably caused investor sentiment to turn away from insurance. We don’t disagree with this notion and discuss our sale of GSHD below.

Lastly, EPAM was weak as investors stay on the sideline, wanting to see the impact of AI on all software engineering and IT service businesses. As we noted earlier, in periods when excitement concentrates elsewhere, some of the most compelling long-term beneficiaries of AI implementation can be found in the overlooked parts of the market – and EPAM fits that pattern well. EPAM is an absolute leader in high end software engineering, and our belief, based on dozens of conversations with their clients, is that high end software engineering is not going to disappear as a result of AI. On the contrary, AI will prove to be an accelerant, as companies will need help with the heavy lifting to get data organized for AI, and the talent needed to harness AI in a compliant, industrial-strength way will be very scarce compared to the size of the need. Taking advantage of its financial strength and depressed multiples in the industry, EPAM is augmenting its organic growth by making countercyclical acquisitions that expand their industry and geographic reach and is buying back its own stock aggressively. As companies seek a return on their massive AI investments, the AI cycle will turn from buildout, Page 5 of 9 to delivery, and then to deployment. EPAM will be a large beneficiary of the huge spend needed to leverage this unprecedentedly large investment. And the current starting point with depressed margins, accelerating top line, and all-time trough multiple makes EPAM stock especially coiled.

Q3 2025 Portfolio Adjustments

It was an active quarter for us. We exited 3 positions (Paylocity, JB Hunt, Goosehead) and added two new positions (Exchange Income Corp, Ecovyst). We also lightened up on some positions that had moved up (WMS, TBBK, ENSG), while we added to TGLS and EPAM, effectively buying back stock that we had sold at higher prices earlier in the year.

Each of the sales reflects important elements of our sell discipline. While we invest with a long-term lens, our process is flexible enough to adapt when the world changes. We remain believers that investment managers can add as much value over time with disciplined sales as they can with shrewd buys.

Paylocity (PCTY) was a solid winner for us that we bought well and that grew nicely during our holding period. The outlook for PCTY remains quite strong, and we could certainty justify holding our position. But two things have changed recently, causing us to sell. First, we are believers in stable industry structures, and hence we believe that supply and industry capital flows are as important as demand. A smaller “next generation” competitor, Rippling, just got funded at a massive ($17B) valuation in its latest financing. While one could argue that given PCTY’s considerably bigger size, hugely greater profitability and significantly lower valuation, Rippling’s valuation is a great thing for PCTY, at least from a relative valuation perspective. However, this financing requires Rippling to enter “grow at any price” mode and arms them to make waves in the industry over time despite their small size today. Rippling and any investment in Rippling, may or may not ultimately be successful, but we like owning companies that have unfair advantages. PCTY has definite advantages and a very sticky and growing client roster in a great industry, winning share from competitors like ADP and Paychex with antiquated and cobbled together technology. But with Rippling’s ultra-modern tech stack and limitless ability to spend, it is no longer an unfair fight favoring PCTY. This decision reflects lessons learned over decades: when the structural dynamics of an industry shift, even subtly, we act decisively, rather than risk even a slow erosion that compounds over time.

President Trump’s tariffs could not have come at a worse time for JB Hunt (JBHT). The setup was good. Supply was getting back in line after a COVID surge and positive sentiment among shippers around the domestic economy poised JBHT for some meaningful price increases in the upcoming freight bid season, which would drive accelerating profitability. Then the tariffs led to a wave of uncertainty and demand destruction, especially with imports which arrive at western ports and use JBHT’s industry leading intermodal services to get to their final destinations across the country. JBHT remains a great company and will do well. They have levers they can pull to support earnings through a tough environment and are buying back stock. But the excitement around a new positive freight cycle and accelerating revenue momentum for JBHT is deferred for the foreseeable future, and we have opportunities to make our dollars work harder elsewhere.

GSHD has been a big, multi-year winner for us with returns driven by huge growth and margin expansion, and further, helped by our taking advantage of stock price volatility, selling when excitement drove it to high prices, and loading up when it was depressed. Along the way, the secular growth story of share gains in a huge industry has been the driver. In recent years, it has been assisted by higher pricing in personal lines insurance. Higher prices – and hence higher nominal growth – also helped investor sentiment across the insurance industry broadly and drove industry stock multiples higher. Pricing is now stabilizing and likely – and mercifully for the consumer Page 6 of 9 – headed south. This new trajectory will slow nominal growth across the industry and will likely lead to multiple compression as investors move on to more accelerating areas. Reduced pricing has some benefits for GSHD, in that it helps client retention as consumers price shop less. Also, it reflects the current high level of carrier profitability, and carriers wanting to grow will drive higher product availability and commission rates for GSHD. For these reasons and more, it is entirely possible that we will own GSHD again, but we would need to see improvements in product availability, retention and commission rates manifest themselves and not just be an expectation, and we’d need to make sure that they can more than offset a decline in unit pricing.

New Holdings & Next Letter

Congrats! You win a prize (perhaps extra Omaha Steaks) by being probably the only person to make it this far in this letter. Throughout this letter, we have chosen to give full attention to our thought process around our closed-out positions and the current market. Accordingly, we will save the discussion of our newest portfolio additions until the next letter. But suffice it to say, we believe that the portfolio is significantly derisked while adding absolutely attractive names into the portfolio by looking where others are not. How else to explain our getting a company that probably no one reading this letter has ever heard of, that has compounded shareholder returns for over 20% a year for over 20 years, without any multiple expansion, when it is on the cusp of leveraging its monopoly position in its industry in ways that harvest global megatrends, which will throw additional fuel on a shareholder return fire that has run hot for a long time. Stay tuned and keep the faith. You – and we alongside you, to the tune of more than $50M – own great businesses and are aggressively looking for great returns while prudently applying lessons learned in past cycles and the knowledge that aspects of human behavior, especially greed and fear, are timeless. Remember that losing money, especially when you can look back and ask yourself “what was I thinking?”, really sucks.

Investment Program

For the benefit of any first-time readers, the hallmark of the Owls Nest Partners approach is the purchase of smaller, industry leading companies when a temporary headwind has recoiled the fundamental growth drivers and compressed their multiple. This typically happens as hot money “renters” exit and drive the price down. There is no such thing as a free lunch: we can only receive our requisite value if we accept that our companies will appear “catalyst-less” and uninteresting for some time. We believe we are handsomely rewarded for this modest level of patience, especially since it is in these moments that a company can invest in its own business with the highest returns. There is wonderful optionality associated with a well-run, shareholder friendly, cashladen company that is able to aggressively put money to work during a temporary headwind.

It is our belief (and experience) that our future outperformance will not be driven by any economic or market forecasting prowess, but instead by ten unique investments, each playing out over time. We perceive these investments to have modest downside due to high quality and low expectations, and very significant upside as revenue growth and margin expansion return in spades and as increased investor confidence justifies a higher multiple of earnings for the company’s stock. We seek reasonable ballast and diversification within the portfolio as a result of our natural conservatism, strengthened by our co-investment alongside clients.

Final Thoughts

More than ever, we thank you for your support and for choosing to have your money working alongside ours.

Gratefully,

Philip, and the Owls Nest Partners team

Disclaimer

In General: This disclaimer applies to this document and the verbal or written comments of any person presenting it. This document has been prepared by Owls Nest Partners IA, LLC as Investment Adviser (the “Adviser”) of Owls Nest Partners Concentrated Long Only Strategy (the “Strategy”). By receiving this document you acknowledge that you are an investor in the Strategy, or a prospective investor who is known to the Adviser, and that you meet all regulatory definitions of “Accredited Investor” and “Qualified Client,” in order to be considered a prospective client of the Adviser. The information included herein reflects current views of the Adviser only, is subject to change, and is not intended to be promissory or relied upon. There can be no certainty that events will turn out as the Adviser may have opined herein.

No offer to purchase or sell securities: This document does not constitute an offer to sell (or solicitation of an offer to buy) any security and may not be relied upon in connection with the purchase or sale of any security.

No reliance, no update and use of information: You may not rely on this document as the basis upon which to make an investment decision. To the extent that you rely on this document in connection with any investment decision, you do so at your own risk. This document is being provided in summary fashion and does not purport to be complete. The information in this document is provided you as of the dates indicated and the Adviser does not intend to update information after its distribution, even in the event the information becomes materially inaccurate.

Knowledge and experience: You acknowledge that you are knowledgeable and experienced with respect to the financial, tax and business aspects of this presentation and that you will conduct your own independent financial, business, regulatory, accounting, legal and tax investigations with respect to the accuracy, completeness and suitability of this information, should you choose to use or rely on this document, at your own risk, for any purpose.

No tax, legal or accounting advice: This document is not intended to provide and should not be relied upon for (and you shall not construe it as) accounting, legal, regulatory, financial or tax advice, or investment recommendations.

Confidential information and distribution: By accepting receipt or reading any portion of this document, you agree that you will treat all information contained herein confidentially. Any reproduction or distribution of this document or any related marketing materials, as a whole or in part, or the disclosure of the contents hereof, without the prior written consent of the Adviser, is prohibited.

Suitability: Any investment program involves a high degree of risk and is suitable only for sophisticated investors who meet certain other suitability standards.

Investment strategies, market conditions and risk disclosures: Notwithstanding the general objectives and goals described in this document, readers should understand that the Adviser is not limited with respect to the types of investment strategies it may employ or the markets or instruments in which it may invest. Over time, markets change and the Adviser will seek to capitalize on attractive opportunities wherever they might be. Depending on conditions and trends in securities markets and the economy generally, the Adviser may pursue other objectives or employ other techniques it considers appropriate and in the best interest of the Fund. No representation or warranty is made as to the efficacy of any particular strategy or actual returns that may be achieved. The Strategy is subject to investment risk, including possible loss of the entire principal amount invested. Investors must be prepared to bear the risk of a total loss of their investment.

Projections: This document may contain certain “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of the Strategy’s investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

Disclosures

- Past performance is not indicative of future results. Performance presented from inception through September 2020 is for a representative account of the Owls Nest Partners Concentrated Long Only SMA strategy (the “Strategy”). As of October 2020, performance is for a composite of all accounts managed by the Adviser with substantially similar investment policies and objectives as the Strategy (the “Composite”). Composite performance may be considered ‘hypothetical performance’ under Rule 206 (4)-1 (the “Marketing Rule”) of the Investment Advisers Act of 1940 (the “Adviser’s Act”), as amended. The Adviser has established policies to meet the requirements of the Marketing Rule. Performance is presented net of all fees as of the date listed at the top of this document and includes the reinvestment of all realized proceeds, income, and earnings. From inception through August 2022 the fees applied are the highest fees received by the Adviser for a separate account managed within the Strategy, which is a 1% annual management fee, and 15% performance fee charged only on the outperformance of the Strategy to the Benchmark (as defined below), accrued over 5 years. From September 2022 the performance fee accrued is 20% of the outperformance, which represents the highest fee received by the Adviser for a separate account managed within the Strategy at that time. Performance fees are accrued monthly. The expected vehicle for the Strategy is a separately managed account. All performance is calculated by the Adviser. Further information regarding the Strategy or the Composite can be provided upon request. The Adviser does not claim compliance with the GIPS reporting standards and the performance presented herein has not been audited or verified by any third-party. All monthly returns presented for the Strategy or the Composite represent preliminary, unaudited figures that are subject to change.

- The Russell 2000 Total Return Index (the “Benchmark”) is a broad market index that is presented for comparative purposes as the performance benchmark to the Strategy. The Benchmark is an unmanaged index consisting of the smallest 2000 stocks in the Russell 3000 Index. The stocks are issued in the United States, and the Benchmark includes the reinvestment of all dividends and income. Because the Benchmark is unmanaged, it assumes no transaction costs, management and performance fees, or other expenses. Unlike the Strategy, it contains only domestic companies and is rebalanced monthly. Therefore, while the Benchmark contains publicly traded companies, it does not purport to represent an exact performance comparison to the Strategy. It is not possible to invest directly in an index, such as the Benchmark.